We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Gilts - pricing

Comments

-

tigerspill said:

Great explanation and confirms what I think I understood. I am going to try to go through the maths here in detail to ensure I fully understand in detail so may have more questions.SnowMan said:tigerspill said:Can I ask another question for clarification.

There are two parts to an ILG -

1. Assuming the ILG is purchased at a nominal clean price of 100 (actual equivalent dirty price on the purchase day) - That on maturity, the ILG retains its clean value of 100 and this is then indexed by the inflation amount (RPI then CPIH) after 2030 over the time held (essentially the dirty price on maturity).

2. The Coupons paid.

Is it the case, that if we totally ignore the coupon, the capital invested at a clean price of 100 will fully retain its real value regardless of coupon. So the coupon can be seen as real growth in this example. OR, does the final real capital value assume coupons paid - i.e. the actual capital value on maturity wont quite have retained its real value, but will be less because of the coupons paid.If we look at T32 (at 30th December) it is priced very close to par at a clean price of 99.90. From the diagram below (the scaled amounts on the right) you can see that the amount at maturity, excluding the coupons, made up of the fawn, light blue and white elements provides the return to cover the inflationary element and the coupons shown in green provide the real return on top of this. If we look at TG51 which is priced below par at a £61.35 clean price (at 30th December) the maturity amount (excluding coupons) provides the return to cover the inflationary element. But in this case it also provides most of the real return also. The coupons only provide a small element of the real return in this case, the bit shaded in green.

If we look at TG51 which is priced below par at a £61.35 clean price (at 30th December) the maturity amount (excluding coupons) provides the return to cover the inflationary element. But in this case it also provides most of the real return also. The coupons only provide a small element of the real return in this case, the bit shaded in green. Where the real return comes from depends on how the coupon payable compares with the real return implied by the pricing of the index linked gilt.With T32 the coupon is 1.25%pa and the real return is 1.27%pa. So quite similar percentages which means the coupons roughly speaking cover the whole of the real return.But with TG51 the coupon is 0.125%pa of the indexed nominal (or about 0.20% of the dirty price taking into account the below par pricing where 0.2 = 0.125/0.6135) and the real return is much higher at 2.12%pa and so only a small part of the real return comes from the coupons.

Where the real return comes from depends on how the coupon payable compares with the real return implied by the pricing of the index linked gilt.With T32 the coupon is 1.25%pa and the real return is 1.27%pa. So quite similar percentages which means the coupons roughly speaking cover the whole of the real return.But with TG51 the coupon is 0.125%pa of the indexed nominal (or about 0.20% of the dirty price taking into account the below par pricing where 0.2 = 0.125/0.6135) and the real return is much higher at 2.12%pa and so only a small part of the real return comes from the coupons.

I did actually buy T32 on 29/12 at 187.50482 GBP for 13844.99 units (it seems there is a factor of 100 here). The accrued interest was £34.98 - I am not really sure what this is or how it is calculated? Is it paying the seller the accrued coupon to date as I will be paid the full coupon when this comes up? Yes the accrued interest is exactly what you say i.e. paying the seller the accrued coupon to date as you will be paid the full coupon when this is paid on 22/5/2026, and not just the coupon accrued since purchase.It is calculated as 39/181 x 0.0125/2 x 1.87608 x 13844.99 = 34.98where39 is number of days from last coupon (22/11/2025) to the settlement date (which is 2 working days after the purchase date for Scottish Widows Share Dealing so 31/12/2025).181 is the number of days from the last coupon (22/11/2025) to the next coupon (22/5/2026)0.0125 is the annual coupon rate i.e 1.25%1.87608 is the indexation factor from issue to settlement date (allowing for the 3 month lag) so an 87.608% increase because of the inflationary increase since issue13,844.99 is the number of units purchased

Yes the accrued interest is exactly what you say i.e. paying the seller the accrued coupon to date as you will be paid the full coupon when this is paid on 22/5/2026, and not just the coupon accrued since purchase.It is calculated as 39/181 x 0.0125/2 x 1.87608 x 13844.99 = 34.98where39 is number of days from last coupon (22/11/2025) to the settlement date (which is 2 working days after the purchase date for Scottish Widows Share Dealing so 31/12/2025).181 is the number of days from the last coupon (22/11/2025) to the next coupon (22/5/2026)0.0125 is the annual coupon rate i.e 1.25%1.87608 is the indexation factor from issue to settlement date (allowing for the 3 month lag) so an 87.608% increase because of the inflationary increase since issue13,844.99 is the number of units purchased

I came, I saw, I melted2 -

tigerspill said:

Thank you. I am holding my ILGs in an ISA so no tax liability.phlebas192 said:

Yes, the accrued interest is paid to the seller. nb: if you are not holding the gilt in a tax-free wrapper then you deduct the accrued interest from the first coupon received to determine how much taxable interest you have received. eg if the coupon is £160 then £125.02 is taxable interest and £34.98 is return of capital (which is not taxed). Similarly, if you were to sell the gilt then you would receive some accrued interest which is taxable.tigerspill said:

Great explanation and confirms what I think I understood. I am going to try to go through the maths here in detail to ensure I fully understand in detail so may have more questions.SnowMan said:tigerspill said:Can I ask another question for clarification.

There are two parts to an ILG -

1. Assuming the ILG is purchased at a nominal clean price of 100 (actual equivalent dirty price on the purchase day) - That on maturity, the ILG retains its clean value of 100 and this is then indexed by the inflation amount (RPI then CPIH) after 2030 over the time held (essentially the dirty price on maturity).

2. The Coupons paid.

Is it the case, that if we totally ignore the coupon, the capital invested at a clean price of 100 will fully retain its real value regardless of coupon. So the coupon can be seen as real growth in this example. OR, does the final real capital value assume coupons paid - i.e. the actual capital value on maturity wont quite have retained its real value, but will be less because of the coupons paid.If we look at T32 (at 30th December) it is priced very close to par at a clean price of 99.90. From the diagram below (the scaled amounts on the right) you can see that the amount at maturity, excluding the coupons, made up of the fawn, light blue and white elements provides the return to cover the inflationary element and the coupons shown in green provide the real return on top of this.If we look at TG51 which is priced below par at a £61.35 clean price (at 30th December) the maturity amount (excluding coupons) provides the return to cover the inflationary element. But in this case it also provides most of the real return also. The coupons only provide a small element of the real return in this case, the bit shaded in green.Where the real return comes from depends on how the coupon payable compares with the real return implied by the pricing of the index linked gilt.With T32 the coupon is 1.25%pa and the real return is 1.27%pa. So quite similar percentages which means the coupons roughly speaking cover the whole of the real return.But with TG51 the coupon is 0.125%pa of the indexed nominal (or about 0.20% of the dirty price taking into account the below par pricing where 0.2 = 0.125/0.6135) and the real return is much higher at 2.12%pa and so only a small part of the real return comes from the coupons.

I did actually buy T32 on 29/12 at 187.50482 GBP for 13844.99 units (it seems there is a factor of 100 here). The accrued interest was £34.98 - I am not really sure what this is or how it is calculated? Is it paying the seller the accrued coupon to date as I will be paid the full coupon when this comes up?

Another question about the tables shown at for example https://giltsyield.com./bond/inflation/

Regarding the column "Real Yield" - is the real yield per year? And is therefore in effect compounded to maturity?

I assume that Net Yield takes the tax on coupons into account if not wrapped.Yes the real yield is per year and the return if held to maturity (and ignoring usually minor assumptions re the reinvestment of coupons) will indeed be the quoted annual real return compounded to maturity.The net real yield does take into account the tax on coupons if the index linked gilt is not not wrapped in an ISA or SIPP and the coupons are not covered by the £1,000/£500/£0 savings allowance.I came, I saw, I melted1 -

Can I ask a question about the clean and dirty price for ILGs - in particular, how they change day by day.

Should the clean and dirty prices change exactly in line with other. So if the dirty price increases exactly 1% in a period, then the clean price will increase by exactly 1% as well. Or can they change at different rates - if so, why?

0 -

The dirty price will increase very slightly more quickly from day to day (unless the reference RPI index happens to be falling when it's the other way round) because it's movement includes the change in indexation (3 month lagged RPI increase) from day to day, whereas the clean price does not include indexation. Over a day it's hard to spot numerically or visually (because it is indexation for a single day and that's trivial relative to the general daily price movement) but over a year it adds up to a years indexation, i.e. RPI increase.

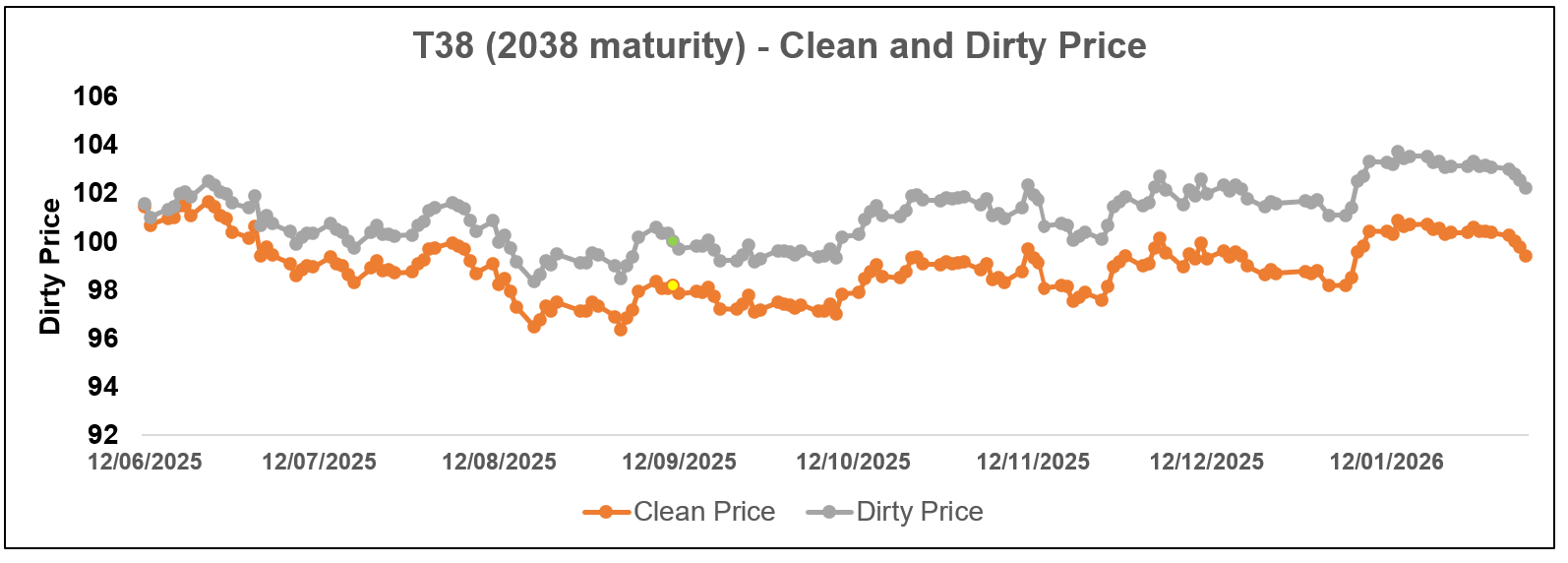

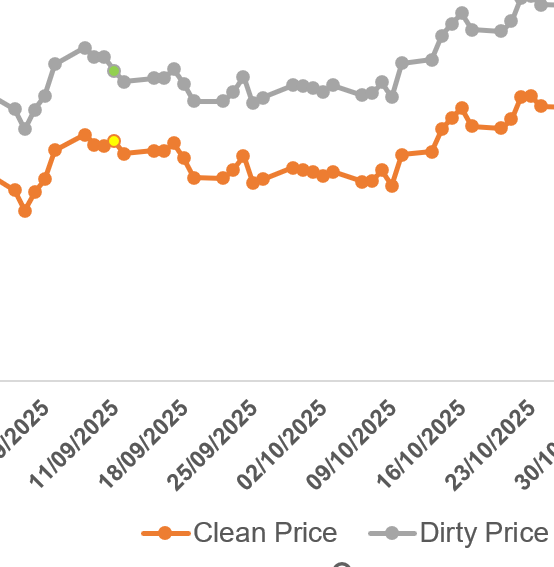

If we look at a chart of T38, which was issued on 11th June 2025 you can see how at issue the clean and dirty price are the same (because no indexation has at that point happened) but as time goes by the dirty price pulls away from the clean price because of the RPI indexation. Note I've truncated the y axis, rather than starting it at zero, so the price difference can be easily seen.

If we zoom in on the green and yellow dots in the above chart at 11th September we see that on 11th September 2025 the dirty price went down but the clean price went up. This is because T38 went xdividend on that date. The dirty price includes accrued interest. But the clean price excludes accrued interest. The accrued interest changed from 0.445716 on 10th September to minus 0.048454 on 11th September (per £100 unit) as it went xd. So the accrued interest is the other reason the price change can be different between clean and dirty prices, in particular on the day it goes xd.

I came, I saw, I melted5

I came, I saw, I melted5 -

Thank you. Makes sense now.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards