We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

US Markets Risk

Comments

-

It wasn't difficult to achieve in the last 12 months, as a target for every year, I would say it will be "challenging".

2 -

I have no doubt about that. But it helps enormously to have a strategy and an approach that has been sucessfully tested and also execution experience of it, spanning a few years. Everyone should have targets, endlessly trying to invest to make money, without that target and a strategy, is counterproductive.

0 -

I don't have a target in terms of a percentage return I aim to see on a year to year basis, because that would just lead to inevitable disappointment.

A 10 year real return "aim" may make sense, and I have in my mind a target for that, but it is not something that leads me to fixate on the short term.

15% per year means quadrupling your money every 10 years, which is not achievable without considerable risk.

4 -

Target or aim, I think there needs to be a quantative value. I definitely fixate on the short term, aka one year intervals, what are you going to do at age 75 years, fixate on the 10 year plan, I don't think so……the way to eat an elephant is in small bites!

0 -

Ideally, what you should be doing at age 75, is benefiting from the long term retirement planning you set in motion decades ago and using the associated fixed income and/or risk off element of your portfolio allowing you to chill out and enjoy the rest of your life without worrying about the stock market.

My cash flow model shows that my retirement could survive with a 0% annual return going forward, assuming 2.5% annual inflation, but I model a return of 6% from a mix of 68% equities that are US and Tech heavy (but with some global and EM exposure) and 32% cash. I don't need to sell any equities for 8 years as I consume the cash first up to state pension payment commencing by when the extra draw down needed from the portfolio is much reduced. I don't worry about US exposure in my portfolio and accept that values will readjust when it gets frothy, as is has become lately. History also indicates there will be volatility and declines in US stocks in the run up to a mid term election but settle down after the seats in the houses are known.

2 -

If you have objectives with different time frames I would recommend that you run different portfolios each optimised for their particular role. In my (over 75) case guaranteed income together with the dividends and interest from my focussed income portfolio meet all foreseeable needs except perhaps future expensive holidays and long term care.

The separate 100% equity long term growth portfolio ensures that the size of the income portfolio can be increased to at least match inflation and the cash pot continues to meet known future large one-off expenses.

Hence there is no need to worry about short/medium term returns nor about significant falls in equity prices.. Continually fiddling with your portfolio in response to short term events takes time and effort, adds to stress, and overall has a high risk of being counter-productive. Fortunately it is not necessary.

4 -

"Ideally"….perhaps according to the text books and the FCA flyers, for the average person. We are alll very different, we have different finances, approaches and plans in mind for the future. My investment fund is a ring fenced play thing that I try to grow so I can leave it for my wife. Investing gives me pleasure, it's a challenge and its fun but what ever happens to that ring fenced pot, wont impact my retirement or my wifes eventual financial future, my income streams and financial assets are total separate. But I treat those funds and my investment process with the same respect that I would as if my day to day existence depended on it, which doesn't prevent me from taking risks, in a structured and limited manner.

0 -

The person holding a 50/50 mix of HSBC FTSE All world and an MMF would also have exceeded a target of 12% in the 7 months after April 2025 (28.9% return for equities and 2.5% return for the MMF) with a portfolio return of 15.7%.

I didn't say it is easy to make 15%, but that making 15% in 2025/26 has been easy since global equities have so far returned about 28% (note the tenses!).

Over 150 years, the US stock market (a highly successful market!) has had an annualised nominal $ total return of 9.3%, but there have been periods where growth has been significantly less - e.g., between end of 1999 and 2010 there was a nominal annualised return of 0%. In some decades an annualised return of 12% was met, in some it was not and therefore, in some decades your target will be met and in some not. I would argue that in the face of such variability there is little/nothing that you can do to ensure meeting your target.

My other point was that with all your predictions and careful selection of funds so far in 2025/26 you have essentially matched the performance of a simple 2 fund portfolio with a similar allocation to equities so could have saved yourself time and effort.

Finally, I spent a good part of my career looking at the effect of random and non-linear phenomena on engineering systems. While the failure rate and mean time between failure of such systems can be measured/modelled and future performance predicted, even where the underlying physics is well known, the time of the next failure cannot be predicted. Applying the knowledge that random systems are effectively unpredictable to the problem of funding my retirement has resulted in a solution where our reliance on income from our risk portfolio (i.e., equities, bonds, etc.) has been reduced by ensuring a solid floor in guaranteed income (e.g., DB pension, SP, an inflation linked gilt ladder - although all these are not without their own risks, together with term life insurance). We withdraw a percentage of our portfolio (broadly similar to the bogleheads VPW approach) - overall in good years we have a bit more money to spend and in bad years a bit less, but we are not reliant on meeting any particular target return (although I'd quite like the real return to be higher than 0%).

edit: I note your reply (the post above this one) about the investment pot you're talking about here being solely for legacy purposes and investing being enjoyable.

3 -

"My other point was that with all your predictions and careful selection of funds so far in 2025/26 you have essentially matched the performance of a simple 2 fund portfolio with a similar allocation to equities so could have saved yourself time and effort".

Hindsight is a wonderful thing of course, had I realised at the outset that might be the case, perhaps I may have not bothered with it all. But since I prefer a manual gearbox to an automatic, I suspect I probably would have, regardless! I'm certain that if I would have gone the two fund route, I would have learned only a fraction of what I did by choosing the more labour intensive route. Had I gone with index trackers, I am certain I would never beat the index. By going with managed funds I may not match the index but I do have a chance at beating it….and so I have, with most funds. Talking of labour intensity and effort….I help manage a family business here in Asia that comprises large scale rice production and 3.7 crops per year. Given the choice between sifting funds on Morningstar and being out in the fields in 44 degrees C, Morningstar wins hands down, every time.

0 -

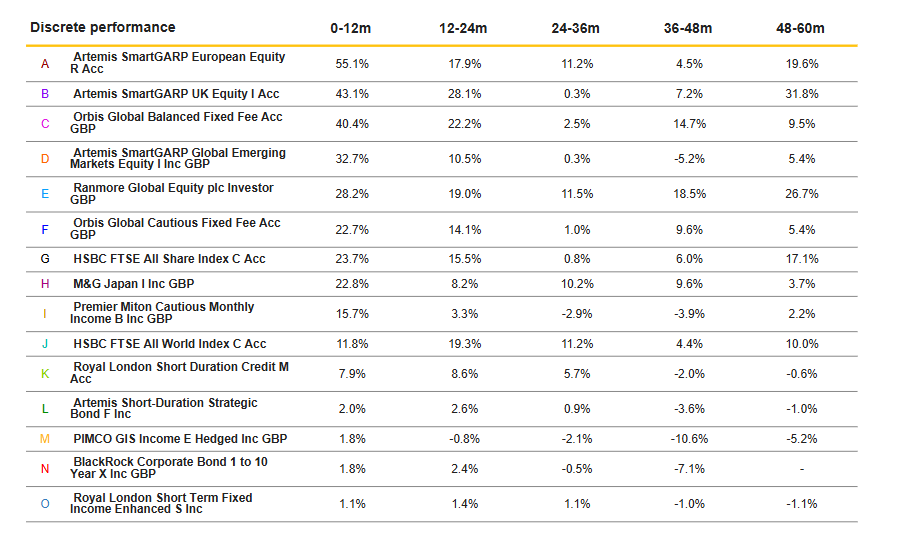

For interests sake, the following funds comprise my portfolio, mostly since April last year, some swaps were made early year:

1

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards