We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Help with knowing how much is 'needed' to retire?

Comments

-

Sorry if this sounds like I'm being pedantic, but I'm not a fan of the term unaffordable, as it implies there is a single point before which it is affordable and after which it is not. In the context of public expenditure, affordability is somewhat vague as the government can almost always rob from Peter (e.g. increase taxes/cut NHS spending) to pay Paul (e.g. maintain Triple Lock) - depending on their priorities.michaels said:

Fiscal drag means govt revenues go up faster than average incomes or prices so if the triple lock is unaffordable it will be due to demographics rather than pension increases - and increases to the spa help to protect against some of the impacts of demographics.Exodi said:

People often prefer to resort to ad hominem attacks like that or deliberately misrepresenting what is being said as opposed to having a constructive conversation on the triple lock on this forum. But credit where it's due, there are also many others that acknowledge that it's unsustainable.LHW99 said:Veloflyer said:

For sure younger folk can plan - as long as they are aware of the issues. I am not sure the vast majority are, or are even aware of the need to have a pension to supplement the SP - assuming it even exists in the next 30/40 years. I also appreciate many cannot also afford to supplement it.kempiejon said:State Pension seems a long way away when you're in your 30s, my first pension had started by my 22nd birthday, but it was in my 30s that there was a real plan, it was a 15+ year plan but state pension never factored as I wanted early retirement. The early bit is the clue there. SIPPs are not accesible until 55, SP not for another 12 years. Younger folk can plan, I am lucky not to be too dependant on SP, my retirement plan was separate to the SP, If I get to 67 let's see.

Compared with younger folk, I consider myself extremely fortunate to be in the position I am in with regard to pensions.While I can't see the state pension being abolished, even if the triple lock goes, it is not only the Mail readers who appears to be considering the possibility

Like you, I also can't see the state pension being completely abolished, I can however see it being scaled back - whether that's means testing, increasing SPA more than life expectancy, increasing minimum auto-enrollment contributions and reducing SP, etc. Especially if politicians continue to feel they don't have the political capital to end the triple lock in the future.

Unfortunately this forum is not the place to have a balanced conversation on this, as mentioned earlier the forum demographic skews much older and there are more retirees than workers. Naturally you can expect to have a bias for maintaining the triple lock, which is what we often see.

I would certainly agree that young people of today should consider the worst case scenario that they won't have a state pension, as JP Morgan suggests in that article.

I'm also not a fan of framing it that increasing spending is down to either the triple lock or demographics - obviously these things aren't mutually exclusive. Both will clearly have a significant impact, particularly over the long term.

On fiscal drag since I see you've mentioned it a few times - I think the basis of your argument hinges on fiscal drag continuing over the long term?

It's also a very awkward way to maintain the triple lock as not only does it upset pensioners due to the optics (who already have their nose out of joint it at the potential of paying income tax on their state pension - with some seeing it as being taxed twice), but let's not forget it simultaneously crushes workers by ever-increasing their effective tax rate. As mentioned earlier, I suspect we're already over the peak of the Laffer curve, of course that is subjective.

I suspect most would prefer that the tax allowances were unfrozen but the triple lock scrapped in place with a link to inflation or earnings (and it can be smart, e.g.as often suggested by various pension thinktanks, one does not decrease but instead balances on the next increase to the tracked metric).

That said, we're not all rational, and after the pandemonium caused around the WFA, I suspect that any politician daring to mention the the triple lock will undoubtedly find an army of pensioners with pitch forks at their door. It is a political problem, not an economical one - the economics are fairly simple, it is by its nature unsustainable. Politically the mistake was introducing it without a plan for phasing it out.

Due to this, I fear that we are destined to inertia and to follow in Frances steps.

Thanks for editing in the data, it's a pet peeve of mine when someone tells me to look up data for them!michaels said:Can you show us some figures for what share of GDP SP

(...)

A quick google suggests the state pension share of GDP is likely to go from 5% to 8% of GDP over the next 50 years under the triple lock.

I think this highlights how far apart we are on this issue - I am surprised you don't see these numbers as anything short of alarming.

Out of interest, why do you consider these things through the lens of GDP? Why not government revenues, from which the state pension is paid? Since we are talking about sustainability/affordability.

Unless by using GDP you're implying the government could increase taxes?

Also my apologies I missed this thread a bit but I wanted to loop back to an earlier suggestion of yours:In 2024/25, the UK government raised approximately £1,139 billion (£1.139 trillion) equivalent to about 39% of GDP.

https://commonslibrary.parliament.uk/research-briefings/cbp-8513/

I can see how that will improve finances, however from a moral standpoint, it's deeply unfair.michaels said:

If they fix the number of retired years rather than the ratio of working to retired years then increasing longevity will improve finances.

The SPA today is 66 and the average life expectancy is ~83. Someone working from 18 to 66 will pay in for 48 years and claim state pension for 17 years (~20.5% of their life). Each year they worked 'earned' them about a 35% of a year of SP.

If life expectancy in the future were to increase 10 years to 93, to maintain a fixed number of years of retirement, the government would need to set SPA to 76. This would mean someone working from 18 to 76 will pay in for 58 years and claim state pension for 17 years (~18.3% of their life). Each year they worked 'earned' them about 29% of a year of SP.

It would only get worse the further life expectancy increases.

Again it would be a awkward solution (making people work longer and longer so that the triple lock can be maintained over the long term, so they can live the life of riley in retirement). I know what I'd pick if given the choice and I suspect I suspect I know what you would chose if the shoe was on the other foot and you were fresh out school just about to begin your working life.

Know what you don't2 -

A few comments.

Increasing the govt take from 39% of GDP to 42% over 50 years would not be unprecedented. Don't forget in theory with 'normal' GDP per head growth, everyone would still see a large increase in real income per head. Also pensioners pay an increasing proportion of their income in tax (the 10 years and counting threshold freeze) so a fair chunk of that extra tax will come from pensioners not workers.

In terms of retirement age, we are both talking about ways to limit the liability, you are suggesting a lower pension over more years, I am suggesting a higher pension for fewer. With the lower pension it then becomes at a level where the taxpayers top it up via pension credit so no real savings there....I think....1 -

To be honest, I'm not convinced - we haven't yet crossed the point that pensioners are liable to pay tax on their state pension. I did see a fair bit of uproar on social media when Martin Lewis mentioned it will happen in 2027/28. I'll be interested to see how this plays out.michaels said:A few comments.

Increasing the govt take from 39% of GDP to 42% over 50 years would not be unprecedented. Don't forget in theory with 'normal' GDP per head growth, everyone would still see a large increase in real income per head. Also pensioners pay an increasing proportion of their income in tax (the 10 years and counting threshold freeze) so a fair chunk of that extra tax will come from pensioners not workers.

The government hasn't made their stance totally clear on this either:

Also on -In the 2025 Budget the government announced the personal allowance would be frozen at its current level up to April 2031. It also announced that pensioners whose sole income is the basic or new state pension would not have to pay small amounts of tax via simple assessment from 2027/28 if the new or basic state pension exceeded the personal allowance from that point. To date the government has not published any further details of how this is to be done.

https://commonslibrary.parliament.uk/research-briefings/cbp-10250/

Indeed, we are both talking about ways to limit liability, and I accept that it can be a false economy with pension credit (I think that needs a separate discussion on it's own), though I would question the necessity of 'a higher pension for fewer [retirement years]' given that the longer people work, the more private pension provision they are likely to accumulate - or to put it another way, the later you force people to retire, the less likely they are to need a relatively bigger state pension.michaels said:In terms of retirement age, we are both talking about ways to limit the liability, you are suggesting a lower pension over more years, I am suggesting a higher pension for fewer. With the lower pension it then becomes at a level where the taxpayers top it up via pension credit so no real savings there....

Know what you don't1 -

And as we know from many examples on these forums, no one is actually forced to retire at SPA nowadays. They can do so before (or after) providing they have their own provision, which autoenrollment should / can hopefully help with.Exodi said:

To be honest, I'm not convinced - we haven't yet crossed the point that pensioners are liable to pay tax on their state pension. I did see a fair bit of uproar on social media when Martin Lewis mentioned it will happen in 2027/28. I'll be interested to see how this plays out.michaels said:A few comments.

Increasing the govt take from 39% of GDP to 42% over 50 years would not be unprecedented. Don't forget in theory with 'normal' GDP per head growth, everyone would still see a large increase in real income per head. Also pensioners pay an increasing proportion of their income in tax (the 10 years and counting threshold freeze) so a fair chunk of that extra tax will come from pensioners not workers.

The government hasn't made their stance totally clear on this either:

Also on -In the 2025 Budget the government announced the personal allowance would be frozen at its current level up to April 2031. It also announced that pensioners whose sole income is the basic or new state pension would not have to pay small amounts of tax via simple assessment from 2027/28 if the new or basic state pension exceeded the personal allowance from that point. To date the government has not published any further details of how this is to be done.

https://commonslibrary.parliament.uk/research-briefings/cbp-10250/

Indeed, we are both talking about ways to limit liability, and I accept that it can be a false economy with pension credit (I think that needs a separate discussion on it's own), though I would question the necessity of 'a higher pension for fewer [retirement years]' given that the longer people work, the more private pension provision they are likely to accumulate - or to put it another way, the later you force people to retire, the less likely they are to need a relatively bigger state pension.michaels said:In terms of retirement age, we are both talking about ways to limit the liability, you are suggesting a lower pension over more years, I am suggesting a higher pension for fewer. With the lower pension it then becomes at a level where the taxpayers top it up via pension credit so no real savings there....

1 -

You're right and it's a point I'm all too familiar with at work (we have an aging work force like every one which makes long term labour planning difficult), but I don't see how it's relevant in the context of what we were discussing.LHW99 said:

And as we know from many examples on these forums, no one is actually forced to retire at SPA nowadays. They can do so before (or after) providing they have their own provision, which autoenrollment should / can hopefully help with.Exodi said:

To be honest, I'm not convinced - we haven't yet crossed the point that pensioners are liable to pay tax on their state pension. I did see a fair bit of uproar on social media when Martin Lewis mentioned it will happen in 2027/28. I'll be interested to see how this plays out.michaels said:A few comments.

Increasing the govt take from 39% of GDP to 42% over 50 years would not be unprecedented. Don't forget in theory with 'normal' GDP per head growth, everyone would still see a large increase in real income per head. Also pensioners pay an increasing proportion of their income in tax (the 10 years and counting threshold freeze) so a fair chunk of that extra tax will come from pensioners not workers.

The government hasn't made their stance totally clear on this either:

Also on -In the 2025 Budget the government announced the personal allowance would be frozen at its current level up to April 2031. It also announced that pensioners whose sole income is the basic or new state pension would not have to pay small amounts of tax via simple assessment from 2027/28 if the new or basic state pension exceeded the personal allowance from that point. To date the government has not published any further details of how this is to be done.

https://commonslibrary.parliament.uk/research-briefings/cbp-10250/

Indeed, we are both talking about ways to limit liability, and I accept that it can be a false economy with pension credit (I think that needs a separate discussion on it's own), though I would question the necessity of 'a higher pension for fewer [retirement years]' given that the longer people work, the more private pension provision they are likely to accumulate - or to put it another way, the later you force people to retire, the less likely they are to need a relatively bigger state pension.michaels said:In terms of retirement age, we are both talking about ways to limit the liability, you are suggesting a lower pension over more years, I am suggesting a higher pension for fewer. With the lower pension it then becomes at a level where the taxpayers top it up via pension credit so no real savings there....

We were discussing about whether people would prefer an increasingly deferred state pension in exchange for continuining the triple lock (or in essence, a smaller state pension earlier, or a bigger state pension later). I pointed out that a bigger state pension later may not be logical as the longer people work, the more private provision they accumulate (which is essentially what you've said). Unless you were agreeing with me, I can't tell.

My apologies, my heads all over the place today!Know what you don't0 -

ummm...

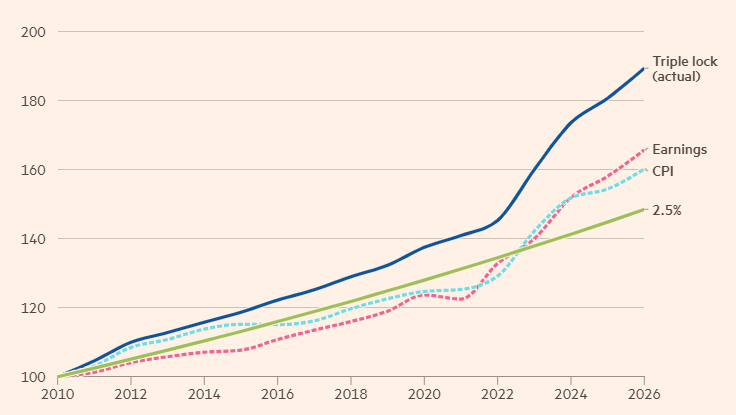

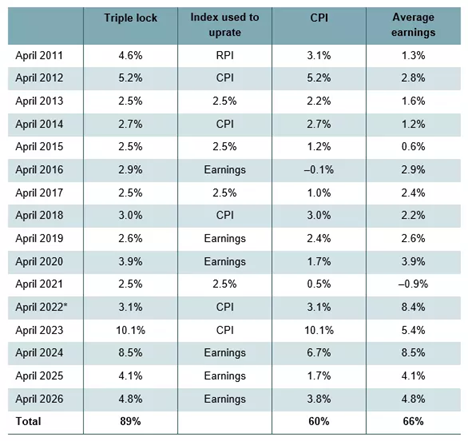

as I understand it the Triple lock increases the State Pension by largest of CPI, earnings or 2.5% - so the only time it will wildly increase in real value is if inflation is close to zero so outstrips it by 2.5% (very rare) or maybe if wage inflation is huge as post Covid (when TLwasn't applied anyway). The argument that this isn't sustainable is effectively the same as saying ANY state provision is unsustainable, not that the TL is massively over generous.

If we vote in a Government that does away with the State pension then more fool us. But don't believe teh argument that the Triple Lock is some sort of massive money shedding exercise, it ain't.0 -

agree with tigerspill above.I calculate my weekly expenses , multiply by 52, fetch my dividend rate currently 12.52%, and end up with...8*yearly expenses = amount of yearly dividend i need to cover .My pensions currently producing 292% of my yearly expenses just in dividends, so i'm probably going to be ok when retirement day rolls around.0

-

Why does it need to 'wildly increase' in a single year for it to be a problem? Surely the problem is one of sustainability and that it increases by more than earnings and inflation over the long term.ClashCityRocker1 said:ummm...

as I understand it the Triple lock increases the State Pension by largest of CPI, earnings or 2.5% - so the only time it will wildly increase in real value is if inflation is close to zero so outstrips it by 2.5% (very rare) or maybe if wage inflation is huge as post Covid (when TLwasn't applied anyway).

But we don't need to rely on gut-feel, it's relatively easy to find data comparing the difference between the triple lock and each single lock equivalent - see below for convenience.

https://www.ft.com/content/9baeb1d0-3c38-4c11-8973-54633552af7d

You mention the scenario that inflation and earnings are close to zero so there is a 2.5% delta (such as in 2021), but you forget some of the other major issues that can occur (some of which only happened a few years ago).

For example and perhaps the biggest issue was the rapid inflation caused by spikes in energy prices (among other things) stemming from the war in Ukraine, causing a CPI figure of 10.1% - this then led to a CPI based triple lock increase in 2023.

The following year, when employees started receiving pay increases to meet rapidly increasing mortgage/food/energy/etc bills (leading to the infamous Andrew Bailey moment where he asks employers to show 'restraint' in giving pay rises), the triple lock then double dips by linking to earnings instead.

https://ifs.org.uk/articles/what-are-effects-triple-lock-and-how-could-it-be-reformed

I'm not sure whether your latter point about the TL (not being applied) is disingenuous, but the reason it wasn't earnings linked in Apr 2022 was solely because the assessment period coincided with the unwinding of the furlough scheme, meaning people were going from (reduced) furlough pay back to full pay - which looked on paper like an incredible increase in earnings, but in reality employees were just returning to normal pay. To uprate the state pension in line with that increase would have been incredibly daft, hence parliament temporarily removed the earnings component.

Textbook example of false equivalence.ClashCityRocker1 said:The argument that this isn't sustainable is effectively the same as saying ANY state provision is unsustainable, not that the TL is massively over generous.

Obviously any state provisions can be sustainable if they increase sustainably (e.g. in line with revenue). State provisions are not sustainable if they continue to increase more than revenues - which is what the triple lock is inherently designed to do.

Agreed - and again as I've repeated several times, no-one is suggesting the government would 'do away with the state pension', this seems to a strawman that keeps getting brought out in these discussions.ClashCityRocker1 said:If we vote in a Government that does away with the State pension then more fool us.

My fear is that if successive governments feel they do not have the political capital to end the triple lock, then they will instead look at limiting the SP liability - whether that's increasing SPA, means-testing, etc. I don't think for one second that any government would just totally cancel the state pension and I don't think any one has suggested that.

Likely they could try to pass the burden onto employers by increasing mandatory minimum contributions to workplace schemes and in tandem reduce SP liability on younger people.

Or ideally, just end the triple lock - but obviously not popular with pensioners in receipt of the state pension, and as we all know, those are the ones that actually vote.

We're all clear on what it is - a bribe for the grey vote, hence virtually all main political parties have commit to it despite being aware of its unsustainability (else lose to a party that does pledge to keep it).ClashCityRocker1 said:But don't believe teh argument that the Triple Lock is some sort of massive money shedding exercise, it ain't.Know what you don't2 -

"We're all clear on what it is - a bribe for the grey vote, hence virtually all main political parties have commit to it despite being aware of its unsustainability (else lose to a party that does pledge to keep it)."

Or an attempt to lift the state penson up to something comparable to other similar countries in Europe?

0 -

These are complex systems that are not easily comparable. For example, consider the fact that what you see as the more generous overseas pensions typically require higher social security taxes during working years and that you have not considered the position if income from all sources is included. Unlike many other countries, income from occupational and personal pensions are an important source of income in the UK.

Know what you don't0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards