We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Help with knowing how much is 'needed' to retire?

Comments

-

An interesting thread. To mangle Donald Rumsfeld somewhat - You retire with the money you have, not the money you might want or wish to have at a later time.

To explain perhaps. I am of the view that until the SP clears in my account, then it is just a concept. Many folk factor it into their plans and trust HMG to do what should be a fait accompli. I don't trust HMG one iota, and neither should anyone else.

Online calculators are a guide and nothing else. You need to understand their considerable limitations

Spend in retirement must be understood for planning purposes. I have done a dump of my annual spend from my online account, reformatted it into a simple Excel spreadsheet, modified it a wee bit, and used that as reasonable guide.

I paid off the mortgage years ago. It was a debt and costing me.

I am a firm believer in planning for the worst and hoping for the best. Granted this is also a bit of a mindset thing, but then once done, it removes considerable anxiety for the future, helps me sleep at night, greatly removes reliance on other people - who may not have your best interests at heart - and a reliance on future events you have no control over.

Any growth of funds during retirement is a bonus. I don't rely on it.

2 -

While it's important to have a plan B, it seems sensible to me to factor the SP into your long term plans.Some of the comments here seem almost prepper level paranoia.3

-

I'm confused about what you mean here, is that not effectively what is happening now? A SPA that increases in line with life expectancy?michaels said:I think you are being pessimistic on the maths. The govt can maintain the triple lock and simply keep the average number of years of receipt constant via the retirement age.

If everyone is getting the same number of average years in receipt, the triple lock would be unsustainable over the long term as it increases by more than earnings or inflation. To counterbalance it, you would need to effectively reduce the average number of years of receipt to balance the difference between the triple locked increases and average earnings (or, perhaps most obviously, end the triple lock).

That's not even considering the age demographics dramatically shifting. Checking ONS predications, 14.8% of the population in 2016 was 68 or order, in 2026 it's 16.9%, in 2036 it's 20.2%, in 2046 it's 21.5%, you get the idea.

https://www.ons.gov.uk/visualisations/dvc418/pyramids_projections/index.html#0/0/0/106/68/false/false/na/0

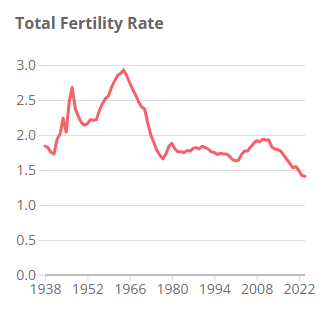

Some may argue that it's because people are living longer, which is only a very small part of it, the main problem is the declining birth rate, whereby we are now achieving new record lows every year. We have been below the net replacement rate for over 50 years.

https://www.ons.gov.uk/peoplepopulationandcommunity/birthsdeathsandmarriages/livebirths/bulletins/birthsummarytablesenglandandwales/2024refreshedpopulations

Given that we all know there is no state pension 'pot' and current retirees are paid from current tax receipts, it is inevitable the state pension in it's current iteration is not sustainable (I guess they could delay the inevitable by increasingly cutting public services and taxing the living smithereens out of workers, but even this would not work in the long term as I suspect we are already past the peak of the Laffer curve).

Know what you don't2 -

Depends if you trust HMG. I don't. In addition, and as mentioned above, the sustainability of the SP in it's present form is also highly questionable. I appreciate it is also a mindset thing. Each to his own there I feel.Tree_pipe99 said:While it's important to have a plan B, it seems sensible to me to factor the SP into your long term plans.Some of the comments here seem almost prepper level paranoia.0 -

The state pension is the bedrock of the majority of people’s plans. Higher earners may have the fortune to plan to have it as ‘bonus’ money but not the reality for much of the population. The triple lock has been in place for some time. Nothing lasts forever, hence the comparison to the TFLS. Legislation changes. When the TL goes, it will be replaced with something else. That may leave people ‘X’ worse off. The same as when my DB pension closed. It left me hundreds of thousands worse off in theory and I adjusted my plans.

Who knows what the future brings? The exact reason I work in today’s money and the increases I know, although FWIW I ignore the TL.Saving for the future, without suffering today is basic common sense. e.g. in my 50’s I live on less than I know I could retire on today but choose not to.

As for the Triple Lock in isolation. It will take some political shift and compromise elsewhere. They can’t even make the winter fuel allowance removal stick and Tory 2.0 won’t want to rock the boat, unless there is something like a big hike in the basic rate of tax threshold. Who knows? In the future the state pension could be means tested, like the WFA.1 -

I'd agree that the SP could be means tested. Indeed, I think it is highly likely - that, or they shove the retirement age out again. I don't rely on monies I don't have, especially if those monies are something I have no control over. I appreciate the SP is indeed a bedrock for most folks' plans, but I have never viewed it as such. Given the doubts over it's present viability, I'd argue that one should at least be prepared for being worse off in retirement if relying on it now for the future.Cobbler_tone said:The state pension is the bedrock of the majority of people’s plans. Higher earners may have the fortune to plan to have it as ‘bonus’ money but not the reality for much of the population. The triple lock has been in place for some time. Nothing lasts forever, hence the comparison to the TFLS. Legislation changes. When the TL goes, it will be replaced with something else. That may leave people ‘X’ worse off. The same as when my DB pension closed. It left me hundreds of thousands worse off in theory and I adjusted my plans.

Who knows what the future brings? The exact reason I work in today’s money and the increases I know, although FWIW I ignore the TL.Saving for the future, without suffering today is basic common sense. e.g. in my 50’s I live on less than I know I could retire on today but choose not to.

As for the Triple Lock in isolation. It will take some political shift and compromise elsewhere. They can’t even make the winter fuel allowance removal stick and Tory 2.0 won’t want to rock the boat, unless there is something like a big hike in the basic rate of tax threshold. Who knows? In the future the state pension could be means tested, like the WFA.0 -

I think the state pension will exist but more of it will be clawed back through the income tax regime. So if you only have state pension you will be able to keep most of it. Those who have made their own provision too will be hammered by higher income taxes.1

-

I’d say that approach is time linked though. It would be a shame if anyone (for example) aged 60 chooses to keep working (if they didn’t want to) if they have plans to bridge to the state pension. The same with lower earnings who don’t have an alternative.Veloflyer said:

I'd agree that the SP could be means tested. Indeed, I think it is highly likely - that, or they shove the retirement age out again. I don't rely on monies I don't have, especially if those monies are something I have no control over. I appreciate the SP is indeed a bedrock for most folks' plans, but I have never viewed it as such. Given the doubts over its present viability, I'd argue that one should at least be prepared for being worse off in retirement if relying on it now for the future.Cobbler_tone said:The state pension is the bedrock of the majority of people’s plans. Higher earners may have the fortune to plan to have it as ‘bonus’ money but not the reality for much of the population. The triple lock has been in place for some time. Nothing lasts forever, hence the comparison to the TFLS. Legislation changes. When the TL goes, it will be replaced with something else. That may leave people ‘X’ worse off. The same as when my DB pension closed. It left me hundreds of thousands worse off in theory and I adjusted my plans.

Who knows what the future brings? The exact reason I work in today’s money and the increases I know, although FWIW I ignore the TL.Saving for the future, without suffering today is basic common sense. e.g. in my 50’s I live on less than I know I could retire on today but choose not to.

As for the Triple Lock in isolation. It will take some political shift and compromise elsewhere. They can’t even make the winter fuel allowance removal stick and Tory 2.0 won’t want to rock the boat, unless there is something like a big hike in the basic rate of tax threshold. Who knows? In the future the state pension could be means tested, like the WFA.

Clearly the younger you are, the more change you are going to be faced with.0 -

If they fix the number of retired years rather than the ratio of working to retired years then increasing longevity will improve finances.Exodi said:

I'm confused about what you mean here, is that not effectively what is happening now? A SPA that increases in line with life expectancy?michaels said:I think you are being pessimistic on the maths. The govt can maintain the triple lock and simply keep the average number of years of receipt constant via the retirement age.

If everyone is getting the same number of average years in receipt, the triple lock would be unsustainable over the long term as it increases by more than earnings or inflation. To counterbalance it, you would need to effectively reduce the average number of years of receipt to balance the difference between the triple locked increases and average earnings (or, perhaps most obviously, end the triple lock).

That's not even considering the age demographics dramatically shifting. Checking ONS predications, 14.8% of the population in 2016 was 68 or order, in 2026 it's 16.9%, in 2036 it's 20.2%, in 2046 it's 21.5%, you get the idea.

https://www.ons.gov.uk/visualisations/dvc418/pyramids_projections/index.html#0/0/0/106/68/false/false/na/0

Some may argue that it's because people are living longer, which is only a very small part of it, the main problem is the declining birth rate, whereby we are now achieving new record lows every year. We have been below the net replacement rate for over 50 years.

https://www.ons.gov.uk/peoplepopulationandcommunity/birthsdeathsandmarriages/livebirths/bulletins/birthsummarytablesenglandandwales/2024refreshedpopulations

Given that we all know there is no state pension 'pot' and current retirees are paid from current tax receipts, it is inevitable the state pension in it's current iteration is not sustainable (I guess they could delay the inevitable by increasingly cutting public services and taxing the living smithereens out of workers, but even this would not work in the long term as I suspect we are already past the peak of the Laffer curve).

If the triple lock exceeds wage inflation then this just means that pensioners will get a larger share of rising GDP per head than workers do, is this really unsustainable?

But the Biggie is fiscal drag. Going forward most increases in state pension will be taxed at 20 or 40% Suppose between 2027 and 2031 state pension increases from 12570 to 13570 and that 800 of this increase is swallowed by inflation. The real cost of the 13750 after 200 tax is collected is zero, for a 40% tax payer the real cost after tax has fallen by £200.I think....0 -

I agree - especially to the latter, and the change will not be for the better. Younger folk especially need to be made aware so they can plan accordingly.Cobbler_tone said:

I’d say that approach is time linked though. It would be a shame if anyone (for example) aged 60 chooses to keep working (if they didn’t want to) if they have plans to bridge to the state pension. The same with lower earnings who don’t have an alternative.Veloflyer said:

I'd agree that the SP could be means tested. Indeed, I think it is highly likely - that, or they shove the retirement age out again. I don't rely on monies I don't have, especially if those monies are something I have no control over. I appreciate the SP is indeed a bedrock for most folks' plans, but I have never viewed it as such. Given the doubts over its present viability, I'd argue that one should at least be prepared for being worse off in retirement if relying on it now for the future.Cobbler_tone said:The state pension is the bedrock of the majority of people’s plans. Higher earners may have the fortune to plan to have it as ‘bonus’ money but not the reality for much of the population. The triple lock has been in place for some time. Nothing lasts forever, hence the comparison to the TFLS. Legislation changes. When the TL goes, it will be replaced with something else. That may leave people ‘X’ worse off. The same as when my DB pension closed. It left me hundreds of thousands worse off in theory and I adjusted my plans.

Who knows what the future brings? The exact reason I work in today’s money and the increases I know, although FWIW I ignore the TL.Saving for the future, without suffering today is basic common sense. e.g. in my 50’s I live on less than I know I could retire on today but choose not to.

As for the Triple Lock in isolation. It will take some political shift and compromise elsewhere. They can’t even make the winter fuel allowance removal stick and Tory 2.0 won’t want to rock the boat, unless there is something like a big hike in the basic rate of tax threshold. Who knows? In the future the state pension could be means tested, like the WFA.

Clearly the younger you are, the more change you are going to be faced with.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards