We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

I think I've finally cracked why most people don't invest in the stock market

In the UK only 23% of people invest in the stock market outside of their pensions. I think I've identified 3 key reasons for this, and not having money to invest isn't one of them.

1, They don't learn about compound growth and think £200 a month isn't worth it.

They think in a short term linear fashion like £200 x 12 = £2,400, even after 30 years it's only £72,000. Barely life changing, this isn't going to make me rich, it's pointless I'd rather just spend £200 a month now.

But £200 a month (increased by 3% per year for pay rises) @ 9 % compound growth for 30 years = £450,000.

2, They think investing is complicated and you need a degree to do it with 5 computer screens open with flashing prices, buying and selling trading in and out.

They don't know that global index funds exist. They think investing means picking 1 or a few companies and dumping your life savings in and hoping for the best. In reality almost every investor dollar cost averages, meaning they buy every month consistently with their pay check.

3, They are scared of losing their money because they think the stock market is like a roulette table.

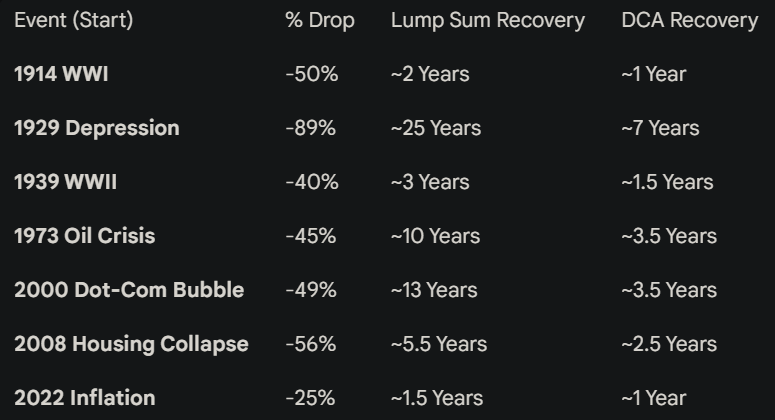

They don't realise that dollar cost averaging into a global index fund is incredibly safe over a long time period and in the entire history of the stock market, the longest it has ever remained in the red was 7 years and that was 1929 - 1936, known as the great depression.

DCA'ing into the global stock market drastically reduces the time you stay in the red compared to one time lump sum investing.

The average bear market for someone dollar cost averaging is a meagre 3 years give or take. And they're going to be investing for like 30 years...

So basically they just never bother to start due to all or some of the above reasons. And don't give me the "they don't have money" line because most people who work do have money left over, but they put it in a savings account or just blow it on useless crap they don't really need.

Comments

-

I'll add another

The vast majority of money invested in the stock market is by individuals with insider knowledge / more data.

Unfortunately the TikTok Generation is wowed by Gold and Crypto.

0 -

"just blow it on useless crap they don't really need."

Maybe some people enjoy spending rather saving😉

Things that are different: draw & drawer, brought & bought, loose & lose, dose & does, payed & paid1 -

Isn't the reason that stocks and shares are a good investment that the companies who make up the market's value continue to grow because people continue to spend on "useless crap" (and presumably other things neither useless nor crap)?

4 -

Ponzi scheme

0 -

But why does it have to be a binary option? Why can you not spend on things you enjoy but also invest a bit for retirement?

I never understood the mindset of those or think "it's either 100% saving 0% fun or 100% fun 0% saving"

0 -

We see many threads on the Savings & Investment Forum, along the lines ' I have just inherited £100K and do not know what to do it, but I'm not interested in stocks and shares as I am risk averse' In fact not investing is actually a risk in itself. Many also are actually invested via their DC pensions, but do not realise it, or somehow think that is different.

Another misunderstanding, is that now is not the right time due to 'everything going on in the world' . As if there have never been previous times of global instability, wars etc. In any case financial markets often shrug off bad news, and are generally more concerned with company profits forecasts and the like.

Just a couple of comments on the OP.

Drip feeding money into investments, may reduce the number of years in the red, but lump sum investing should get you a better long term result. The reason is simple. Stock markets go up more than they go down, so statistically it is better to add as much as possible as soon as possible. Problem is you might be one of the unlucky ones and you just might get the timing wrong.

Global index funds - These for sure are often the recommended investment for the long term, but only if you have the nerve to sit out the bad times. Many people would panic if their investment lost 30% in a couple of weeks, and with the media screaming about financial Armageddon, markets still crashing etc. they may well pull out nursing a big loss and miss out on the inevitable recovery. So for most investors, something a bit less racy is more suitable, such as a multi asset fund, with 50% to 80% equity, rather than 100%.

For the same reason pension default funds are normally not 100% equity.

2 -

Which is why dealing/trading in individual company shares is not recommended for the inexperienced.

Index funds that just follow the market, need zero expertise, or insider knowledge. The only thing you have to do is hang on long term ( ideally >10 years) .

0 -

I agree with the lump sum detail you mentioned, but this is where psychology plays a massive part. Psychologically investing £10,000 and the market dumping 20% in the first 6 months is definitely going to make people doubt their decision, you're down £2k in 6 months…

But investing from your pay check every month builds the pot slowly, it also gives you a sense of "at least I'm getting a discount" when the market drops 20% and you still have money to buy more.

1 -

I had endowments and they didn't do very well, then had an S&S ISA and that didn't do very well either. my money is in a cash account now - not risking it again

1 -

This doesn't sound like a praise, vent or warning.

My money is mine (and OH's) to spend/save as we wish.

But just FTR, we have invested in stocks & shares for many years.

I retired aged 50, OH at 52.

I've bought gold and silver jewellery over the years because I liked it.

My purchases have turned out to be very profitable.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards