We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Gilts - pricing

Comments

-

The price of ILGs is driven by the value of equivalent duration fixed gilts. In 2021 expected long term inflation rates were perhaps around 2.5% when interest rates were less than 0.5%. Therefore ILGs were seen as a better buy than fixed gilts and prices adjusted themselves accordingly. Now interest rates are above 4% against long term inflation still much the same at around 2.5%. Hence low coupon ILGs are less desirable.tigerspill said:Can I ask a question about ILG pricing. Looking at these, it seems they were trading at a much highher prices not that long ago.

For example - TR41 was trading at over 140 and TRTQ over 150 (clean prices) in December 2021.

I can't understand why so many were buying these at that time and how they expected to get a return? I must be missing something.

1 -

tigerspill said:Can I ask a question about ILG pricing. Looking at these, it seems they were trading at a much highher prices not that long ago.

For example - TR41 was trading at over 140 and TRTQ over 150 (clean prices) in December 2021.

I can't understand why so many were buying these at that time and how they expected to get a return? I must be missing something.

We had a long period of artificially low interest rates, where the government could sell gilts at very low interest rates, with a long dated maturation. We then had a correction where interest rates reverted to more 'normal' levels and 'safe' gilts went through the biggest drop in value that anyone had ever seen.

Conventional thinking turned on its head, and the safe option in gilts lost a lot of money - but only for those who sold them. Those who kept them to maturity got the gains they had been offered.

Never say never, but it appears unlikely that we will go through such a drop any time soon, and gilts may go back to being the safe boring option.

In the meantime, for long-date gilts, you can still choose between conventional at a guaranteed 5%+, or index-linked at 2%+ above inflation. If you hold either of those to maturity you get the expected return, regardless of volatility in-between.

1 -

Yeah the crash particularly in the longer dated ILGs has been astonishing. A few years ago I never would have expected to make a material investment in something like my TR50 that's crashed 70% although I hardly think it will bounce back and pull so much future return forward again as we may never see zero interest rates reoccur in our lifetimes.tigerspill said:Can I ask a question about ILG pricing. Looking at these, it seems they were trading at a much highher prices not that long ago.

It's a bit like the offers in the January sales where a bed or carpet shop is knocking 50% off plus they are running a 10% promotional event and another 10% from the manager for today only which sounds great except there is no way I would ever have paid the full price. Still a 2.1% real return with no fund manager fees for the next 25 years is a bird in the hand and I've not bought many beds or carpets that have lasted that long.

A speculator could make a return if interest rates continued to drop or inflation picked up and they became more desirable. Some people will have already made gains in them getting up to those crazy valuations.tigerspill said:I can't understand why so many were buying these at that time and how they expected to get a return? I must be missing something.

Defined benefit pensions schemes or annuity providers might be required to buy them to underpin inflation linked guarantees they were offering pensioners effectively burning money to the negative yields by either having to further fund the DB scheme or offering a lower annuity income rate that some people still bought because they valued the lifetime income guarantee.

Tin hatters might have bought them because they expected high inflation and lower real returns from other assets.

Portfolio investors might have bough them because they were rigidly following multi asset diversification methods with no regard to valuations.

It was just the price enough people or organisations were willing to pay at the time.

The crash doesn't really matter to DB pension schemes or annuity providers as they intend to hold them to redemption anyway. For portfolio investors they have probably had upside in their equities exposure so the diversification will have protected them.1 -

Can I ask another question for clarification.

There are two parts to an ILG -

1. Assuming the ILG is purchased at a nominal clean price of 100 (actual equivalent dirty price on the purchase day) - That on maturity, the ILG retains its clean value of 100 and this is then indexed by the inflation amount (RPI then CPIH) after 2030 over the time held (essentially the dirty price on maturity).

2. The Coupons paid.

Is it the case, that if we totally ignore the coupon, the capital invested at a clean price of 100 will fully retain its real value regardless of coupon. So the coupon can be seen as real growth in this example. OR, does the final real capital value assume coupons paid - i.e. the actual capital value on maturity wont quite have retained its real value, but will be less because of the coupons paid.

1 -

(1) Yes and (2)Yes the coupon is additional to the inflation link.tigerspill said:Can I ask another question for clarification.

There are two parts to an ILG -

1. Assuming the ILG is purchased at a nominal clean price of 100 (actual equivalent dirty price on the purchase day) - That on maturity, the ILG retains its clean value of 100 and this is then indexed by the inflation amount (RPI then CPIH) after 2030 over the time held (essentially the dirty price on maturity).

2. The Coupons paid.

Is it the case, that if we totally ignore the coupon, the capital invested at a clean price of 100 will fully retain its real value regardless of coupon. So the coupon can be seen as real growth in this example. OR, does the final real capital value assume coupons paid - i.e. the actual capital value on maturity wont quite have retained its real value, but will be less because of the coupons paid.1 -

The capital returned is £100 multiplied by the final Index Ratio (covering all the compound inflation) - as ILGs are currently trading at a discount to the £100 x current Index Ratio then that's great because the inflation adjustment is actually an above-inflation increase to the dirty price you paid. Plus, assuming stable markets, you see the narrowing of the discount as you get closer to redemption.tigerspill said:Can I ask another question for clarification.

There are two parts to an ILG -

1. Assuming the ILG is purchased at a nominal clean price of 100 (actual equivalent dirty price on the purchase day) - That on maturity, the ILG retains its clean value of 100 and this is then indexed by the inflation amount (RPI then CPIH) after 2030 over the time held (essentially the dirty price on maturity).

2. The Coupons paid.

Is it the case, that if we totally ignore the coupon, the capital invested at a clean price of 100 will fully retain its real value regardless of coupon. So the coupon can be seen as real growth in this example. OR, does the final real capital value assume coupons paid - i.e. the actual capital value on maturity wont quite have retained its real value, but will be less because of the coupons paid.

The coupon is multiplied by the current Index Ratio so isn't as unattractive as it looks as again if you are buying at a discount to the £100 x current Index Ratio then it's a higher percentage of the dirty price you pay.

1 -

tigerspill said:Can I ask another question for clarification.

There are two parts to an ILG -

1. Assuming the ILG is purchased at a nominal clean price of 100 (actual equivalent dirty price on the purchase day) - That on maturity, the ILG retains its clean value of 100 and this is then indexed by the inflation amount (RPI then CPIH) after 2030 over the time held (essentially the dirty price on maturity).

2. The Coupons paid.

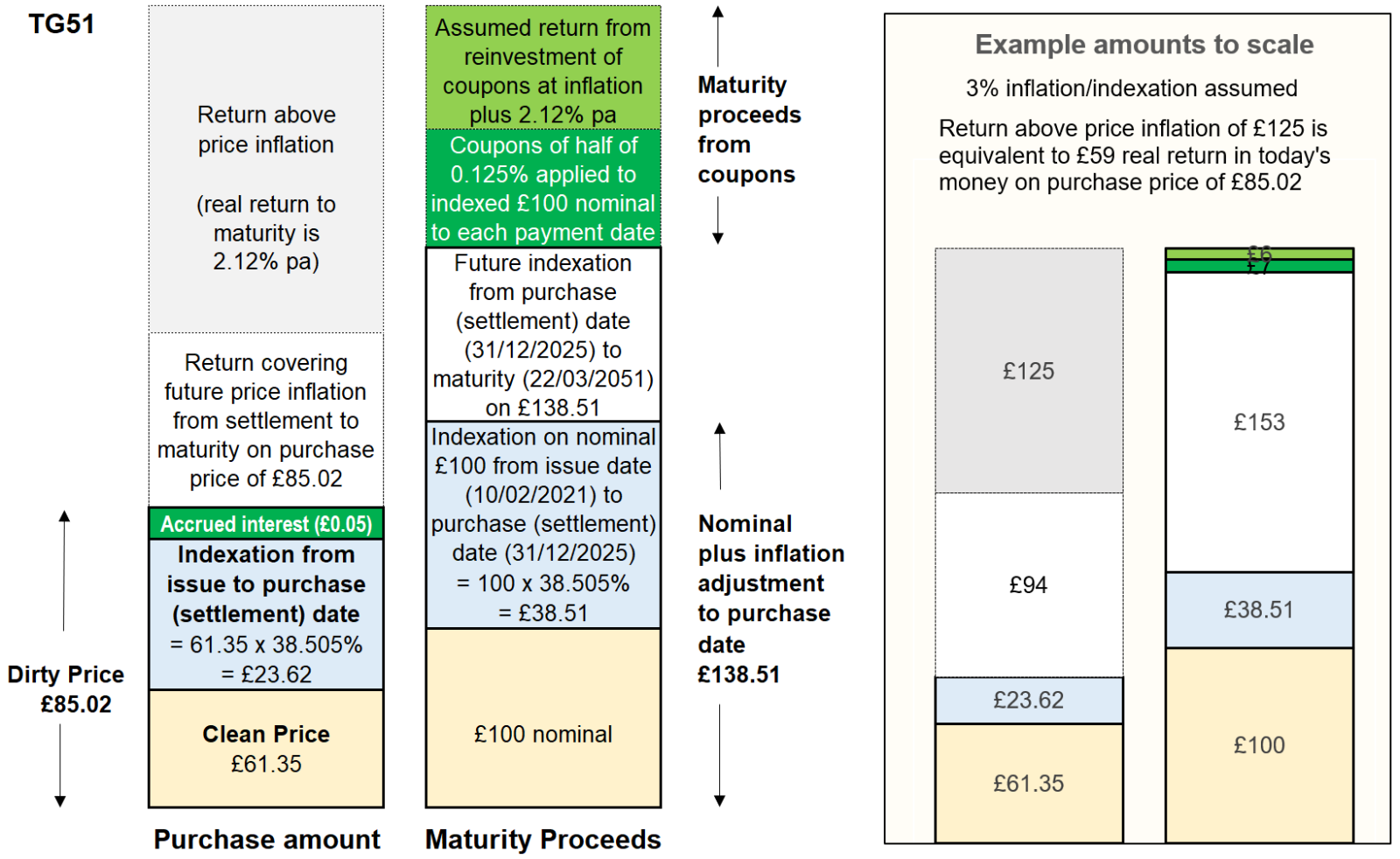

Is it the case, that if we totally ignore the coupon, the capital invested at a clean price of 100 will fully retain its real value regardless of coupon. So the coupon can be seen as real growth in this example. OR, does the final real capital value assume coupons paid - i.e. the actual capital value on maturity wont quite have retained its real value, but will be less because of the coupons paid.If we look at T32 (at 30th December) it is priced very close to par at a clean price of 99.90. From the diagram below (the scaled amounts on the right) you can see that the amount at maturity, excluding the coupons, made up of the fawn, light blue and white elements provides the return to cover the inflationary element and the coupons shown in green provide the real return on top of this. If we look at TG51 which is priced below par at a £61.35 clean price (at 30th December) the maturity amount (excluding coupons) provides the return to cover the inflationary element. But in this case it also provides most of the real return also. The coupons only provide a small element of the real return in this case, the bit shaded in green.

If we look at TG51 which is priced below par at a £61.35 clean price (at 30th December) the maturity amount (excluding coupons) provides the return to cover the inflationary element. But in this case it also provides most of the real return also. The coupons only provide a small element of the real return in this case, the bit shaded in green. Where the real return comes from depends on how the coupon payable compares with the real return implied by the pricing of the index linked gilt.With T32 the coupon is 1.25%pa and the real return is 1.27%pa. So quite similar percentages which means the coupons roughly speaking cover the whole of the real return.But with TG51 the coupon is 0.125%pa of the indexed nominal (or about 0.20% of the dirty price taking into account the below par pricing where 0.2 = 0.125/0.6135) and the real return is much higher at 2.12%pa and so only a small part of the real return comes from the coupons.I came, I saw, I melted8

Where the real return comes from depends on how the coupon payable compares with the real return implied by the pricing of the index linked gilt.With T32 the coupon is 1.25%pa and the real return is 1.27%pa. So quite similar percentages which means the coupons roughly speaking cover the whole of the real return.But with TG51 the coupon is 0.125%pa of the indexed nominal (or about 0.20% of the dirty price taking into account the below par pricing where 0.2 = 0.125/0.6135) and the real return is much higher at 2.12%pa and so only a small part of the real return comes from the coupons.I came, I saw, I melted8 -

Great explanation and confirms what I think I understood. I am going to try to go through the maths here in detail to ensure I fully understand in detail so may have more questions.SnowMan said:tigerspill said:Can I ask another question for clarification.

There are two parts to an ILG -

1. Assuming the ILG is purchased at a nominal clean price of 100 (actual equivalent dirty price on the purchase day) - That on maturity, the ILG retains its clean value of 100 and this is then indexed by the inflation amount (RPI then CPIH) after 2030 over the time held (essentially the dirty price on maturity).

2. The Coupons paid.

Is it the case, that if we totally ignore the coupon, the capital invested at a clean price of 100 will fully retain its real value regardless of coupon. So the coupon can be seen as real growth in this example. OR, does the final real capital value assume coupons paid - i.e. the actual capital value on maturity wont quite have retained its real value, but will be less because of the coupons paid.If we look at T32 (at 30th December) it is priced very close to par at a clean price of 99.90. From the diagram below (the scaled amounts on the right) you can see that the amount at maturity, excluding the coupons, made up of the fawn, light blue and white elements provides the return to cover the inflationary element and the coupons shown in green provide the real return on top of this.If we look at TG51 which is priced below par at a £61.35 clean price (at 30th December) the maturity amount (excluding coupons) provides the return to cover the inflationary element. But in this case it also provides most of the real return also. The coupons only provide a small element of the real return in this case, the bit shaded in green.Where the real return comes from depends on how the coupon payable compares with the real return implied by the pricing of the index linked gilt.With T32 the coupon is 1.25%pa and the real return is 1.27%pa. So quite similar percentages which means the coupons roughly speaking cover the whole of the real return.But with TG51 the coupon is 0.125%pa of the indexed nominal (or about 0.20% of the dirty price taking into account the below par pricing where 0.2 = 0.125/0.6135) and the real return is much higher at 2.12%pa and so only a small part of the real return comes from the coupons.

I did actually buy T32 on 29/12 at 187.50482 GBP for 13844.99 units (it seems there is a factor of 100 here). The accrued interest was £34.98 - I am not really sure what this is or how it is calculated? Is it paying the seller the accrued coupon to date as I will be paid the full coupon when this comes up? 1

1 -

Yes, the accrued interest is paid to the seller. nb: if you are not holding the gilt in a tax-free wrapper then you deduct the accrued interest from the first coupon received to determine how much taxable interest you have received. eg if the coupon is £160 then £125.02 is taxable interest and £34.98 is return of capital (which is not taxed). Similarly, if you were to sell the gilt then you would receive some accrued interest which is taxable.tigerspill said:

Great explanation and confirms what I think I understood. I am going to try to go through the maths here in detail to ensure I fully understand in detail so may have more questions.SnowMan said:tigerspill said:Can I ask another question for clarification.

There are two parts to an ILG -

1. Assuming the ILG is purchased at a nominal clean price of 100 (actual equivalent dirty price on the purchase day) - That on maturity, the ILG retains its clean value of 100 and this is then indexed by the inflation amount (RPI then CPIH) after 2030 over the time held (essentially the dirty price on maturity).

2. The Coupons paid.

Is it the case, that if we totally ignore the coupon, the capital invested at a clean price of 100 will fully retain its real value regardless of coupon. So the coupon can be seen as real growth in this example. OR, does the final real capital value assume coupons paid - i.e. the actual capital value on maturity wont quite have retained its real value, but will be less because of the coupons paid.If we look at T32 (at 30th December) it is priced very close to par at a clean price of 99.90. From the diagram below (the scaled amounts on the right) you can see that the amount at maturity, excluding the coupons, made up of the fawn, light blue and white elements provides the return to cover the inflationary element and the coupons shown in green provide the real return on top of this.If we look at TG51 which is priced below par at a £61.35 clean price (at 30th December) the maturity amount (excluding coupons) provides the return to cover the inflationary element. But in this case it also provides most of the real return also. The coupons only provide a small element of the real return in this case, the bit shaded in green.Where the real return comes from depends on how the coupon payable compares with the real return implied by the pricing of the index linked gilt.With T32 the coupon is 1.25%pa and the real return is 1.27%pa. So quite similar percentages which means the coupons roughly speaking cover the whole of the real return.But with TG51 the coupon is 0.125%pa of the indexed nominal (or about 0.20% of the dirty price taking into account the below par pricing where 0.2 = 0.125/0.6135) and the real return is much higher at 2.12%pa and so only a small part of the real return comes from the coupons.

I did actually buy T32 on 29/12 at 187.50482 GBP for 13844.99 units (it seems there is a factor of 100 here). The accrued interest was £34.98 - I am not really sure what this is or how it is calculated? Is it paying the seller the accrued coupon to date as I will be paid the full coupon when this comes up?1 -

Thank you. I am holding my ILGs in an ISA so no tax liability.phlebas192 said:

Yes, the accrued interest is paid to the seller. nb: if you are not holding the gilt in a tax-free wrapper then you deduct the accrued interest from the first coupon received to determine how much taxable interest you have received. eg if the coupon is £160 then £125.02 is taxable interest and £34.98 is return of capital (which is not taxed). Similarly, if you were to sell the gilt then you would receive some accrued interest which is taxable.tigerspill said:

Great explanation and confirms what I think I understood. I am going to try to go through the maths here in detail to ensure I fully understand in detail so may have more questions.SnowMan said:tigerspill said:Can I ask another question for clarification.

There are two parts to an ILG -

1. Assuming the ILG is purchased at a nominal clean price of 100 (actual equivalent dirty price on the purchase day) - That on maturity, the ILG retains its clean value of 100 and this is then indexed by the inflation amount (RPI then CPIH) after 2030 over the time held (essentially the dirty price on maturity).

2. The Coupons paid.

Is it the case, that if we totally ignore the coupon, the capital invested at a clean price of 100 will fully retain its real value regardless of coupon. So the coupon can be seen as real growth in this example. OR, does the final real capital value assume coupons paid - i.e. the actual capital value on maturity wont quite have retained its real value, but will be less because of the coupons paid.If we look at T32 (at 30th December) it is priced very close to par at a clean price of 99.90. From the diagram below (the scaled amounts on the right) you can see that the amount at maturity, excluding the coupons, made up of the fawn, light blue and white elements provides the return to cover the inflationary element and the coupons shown in green provide the real return on top of this.If we look at TG51 which is priced below par at a £61.35 clean price (at 30th December) the maturity amount (excluding coupons) provides the return to cover the inflationary element. But in this case it also provides most of the real return also. The coupons only provide a small element of the real return in this case, the bit shaded in green.Where the real return comes from depends on how the coupon payable compares with the real return implied by the pricing of the index linked gilt.With T32 the coupon is 1.25%pa and the real return is 1.27%pa. So quite similar percentages which means the coupons roughly speaking cover the whole of the real return.But with TG51 the coupon is 0.125%pa of the indexed nominal (or about 0.20% of the dirty price taking into account the below par pricing where 0.2 = 0.125/0.6135) and the real return is much higher at 2.12%pa and so only a small part of the real return comes from the coupons.

I did actually buy T32 on 29/12 at 187.50482 GBP for 13844.99 units (it seems there is a factor of 100 here). The accrued interest was £34.98 - I am not really sure what this is or how it is calculated? Is it paying the seller the accrued coupon to date as I will be paid the full coupon when this comes up?

Another question about the tables shown at for example https://giltsyield.com./bond/inflation/

Regarding the column "Real Yield" - is the real yield per year? And is therefore in effect compounded to maturity?

I assume that Net Yield takes the tax on coupons into account if not wrapped.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards