We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Interest reported to HMRC in wrong year

Comments

-

Just be aware that not everybody is allowed to do self assessment, just because they want to.Annemos said:I had not seen your Posting when I posted mine, MinstrelWelly.

(I have posted about the differing tax rate between 26/27 and 27/28, which is now affecting these Bonds, too.)

You are making me think I should also do a self-assessment, as this type of issue also stresses me out.

(Once before, HMRC had tried to change my notice of coding wrongly and the phone calls got into such a tangle, the only way it was resolved was through a Complaint.)

https://forums.moneysavingexpert.com/discussion/6646703/fixed-rate-non-isa-bonds-straddling-2-tax-years-new-22-per-cent-tax-rate-on-interest#latest

I used to do it but was blocked a few years ago. I think it was part of a drive to reduce the number of SA's and I still can not do one, even if I wanted to.

However it seems this drive to reduce them seems to have petered out, so hopefully you will be OK.1 -

Albermarle said:

Just be aware that not everybody is allowed to do self assessment, just because they want to.Annemos said:I had not seen your Posting when I posted mine, MinstrelWelly.

(I have posted about the differing tax rate between 26/27 and 27/28, which is now affecting these Bonds, too.)

You are making me think I should also do a self-assessment, as this type of issue also stresses me out.

(Once before, HMRC had tried to change my notice of coding wrongly and the phone calls got into such a tangle, the only way it was resolved was through a Complaint.)

https://forums.moneysavingexpert.com/discussion/6646703/fixed-rate-non-isa-bonds-straddling-2-tax-years-new-22-per-cent-tax-rate-on-interest#latest

I used to do it but was blocked a few years ago. I think it was part of a drive to reduce the number of SA's and I still can not do one, even if I wanted to.

However it seems this drive to reduce them seems to have petered out, so hopefully you will be OK.The Finance Act 2019 gives everyone the legal right to do self assessment.https://www.legislation.gov.uk/ukpga/2019/1/part/4/crossheading/voluntary-returns

7 -

MinstrelWelly said:MinstrelWelly said:I've just found that Paragon and JN Bank have both reported interest to HMRC in 24/25 that isn't taxable until 26/27 (because its been added to a fixed term savings account). Consequently, that interest will be taxed in 24/25, which is going to cost me about £600 in incorrect tax. Not sure if all banks are the same, or its a problem with just some banks.I've spoken to HMRC, who obviously could talk to the banks, and ask them to report the figures correctly, and solve the problem for all those affected, but they're not interested, and tell me I've got to contact the bank to get my figures corrected.I've spoken to Paragon, who just say that their process is to report interest in the year its credited, not the year in which tax is due.I'm still awaiting a response from JN Bank.This leaves me with several questions1) Is the correct process for the banks to report interest in the year that its due, rather than the year its credited (or are they supposed to report in the year credited, but tell HMRC which year its taxable in)?2) Do any of the banks get this right? I.e. are all banks getting it wrong, or have I just got unlucky with my choice of banks?3) How can I proceed from here? Neither HMRC, nor the banks, perceive a probem, or at least, its not there problem. How can I get my tax corrected? At the moment, my only thought, is to raise a formal complaint with each of HMRC/Paragon/JN. HMRC for not ensuring that the banks are reporting correctly, and the banks for not reporting correctly (but it would help to be absolutely clear what the banks are supposed to be reporting)

Many thanks for all the replies. I've decided to go down the self-assessment route, and hope that HMRC don't query my interest figures (while keeping evidence to justify them). Self assessment done within a couple of hours, and it was _so_ much less stressful than doing simple assessment, and repeatedly waiting for HMRC to get it wrong, and then trying to get them to put it right.

Welcome to the club!

Hopefully your first experience with self assessment will hopefully encourage others to consider this option as a means of taking some proactive control of their tax affairs.1 -

If I go into my personal tax account online, there is still a SA section, as historically I have done SA returns until about 5 years ago.masonic said:Albermarle said:

Just be aware that not everybody is allowed to do self assessment, just because they want to.Annemos said:I had not seen your Posting when I posted mine, MinstrelWelly.

(I have posted about the differing tax rate between 26/27 and 27/28, which is now affecting these Bonds, too.)

You are making me think I should also do a self-assessment, as this type of issue also stresses me out.

(Once before, HMRC had tried to change my notice of coding wrongly and the phone calls got into such a tangle, the only way it was resolved was through a Complaint.)

https://forums.moneysavingexpert.com/discussion/6646703/fixed-rate-non-isa-bonds-straddling-2-tax-years-new-22-per-cent-tax-rate-on-interest#latest

I used to do it but was blocked a few years ago. I think it was part of a drive to reduce the number of SA's and I still can not do one, even if I wanted to.

However it seems this drive to reduce them seems to have petered out, so hopefully you will be OK.The Finance Act 2019 gives everyone the legal right to do self assessment.https://www.legislation.gov.uk/ukpga/2019/1/part/4/crossheading/voluntary-returns

If I try to start a new one, it does not work. ( I can not remember the exact message)

So I presume if I wanted to exercise my legal right to do a SA return, I would have to call HMRC to unblock me.

I suspect it would not be a quick or simple process, considering the mess caused when they involuntarily switched me from SA - at one point I was not allowed to do SA but was not getting any simple assessments either.

So I will let sleeping dogs lie, especially as my P800 was correct and my affairs are quite simple.

0 -

Albermarle said:

If I go into my personal tax account online, there is still a SA section, as historically I have done SA returns until about 5 years ago.masonic said:Albermarle said:

Just be aware that not everybody is allowed to do self assessment, just because they want to.Annemos said:I had not seen your Posting when I posted mine, MinstrelWelly.

(I have posted about the differing tax rate between 26/27 and 27/28, which is now affecting these Bonds, too.)

You are making me think I should also do a self-assessment, as this type of issue also stresses me out.

(Once before, HMRC had tried to change my notice of coding wrongly and the phone calls got into such a tangle, the only way it was resolved was through a Complaint.)

https://forums.moneysavingexpert.com/discussion/6646703/fixed-rate-non-isa-bonds-straddling-2-tax-years-new-22-per-cent-tax-rate-on-interest#latest

I used to do it but was blocked a few years ago. I think it was part of a drive to reduce the number of SA's and I still can not do one, even if I wanted to.

However it seems this drive to reduce them seems to have petered out, so hopefully you will be OK.The Finance Act 2019 gives everyone the legal right to do self assessment.https://www.legislation.gov.uk/ukpga/2019/1/part/4/crossheading/voluntary-returns

If I try to start a new one, it does not work. ( I can not remember the exact message)

So I presume if I wanted to exercise my legal right to do a SA return, I would have to call HMRC to unblock me.

I suspect it would not be a quick or simple process, considering the mess caused when they involuntarily switched me from SA - at one point I was not allowed to do SA but was not getting any simple assessments either.

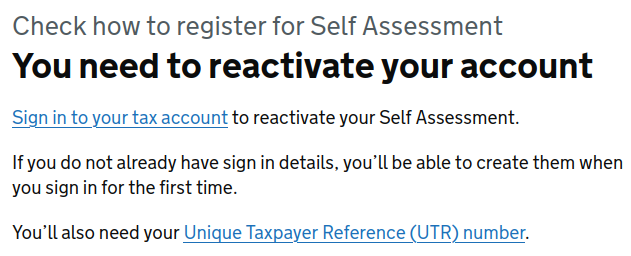

So I will let sleeping dogs lie, especially as my P800 was correct and my affairs are quite simple.It does say you need to register again if you did not file in the previous year, see https://www.gov.uk/log-in-file-self-assessment-tax-returnThis is what I get when I go to register again, say I'm doing it for "another reason" and that I did not complete a return last year but have registered before: It suggests to me it can be done without manual intervention, but I can't go any further as my account is already active.The quickest way in the first instance (especially those who have never registered) is probably to download and complete the paper form at https://www.gov.uk/guidance/how-to-complete-your-self-assessment-tax-return-for-last-tax-yearFor those with simple affairs, only a few boxes need to be filled out.Once the first paper form is received, I rather suspect HMRC will want to make their own life easier and let the customer file online thereafter, and there is plenty of time to do this for the 2026/27 tax year.2

It suggests to me it can be done without manual intervention, but I can't go any further as my account is already active.The quickest way in the first instance (especially those who have never registered) is probably to download and complete the paper form at https://www.gov.uk/guidance/how-to-complete-your-self-assessment-tax-return-for-last-tax-yearFor those with simple affairs, only a few boxes need to be filled out.Once the first paper form is received, I rather suspect HMRC will want to make their own life easier and let the customer file online thereafter, and there is plenty of time to do this for the 2026/27 tax year.2 -

masonic said:Albermarle said:

If I go into my personal tax account online, there is still a SA section, as historically I have done SA returns until about 5 years ago.masonic said:Albermarle said:

Just be aware that not everybody is allowed to do self assessment, just because they want to.Annemos said:I had not seen your Posting when I posted mine, MinstrelWelly.

(I have posted about the differing tax rate between 26/27 and 27/28, which is now affecting these Bonds, too.)

You are making me think I should also do a self-assessment, as this type of issue also stresses me out.

(Once before, HMRC had tried to change my notice of coding wrongly and the phone calls got into such a tangle, the only way it was resolved was through a Complaint.)

https://forums.moneysavingexpert.com/discussion/6646703/fixed-rate-non-isa-bonds-straddling-2-tax-years-new-22-per-cent-tax-rate-on-interest#latest

I used to do it but was blocked a few years ago. I think it was part of a drive to reduce the number of SA's and I still can not do one, even if I wanted to.

However it seems this drive to reduce them seems to have petered out, so hopefully you will be OK.The Finance Act 2019 gives everyone the legal right to do self assessment.https://www.legislation.gov.uk/ukpga/2019/1/part/4/crossheading/voluntary-returns

If I try to start a new one, it does not work. ( I can not remember the exact message)

So I presume if I wanted to exercise my legal right to do a SA return, I would have to call HMRC to unblock me.

I suspect it would not be a quick or simple process, considering the mess caused when they involuntarily switched me from SA - at one point I was not allowed to do SA but was not getting any simple assessments either.

So I will let sleeping dogs lie, especially as my P800 was correct and my affairs are quite simple.It does say you need to register again if you did not file in the previous year, see https://www.gov.uk/log-in-file-self-assessment-tax-returnThis is what I get when I go to register again, say I'm doing it for "another reason" and that I did not complete a return last year but have registered before:It suggests to me it can be done without manual intervention, but I can't go any further as my account is already active.The quickest way in the first instance (especially those who have never registered) is probably to download and complete the paper form at https://www.gov.uk/guidance/how-to-complete-your-self-assessment-tax-return-for-last-tax-yearFor those with simple affairs, only a few boxes need to be filled out.Once the first paper form is received, I rather suspect HMRC will want to make their own life easier and let the customer file online thereafter, and there is plenty of time to do this for the 2026/27 tax year.

I managed to activate Self Assessment by starting in the HMRC app, and going into the Self Assessment section, and following the process there. I have done paper Self Assessment before, but it was many years (20?) ago. I imagine someone would similarly be able to activate (online) Self Assessment for the first time in the same way.2 -

Good to know. It sounds like online may be the way to go for anyone in that case. I think the online process is probably a bit easier too, as it guides you through the relevant sections, skipping over the bits that don't apply.MinstrelWelly said:I managed to activate Self Assessment by starting in the HMRC app, and going into the Self Assessment section, and following the process there. I have done paper Self Assessment before, but it was many years (20?) ago. I imagine someone would similarly be able to activate (online) Self Assessment for the first time in the same way.1 -

As explained, if the account can be accessed, it is taxable in the year it is received.MinstrelWelly said:Thanks for your responses.By 'due' I meant when the tax is due. Interest is paid each year, but that interest is taxable at the end of term (so all interest is taxable in the tax year of end-of-term)With regard to the Gov.uk manual, and 'Example 2'. Yes, I've checked that out. I don't have access to the money until end-of-term, even with a penalty. Tax is definitely due on all the interest at end of term.I've been reading the Gov.uk instructions to banks on reporting interest earned via the "Bank And Building Society Interest Returns". I'm a newby so can't post links, but if you google the quoted return name, it'll be the first option.The instructions just say that banks must annually report interest paid. There is no mention of reporting interest in the year when tax on it is due. The spreadsheet only has one column for tax year (so you can't separately identify the year interest was credited and year interest is taxable), and the instructions say you only need to fill the year column in for one row, so the implication is that all entries will be for the same tax year.So, my take is that the banks are following the instructions, in reporting the interest credited each year (in the tax year that its credited). Meanwhile, HMRC are treating it as taxable in the year reported (which is the year in which the interest is credited, but not the year its taxable!)Or put it another way. HMRC are assuming that banks will report interest in the year that it is taxable, even though they haven't told the banks to do that via their instructions.

The bank and HMRC have likely applied the correct treatment."Real knowledge is to know the extent of one's ignorance" - Confucius0 -

kinger101 said:

As explained, if the account can be accessed, it is taxable in the year it is received.MinstrelWelly said:Thanks for your responses.By 'due' I meant when the tax is due. Interest is paid each year, but that interest is taxable at the end of term (so all interest is taxable in the tax year of end-of-term)With regard to the Gov.uk manual, and 'Example 2'. Yes, I've checked that out. I don't have access to the money until end-of-term, even with a penalty. Tax is definitely due on all the interest at end of term.I've been reading the Gov.uk instructions to banks on reporting interest earned via the "Bank And Building Society Interest Returns". I'm a newby so can't post links, but if you google the quoted return name, it'll be the first option.The instructions just say that banks must annually report interest paid. There is no mention of reporting interest in the year when tax on it is due. The spreadsheet only has one column for tax year (so you can't separately identify the year interest was credited and year interest is taxable), and the instructions say you only need to fill the year column in for one row, so the implication is that all entries will be for the same tax year.So, my take is that the banks are following the instructions, in reporting the interest credited each year (in the tax year that its credited). Meanwhile, HMRC are treating it as taxable in the year reported (which is the year in which the interest is credited, but not the year its taxable!)Or put it another way. HMRC are assuming that banks will report interest in the year that it is taxable, even though they haven't told the banks to do that via their instructions.

The bank and HMRC have likely applied the correct treatment.

No, they haven't. The banks report interest in the year its credited, because that's what they've been tasked with doing. That report doesn't indicate when the interest is taxable, so for simple assessment, HMRC assume its taxable in the year reported.2 -

The bank have applied the correct treatment, since as the OPs later post clarified, BBSI gives them one column to fill out (how much interest has the saver earned) and requires them to do it in the year it is credited. Put it another way, HMRC are asking the wrong question to elicit a response that tells them the whole story. If they asked how much accessible interest has a saver earned, then the bank would be allowed to report a fixed bond on maturity only and save everyone the aggro - and the bank would then be the problem if they erroneously reported interest that was not accessible, meaning less work for HMRC. NS&I admitted that fixes having any form of early access was unusual when they changed their terms back in 2019.kinger101 said:

As explained, if the account can be accessed, it is taxable in the year it is received.MinstrelWelly said:Thanks for your responses.By 'due' I meant when the tax is due. Interest is paid each year, but that interest is taxable at the end of term (so all interest is taxable in the tax year of end-of-term)With regard to the Gov.uk manual, and 'Example 2'. Yes, I've checked that out. I don't have access to the money until end-of-term, even with a penalty. Tax is definitely due on all the interest at end of term.I've been reading the Gov.uk instructions to banks on reporting interest earned via the "Bank And Building Society Interest Returns". I'm a newby so can't post links, but if you google the quoted return name, it'll be the first option.The instructions just say that banks must annually report interest paid. There is no mention of reporting interest in the year when tax on it is due. The spreadsheet only has one column for tax year (so you can't separately identify the year interest was credited and year interest is taxable), and the instructions say you only need to fill the year column in for one row, so the implication is that all entries will be for the same tax year.So, my take is that the banks are following the instructions, in reporting the interest credited each year (in the tax year that its credited). Meanwhile, HMRC are treating it as taxable in the year reported (which is the year in which the interest is credited, but not the year its taxable!)Or put it another way. HMRC are assuming that banks will report interest in the year that it is taxable, even though they haven't told the banks to do that via their instructions.

The bank and HMRC have likely applied the correct treatment.

By definition HMRC will apply incorrect treatment every time a saver has a multi year product that doesn’t either a) pay interest away to a nominated account or b) work in the same way as NS&I and apply all interest at the end of the term and nothing in between. Those are in the minority I believe, but HMRC assume that one of those applies without giving banks and building socieities the means to say that it does not.

Nationwide getting into the habit of releasing competitive 18 month fixed bonds in May has me thinking that they must be aware of the issue. Their timing means it is all in one year and the issue doesn’t arise; I suspect most incorrectly taxed savers who realise there is a problem first complain to the bank because they are easier to get hold of than HMRC.4

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards