We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

HL SIPP Track the market vs Expert Managed

Comments

-

Totally agree. It made us to be the proverbial ducks * as it is not something we wanted to repeat having lived it but still unfortunately rather uneducated in investment knowledge but yes partly through fear more than anything.Albermarle said:

If you ask around, you will find a large majority of the public has a pitiful level of knowledge about personal finance, regardless of their background.sometime_soon said:

You are absolutely right but it is something that really depends on your exposure to finance from a young age. For me and certainly many others, a non existent or very low income family and debt collectors being a way of life as children , just getting out of school with a job was a bonus and this reflects your caution and lack of knowledge for a long time. Education in these matters would benefit many but that’s a whole other discussion!! For now I try to learn more at a rather late stage.Bostonerimus1 said:

I know that this is an ionic remark, but I think it's important to dispel any idea that investing and personal finances needs to be complicated. All you need is basic mathematics like percentages and some understanding of probability - there's no need for eigenfunctions or matrices. Just the mention of investing can intimidate many people and given the way pensions and ISAs are structured that isn't a good thing.sometime_soon said:

Thankyou for that. I am very new to this and probably should start with something easier like Quantum or Theoretical Physics before I move on to understanding this and investments! But joking aside it is a valuable forum and giving me a lot to research and learn .dunstonh said:

What do you mean by expert managed?sometime_soon said:As above. Obviously fees are much higher so just wondered what, if any, people’s experience has been and if they felt it had been worth it or not? ( Appreciate fund size and many other factors come in to play but as a simplistic experience!)

IFA, MPS, Fund house?

Would that management be underlying passive but management on the weightings?

Or is it full managed (funds and selection)?

What do you mean by track the market?

Passive funds with you making the weightings decisions?

Multi-asset funds making the weightings decisions?

Market cap or one of the many variatons possible?

Are you looking specifically at an HL own brand option or a different fund house?

HL platform plus HL own brand charges actually puts your total costs near full advice terrirtory (e.g. HL platform 0.45% + 0.3% OCF = 0.75%. IFA at 0.50%, platform at 0.15% and OCF 0.16% = 0.81%. (can be cheaper, can be more expensive depending on your instructions to the IFA. Indeed, the one I saw on Friday has a total 0.76%).

DIY is best when you achieve the same or a similar outcome without the costs. If you go DIY in any area of life, you usually do it to lower your costs. A good job and good DIY is a good outcome. Bad DIY, which can be bad decision-making or using higher cost options, is not a good outcome. It could range for sub-optimal and still getting away with it through to disastrous decisions.

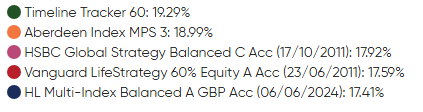

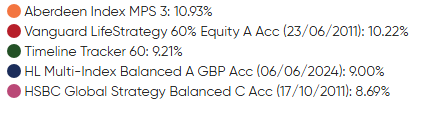

Here is the performance of HL's Balanced version since launch vs a couple of IFA options and OEIC versions all using passives.

If we look at the period when US more or less switched from being best to worst:

You see that one of the best options since 2011 (HSBC) is bottom now.

What is strange is that HL is bottom/near bottom in both periods. Upper has more of the period when US was best. Lower has more of the period when US was worst. So, a portfolio with a higher US weighting did better when the US was best but not as well when US underperformed. HL managed to be bottom or near bottom in both periods. (it is a short list, many fund houses and MPS have variants and HL could be better than some or many of those but I just selected from two of the popular IFA MPS and DIY Multi-asset funds).

If is worth noting that all of those are managed funds or managed portfolios. They all have underlying passive strategies (tracking the market), but the asset weightings, adjustments between them, and how they are rebalanced are management decisions.

Of course if your parents are interested in it and give you a basic grounding, that is bound to be a big help.

However not sure how much income comes into it. We have posters on here earning £150K pa who are pretty clueless about savings, pensions, or even how much tax they are paying.

On the other hand sometimes having a poor background can make people very mindful of money when they grow up.0 -

If you are living your life without getting into massive debt, and are keeping track of your income and spending you are doing better than many.Don't be afraid of asking questions here. People will often ask for more information, in order to give answers that are as helpful as possible.What you get will only be guidance, not advice, so always think about what you read, and decide for yourself if it does or doesn't apply to you. There are many very knowledgable people here, some who have an axe to grind and some (like me) who want to help, but sometimes still get things wrong (but get swiftly corrected!).0

-

I think that be biggest obstacle to understanding and then controlling your personal finances is the dogma that it has to be complicated. There are lots of people who make lots of money off people who are intimidated by a narrative that is perpetuated by many vested interests.sometime_soon said:

You are absolutely right but it is something that really depends on your exposure to finance from a young age. For me and certainly many others, a non existent or very low income family and debt collectors being a way of life as children , just getting out of school with a job was a bonus and this reflects your caution and lack of knowledge for a long time. Education in these matters would benefit many but that’s a whole other discussion!! For now I try to learn more at a rather late stage.Bostonerimus1 said:

I know that this is an ionic remark, but I think it's important to dispel any idea that investing and personal finances needs to be complicated. All you need is basic mathematics like percentages and some understanding of probability - there's no need for eigenfunctions or matrices. Just the mention of investing can intimidate many people and given the way pensions and ISAs are structured that isn't a good thing.sometime_soon said:

Thankyou for that. I am very new to this and probably should start with something easier like Quantum or Theoretical Physics before I move on to understanding this and investments! But joking aside it is a valuable forum and giving me a lot to research and learn .dunstonh said:

What do you mean by expert managed?sometime_soon said:As above. Obviously fees are much higher so just wondered what, if any, people’s experience has been and if they felt it had been worth it or not? ( Appreciate fund size and many other factors come in to play but as a simplistic experience!)

IFA, MPS, Fund house?

Would that management be underlying passive but management on the weightings?

Or is it full managed (funds and selection)?

What do you mean by track the market?

Passive funds with you making the weightings decisions?

Multi-asset funds making the weightings decisions?

Market cap or one of the many variatons possible?

Are you looking specifically at an HL own brand option or a different fund house?

HL platform plus HL own brand charges actually puts your total costs near full advice terrirtory (e.g. HL platform 0.45% + 0.3% OCF = 0.75%. IFA at 0.50%, platform at 0.15% and OCF 0.16% = 0.81%. (can be cheaper, can be more expensive depending on your instructions to the IFA. Indeed, the one I saw on Friday has a total 0.76%).

DIY is best when you achieve the same or a similar outcome without the costs. If you go DIY in any area of life, you usually do it to lower your costs. A good job and good DIY is a good outcome. Bad DIY, which can be bad decision-making or using higher cost options, is not a good outcome. It could range for sub-optimal and still getting away with it through to disastrous decisions.

Here is the performance of HL's Balanced version since launch vs a couple of IFA options and OEIC versions all using passives.

If we look at the period when US more or less switched from being best to worst:

You see that one of the best options since 2011 (HSBC) is bottom now.

What is strange is that HL is bottom/near bottom in both periods. Upper has more of the period when US was best. Lower has more of the period when US was worst. So, a portfolio with a higher US weighting did better when the US was best but not as well when US underperformed. HL managed to be bottom or near bottom in both periods. (it is a short list, many fund houses and MPS have variants and HL could be better than some or many of those but I just selected from two of the popular IFA MPS and DIY Multi-asset funds).

If is worth noting that all of those are managed funds or managed portfolios. They all have underlying passive strategies (tracking the market), but the asset weightings, adjustments between them, and how they are rebalanced are management decisions.

I learned by first financial lessons literally at my mother's knee. She would take my father's pay packet and give him some weekly spending money. She never bought anything on "hire purchase" and put money into a bank saving account each week. There was really no access to other investments, but they weren't that necessary as my father had a DB pension. So I learned frugality and as I ended up in a job that was heavily reliant on maths I wasn't intimidated by personal finances...that was doubly so after seeing the bottom of my university class get jobs at Arthur Anderson and Solomon Bros.And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

Keep reading these forums, it is a good way to learn .

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards