We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

State Pension taxable

Comments

-

At most 20% of future increases will be offset by additional tax. Unless you're one of the few people lucky enough to be a higher rate taxpayer in retirement, in which case I'm sure you'll find a way of coping.

0 -

The freeze on tax thresholds raises a LOT of cash (Rachel reeves getting a whopping chunk in from this January) - taxes needed to go up and Labour promised not to raise taxes so they have just left the existing freeze in place.

I think higher thresholds and higher tax percentages would have been more targeted but would have blatantly breached manifesto.

0 -

I have no political bias. But the way both Parties have 'got away' with not changing the lowest Tax threshold for years, is a disgrace. I think its partly because the average worker probably doesnt understand the rules of 'threshold' they just look at the bottom lines.of their payslip.

Imagine trying to do that to the French !

0 -

I can understand it somewhat but not in conjunction with the basic and higher rate bands also being frozen.

In real terms, the personal allowance is still high. Higher than it was 15-20 years ago. So, fiscal drag is just bringing it back to historic norms.

In 20078 - it was £5,225. Increasing that by inflation would be around £9,250 today. (using ONS inflation uplift of 1.77 between those years)

The higher rate threshold was £34,600 in 2007/8. Applying the same 1.77 uplift for inflation gives £61,300.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.4 -

Even worse in Scotland where higher rate tax starts at £43,633 and at 42%.

Back in 2007/8 the ordinary classroom teacher wasn’t a higher rate taxpayer in Scotland. Now with the daft Scottish tax bands many are.

0 -

Is that not a little bit misleading when viewed just on it's own though?……..several other things have changed over that time which more than offset this……basic rate tax has fallen to 20% from the 22% it was in 2007/8 (even though the 10% rate was also abolished), and employee NI is much lower now than it was then.

Someone earning £34600 back in 2007/8 would have seen 27.2% in govt deductions (ie income tax and NI), while the same person earning the inflation adjusted equivalent of £61300 today would, despite the freeze, be paying 24.8%. If you factored in pension contributions too, the gap is even wider …….

I'm in no way defending or justifying the freeze itself …….especially on the personal allowance with the disproportionate effect on lower income groups……so I'm in the opposite camp, where, to a degree, I can understand the freeze on the BR/HR/AR thresholds, but not on the personal allowance.

2 -

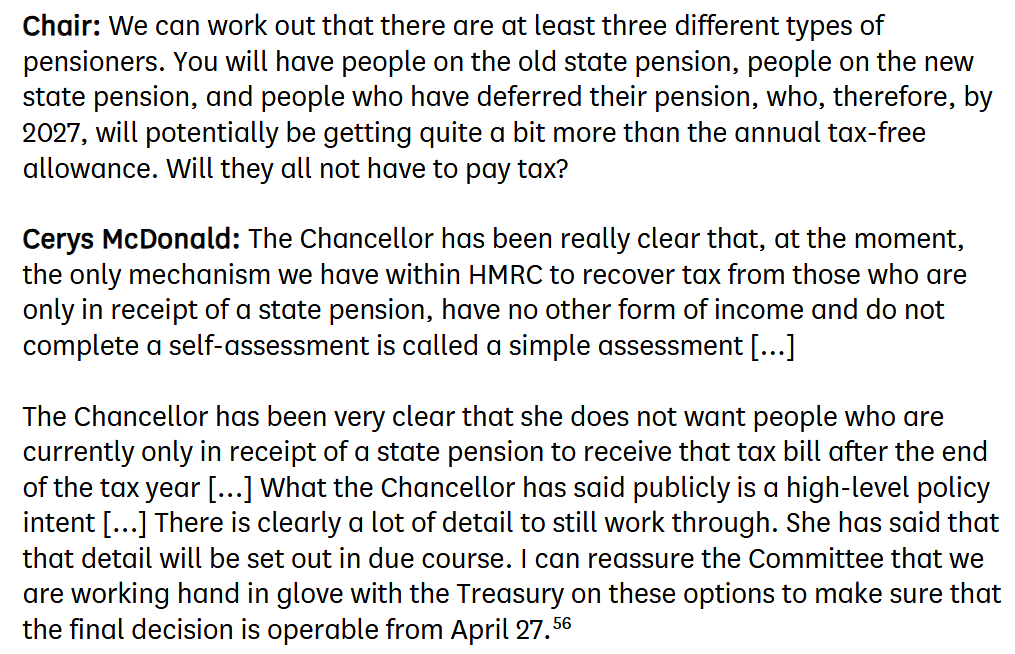

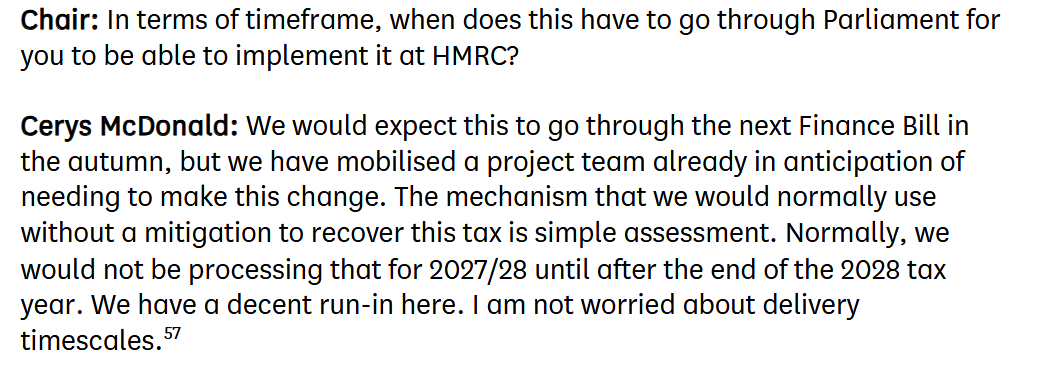

This House of Commons research briefing on the 'Taxation of State Pension' came out on 6th February. This covers the 2025 budget announcement relating to the payment and collection of tax when the full new state pension exceeds the personal allowance in 2027/2028. I can't see that this briefing has been mentioned on these forums so here it is

https://researchbriefings.files.parliament.uk/documents/CBP-10250/CBP-10250.pdf

Page 13 includes a Treasury Select Committee question of when this might be resolved and implemented, the text covering this is copied below

I came, I saw, I melted4

I came, I saw, I melted4 -

not everyone.

anyone who earns £100k begins to lose is, and after £125k it’s gone completely.

That’s a marginal tax of 62%.Oh and the threshold been unchanged since 2009, now THAT is fiscal drag.

0

0 -

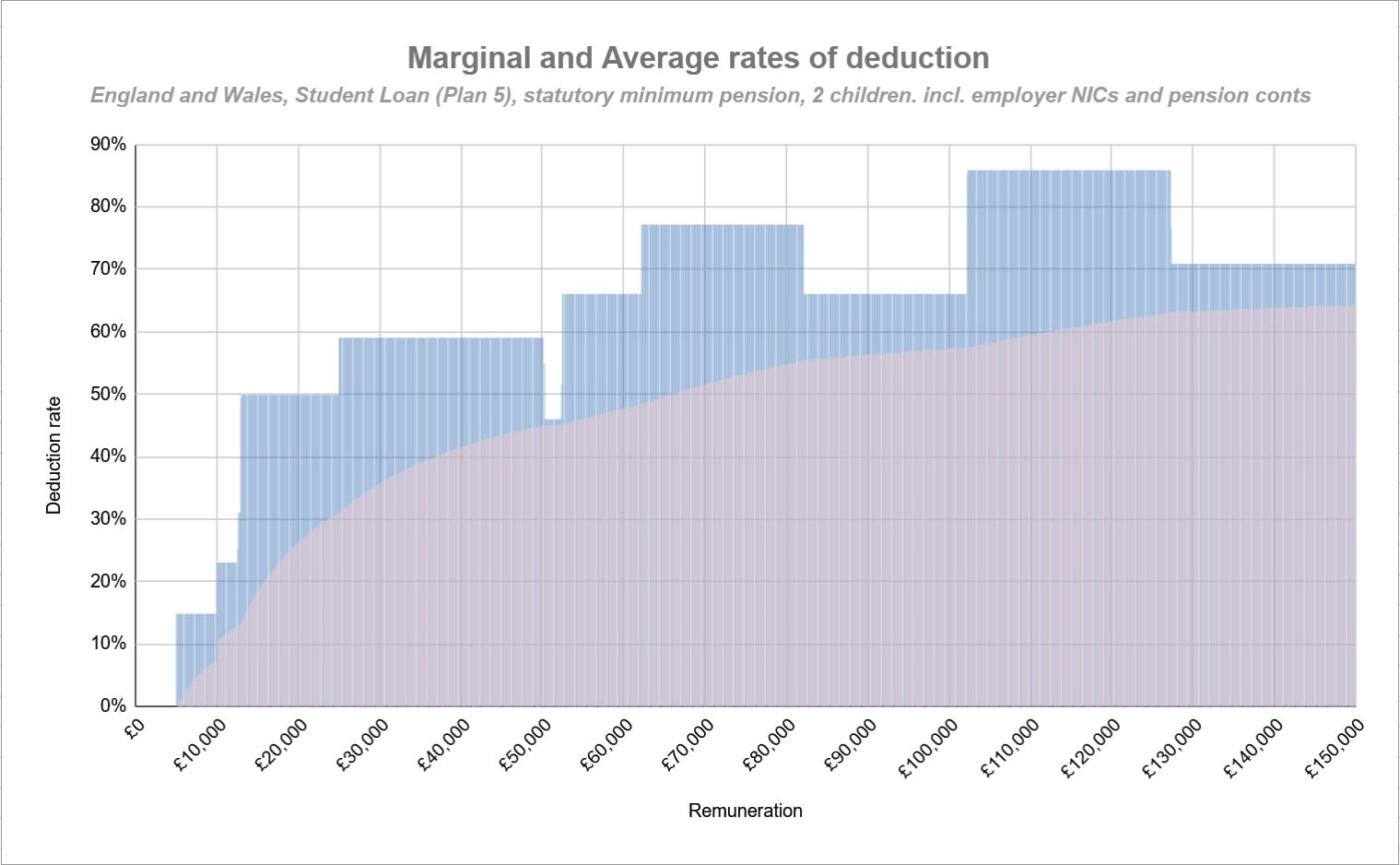

I think just looking at Income Tax and Employer National Insurance gives a very partial picture, given there are quite a few statutory deductions from payments made to employees:

- Income Tax (including tapering)

- Employee National Insurance

- Employer National Insurance

- Employer pension contributions

- Employee pension contributions

- Student loan deductions

- Child Benefit reduction

If you consider that the employee effectively pays all of the above from the total monies dedicated to them by the employer, you get the following chart:

Even someone earning just £30,000 pays an effective marginal rate of:

- 20% income tax

- 8% employee National Insurance

- 15% employer National Insurance

- 3% employer pension contribution

- 4% employee pension contribution (assume relief-at-source)

- 9% Student Loan repayment

Whilst some of those service a debt, or build up a pension, they are nonetheless deductions. Whilst an employee could opt-out of the pension, in practice only about 10% do that.

With fiscal drag added on top, that is a lot of deductions to overcome just to keep net earnings increasing in line with inflation. Employers are going to be hard pressed to award salary increases of a sufficient increase to enable that to happen.

The above doesn't take into account any means-tested benefits, notably Universal Credit. If that was included, the effective marginal deduction rate would be over 50% across the entire income spectrum (other than the tiny portion just above £50,000 subject to only 20% income tax and 2% employee NICS due to pension contributions).

0 -

I am not sure that is correct.

Using your example of £30k salary, summing all the percentages would amount to a marginal rate of 59%.

However, not all of those elements are funded from the employee's £30k. The other elements are additional costs to employ above the £30k incurred by the employer.

20% income tax = paid by employee

8% employee National Insurance = paid by employee

15% employer National Insurance = extra cost to employ

3% employer pension contribution = extra cost to employ

4% employee pension contribution (assume relief-at-source). = paid by employee

9% Student Loan repayment. = paid by employee

The deductions from the employee's £30k are 41%, not 59% so less tabloid click bait scaremongering headline .

Not everyone has student loan deductions.

3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards