We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Pension advice

Beagle77

Posts: 7 Forumite

Hi im 48 and have a pension with standard life, it's worth about 71k at the moment.

Ive just been looking and it's invested in a "Sustainable Multi Asset Annuity SLP (a lifestyle profile)".

I can change this to 12 funds that I pick myself but I don't know which to pick and im not just going to pick at random, im going to do my research first, which is why im here before I do anything.

Does anyone have any advice?

Ive just been looking and it's invested in a "Sustainable Multi Asset Annuity SLP (a lifestyle profile)".

I can change this to 12 funds that I pick myself but I don't know which to pick and im not just going to pick at random, im going to do my research first, which is why im here before I do anything.

Does anyone have any advice?

0

Comments

-

Does anyone have any advice?No advice here. Just discussion and opinion.

Does the current fund fit your objective? i.e. are you intending to buy an annuity at retirement?

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

Good for you! Have a look at https://rebeldonegans.com/finance/rfs/Beagle77 said:Hi im 48 and have a pension with standard life, it's worth about 71k at the moment.

Ive just been looking and it's invested in a "Sustainable Multi Asset Annuity SLP (a lifestyle profile)".

I can change this to 12 funds that I pick myself but I don't know which to pick and im not just going to pick at random, im going to do my research first, which is why im here before I do anything.

Does anyone have any advice?

Last year the Donegans were awarded the British Empire Medal for services to financial education through their Rebel Finance School - and yes, it really is free.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!3 -

As above it is only suitable if you intend to buy an annuity with the pot when you retire.

In simple terms, an annuity is where you exchange the pot for a guaranteed annual income for as long as you live.

The alternative is to leave the pot invested and draw down amounts from it each year.

Each have their plusses and minuses.

If you will want an annuity then the fund is basically OK, if you think you will drawdown the pot then it is the wrong fund to be in.2 -

Fair enough. I really just wondered if the funds that it's invested into now are the best ones to maximise my returns .

I wondered if I changed the funds to slightly more riskier ones it would grow faster?

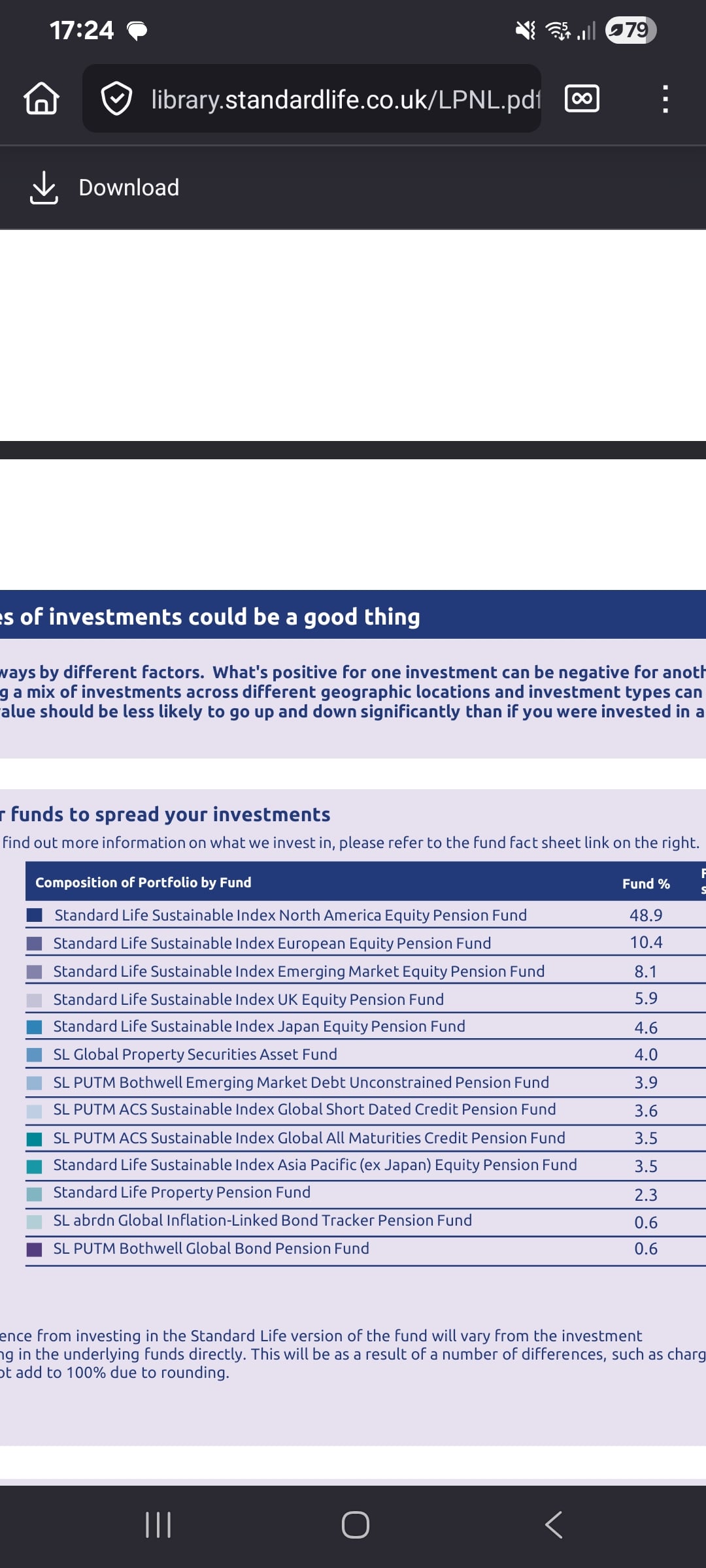

I feel like standard life would just put my funds into a safe investment, which in turn may not be the most lucrative. I've added the funds it's invested in now.

I've added the funds it's invested in now.

0 -

Pensions advice is a regulated industry, we cannot advise on MSE.1

-

Yeah i could have worded it better. It wasn't investment advice I wanted i want to make them.decisions myself, it was advice in where to look to research it all as best I can.

I just don't think it's invested in the best funds at the moment.0 -

Start on this forum. There are loads of interesting threads which you'll learn lots from. I did, and I'm now in a much stronger position. Not necessarily because of financial gain (although that has been the case) but because I now understand and am in control of my pensions.1

-

I would suggesting that you start to understand your objectives. The first two might be -

1. Understand how much you might need per year in retirement. I used a spreadsheet to track every penny I spent for three years before retiring (and still do 7 years on).

2. When might you hope to retire

3. Where is all your retirement money coming from (Savings, pensions, State Pension etc.)?

4. The work out whether what you have in point 4 will cover what you need from 1 from the date you have in mind from point 2 to say 90 years old (to start with).

Then you can work out what you need to do to start making the sums work. One part of this might be to inform what investments you might need. Say you can retire in 20 years, then all equities might be something to look with. If ten years, the maybe something less risky might be appropriate. But who knows until you understand a bit more avout your circumstances and objectives.2 -

I wondered if I changed the funds to slightly more riskier ones it would grow faster?Taking increased risk will improve returns in positive periods but increase losses in negative periods. The further you go up the risk scale, the more rollercoaster it would become.

For example, if you went 100% equities, it would be great when the stock markets grow, but could you handle a 40%-50% loss in a major downturn, or even an 80% loss in a once-in-a-century event?I feel like standard life would just put my funds into a safe investment, which in turn may not be the most lucrative.Lifestyle funds start with higher risk but reduce as you get closer to retirement. They use assets in the final years that hedge against annuity rates. It is fine if you are buying an annuity.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.3 -

So you're about 15 years from retirement? For me that would suggest making regular (monthly) investments in higher risk/volatility/return funds, of a globally diverse nature, for the next 5 to 10 years. After that you would probably want to think about moving to more steady funds since you are getting closer to withdrawing the money.

But that doesn't mean I would move an existing 71k fund into a high risk investment, especially at the moment when global stocks are near all-time highs.

As has been pointed out, the old-fashioned lifestyle approach you are currently enrolled in was better suited to those who would convert their entire fund into an annuity on retirement. This is itself somewhat old-fashioned even though annuities are still a valuable way of using defined contribution pots.A little FIRE lights the cigar1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards