We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

We're aware that some users are currently experiencing errors on the Forum. Our tech team is working to resolve the issue. Thanks for your patience.

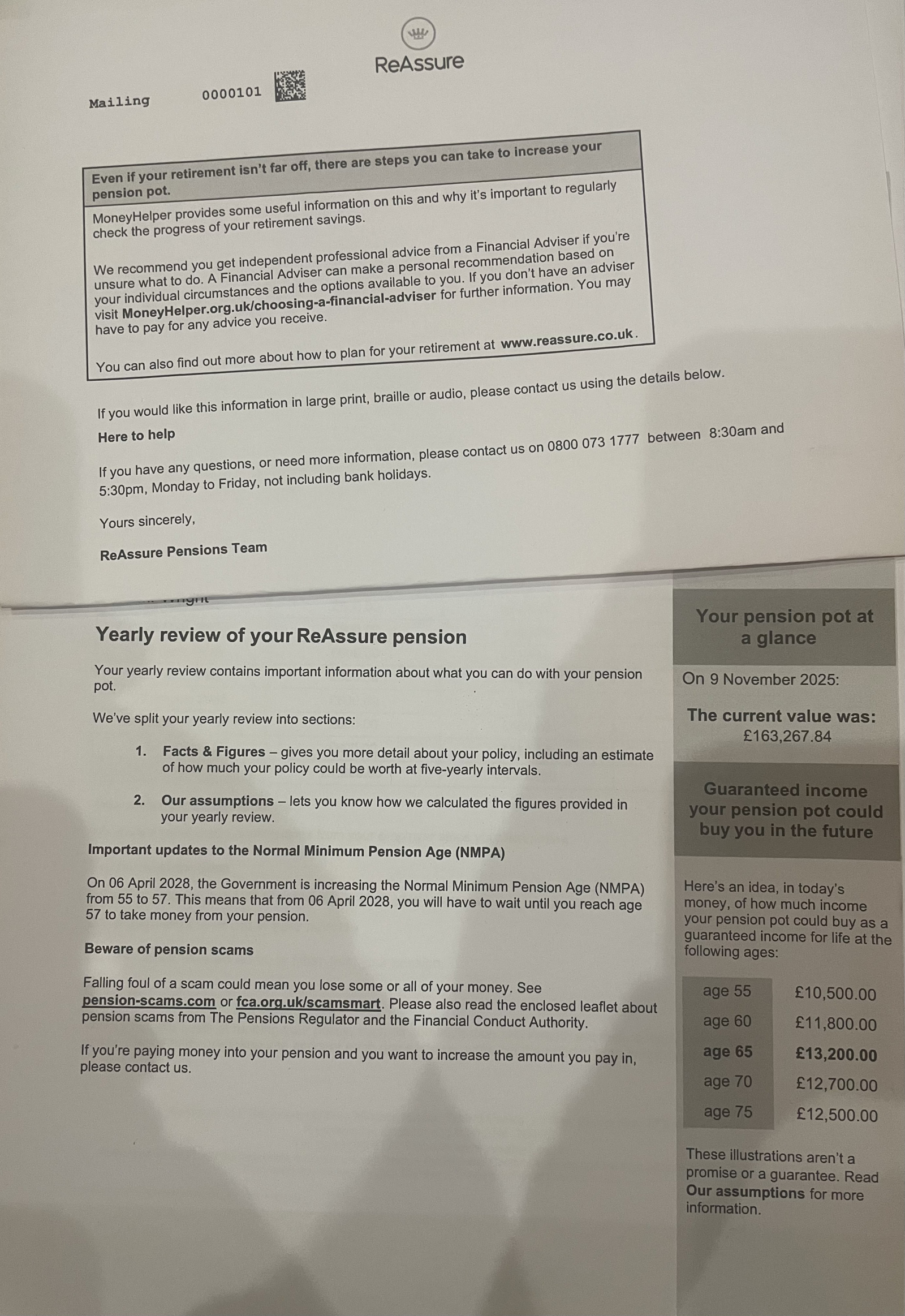

Age to take my personal pension

lionel_hutz

Posts: 55 Forumite

I recently received my pension statement and am after some advice.

I’m 51 years old and in addition to my stakeholder personal pension, which is the one I have this question about, I also have a workplace pension and I’d say I have a good understanding of general finances.

I have a retirement date set of 2039 when I’ll be 65.

I pay in about 9,000 per year.

My predicted pension is

11,800 at 60 years old

13,200 at 65 years old

12,700 at 70 years old

12,500 at 75 years old.

Why would my yearly pension be worth less at 70 than 65? Surely the fund will continue growing if I retired later than 65 and took my pension then?

Would I be better to start taking the pension at 60 years old, as if I waited until 65 I’d have paid in another 45,000 for the benefit of only receiving 1,400 extra per year?

I’m 51 years old and in addition to my stakeholder personal pension, which is the one I have this question about, I also have a workplace pension and I’d say I have a good understanding of general finances.

I have a retirement date set of 2039 when I’ll be 65.

I pay in about 9,000 per year.

My predicted pension is

11,800 at 60 years old

13,200 at 65 years old

12,700 at 70 years old

12,500 at 75 years old.

Why would my yearly pension be worth less at 70 than 65? Surely the fund will continue growing if I retired later than 65 and took my pension then?

Would I be better to start taking the pension at 60 years old, as if I waited until 65 I’d have paid in another 45,000 for the benefit of only receiving 1,400 extra per year?

0

Comments

-

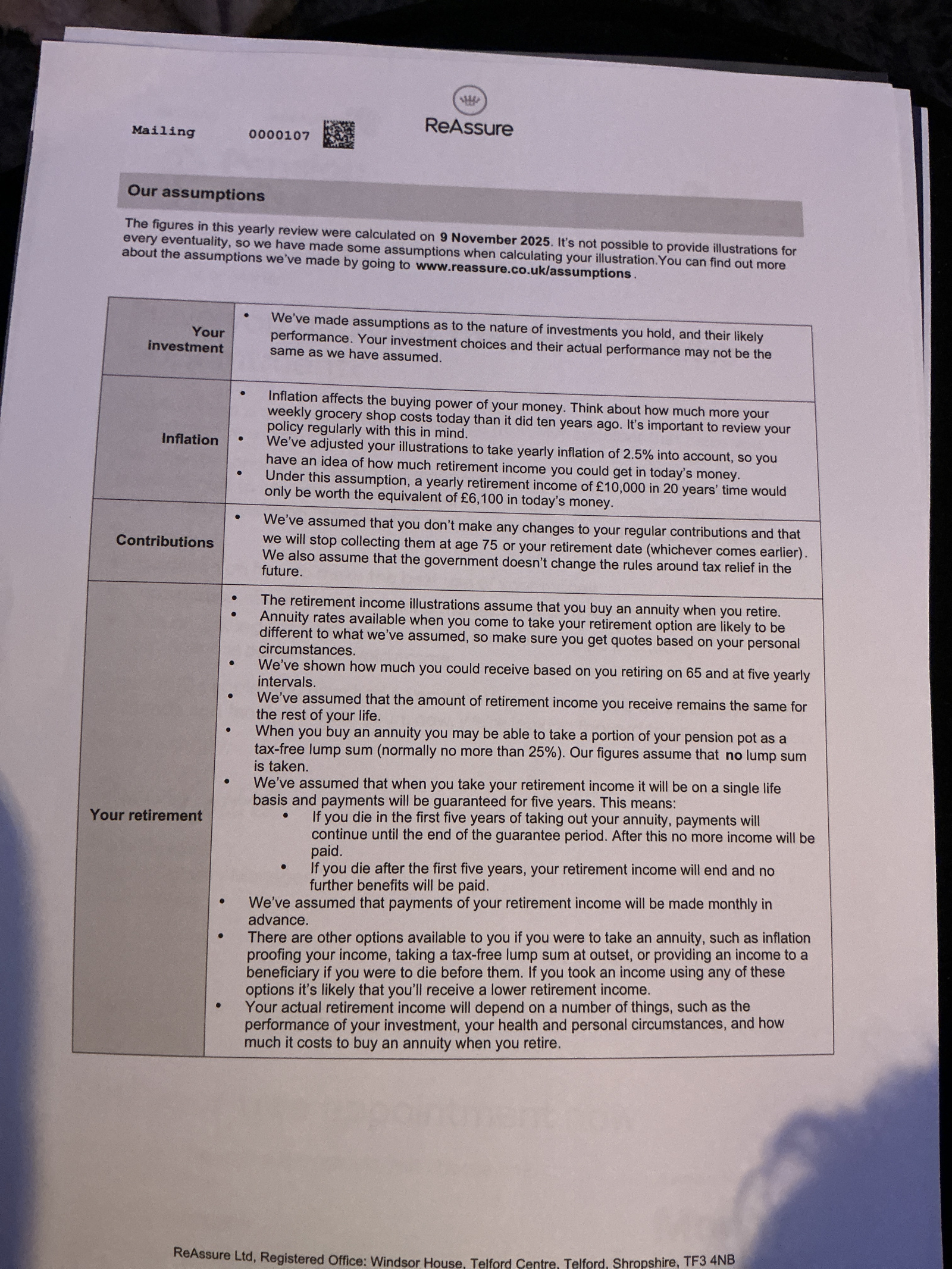

Is it possible the figures assume you start taking a pension at age 65?

I may be wrong but the "predicted pension" figures are probably based on a set of assumptions and they may explain why the figures drop away.

2 -

I agree with DRS1, the answer will lie in the set of assumptions that have been made.

However, you asked "Would I be better to start taking the pension at 60 years old, as if I waited until 65 I’d have paid in another 45,000 for the benefit of only receiving 1,400 extra per year?

This suggests that the assumptions assume that you will get less than 3% return on the investment (after charges). If correct, this seems to be rather poor value. You need to understand why this is. We can't really help as your provider has the details of the assumptions they have used.

What I can tell you is that I am retired and I get a return of about 6% (after fees) on my pension investments; I'm a DIY investor, so a professional should be able to acheive the same return with the same risk (after their fees). (I am perhaps more willing to take risks than most pensioners).

I use income drawdown to take an income from my pension, so everything that I don't draw out remains invested and continues to grow (actually my retirement portfolio is invested in income-producing funds, so what I don't draw out continues to receive dividends). If you buy an annuity, the insurance company invests the money and they keep any excess return above what is needed to pay the income (and rises in income) you have contracted with them for. If you die earlier than expected, they usually keep all the money. If you use income drawdown, you can leave any funds that remain unspent at the time of your death to a loved one or a charity.The comments I post are my personal opinion. While I try to check everything is correct before posting, I can and do make mistakes, so always try to check official information sources before relying on my posts.1 -

Almost certainly the projected figures are in 'real money',which means inflation is taken into account.lionel_hutz said:I recently received my pension statement and am after some advice.

I’m 51 years old and in addition to my stakeholder personal pension, which is the one I have this question about, I also have a workplace pension and I’d say I have a good understanding of general finances.

I have a retirement date set of 2039 when I’ll be 65.

I pay in about 9,000 per year.

My predicted pension is

11,800 at 60 years old

13,200 at 65 years old

12,700 at 70 years old

12,500 at 75 years old.

Why would my yearly pension be worth less at 70 than 65? Surely the fund will continue growing if I retired later than 65 and took my pension then?

Would I be better to start taking the pension at 60 years old, as if I waited until 65 I’d have paid in another 45,000 for the benefit of only receiving 1,400 extra per year?

In other words they are not saying you will actually get £12500 at 75 years old. Your actual pension will be significantly more than that, but after an estimate of inflation over many years is taken into account, it will buy you £12500 worth of goods at todays prices.

So to calculate these figures they use an estimate of investment growth, and an estimate of inflation, and an estimate of annuity rates. As a guess I would say the estimate for growth is slightly less than their estimate for inflation. Hence you estimated pension in real money declines each year from 65.

You will notice that I have used the word 'estimate' quite a lot and that is all these projections are.

I suspect that you also maybe invested too cautiously, hence maybe a low estimate for growth.

2 -

Perhaps the amounts are based on the expectations that you'll need to take more if you retire early whereas after age 67 they assume you will take state pension so don't need so much.

Can you post an anonymised photo of the projection including any small print?0 -

For the avoidance of any doubt is this a defined contribution pension scheme?

If this is a defined benefit pension scheme then the lower amount could be that the pension pays out a higher amount until you reach the state pension age and after that date it is no longer included within your pension (as is the case for me with one of my old DB pensions schemes).1 -

I also invest in a stocks and shares ISA and don’t mind a bit if risk. As you say probably a good idea to look at moving to a different pension fund or provider, possibly move more money to an investment fund also rather than a pension.tacpot12 said:I agree with DRS1, the answer will lie in the set of assumptions that have been made.

However, you asked "Would I be better to start taking the pension at 60 years old, as if I waited until 65 I’d have paid in another 45,000 for the benefit of only receiving 1,400 extra per year?

This suggests that the assumptions assume that you will get less than 3% return on the investment (after charges). If correct, this seems to be rather poor value. You need to understand why this is. We can't really help as your provider has the details of the assumptions they have used.

What I can tell you is that I am retired and I get a return of about 6% (after fees) on my pension investments; I'm a DIY investor, so a professional should be able to acheive the same return with the same risk (after their fees). (I am perhaps more willing to take risks than most pensioners).

I use income drawdown to take an income from my pension, so everything that I don't draw out remains invested and continues to grow (actually my retirement portfolio is invested in income-producing funds, so what I don't draw out continues to receive dividends). If you buy an annuity, the insurance company invests the money and they keep any excess return above what is needed to pay the income (and rises in income) you have contracted with them for. If you die earlier than expected, they usually keep all the money. If you use income drawdown, you can leave any funds that remain unspent at the time of your death to a loved one or a charity.0 -

leosayer said:Perhaps the amounts are based on the expectations that you'll need to take more if you retire early whereas after age 67 they assume you will take state pension so don't need so much.

Can you post an anonymised photo of the projection including any small print? I’d this any use?

I’d this any use?

0 -

You have left out the bit about "Our assumptions".0

-

DRS1 said:You have left out the bit about "Our assumptions".

I noticed when reading this it’s based on the value of my pension depreciating in REAL VALUE by 2.5% per year, I’m presuming that’s why there’s a prediction for a lower income at 70 and 75 as there won’t be any more payments made after my retirement age I’ve selected of 65.

I noticed when reading this it’s based on the value of my pension depreciating in REAL VALUE by 2.5% per year, I’m presuming that’s why there’s a prediction for a lower income at 70 and 75 as there won’t be any more payments made after my retirement age I’ve selected of 65.

0 -

They explain that its in todays value so the numbers arent actually what you will receive but how it will feel so they are predicting that were you to wait from 70 to 75 you would in absolute terms receive more but it would feel like less as presumably they are guesstimating that the inflation will be greater than the escalation of the pension in deferment at that point in time.lionel_hutz said:

I’d this any use?leosayer said:Perhaps the amounts are based on the expectations that you'll need to take more if you retire early whereas after age 67 they assume you will take state pension so don't need so much.

Can you post an anonymised photo of the projection including any small print?1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards