We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Capital gain tax for foreign currency on (non-tax-sheltered) brokerage account

megatower

Posts: 22 Forumite

Some of the brokerage account can hold foreign currencies directly but I wasn't sure how should the tax be treated if it's non-tax-sheltered. I want to hold some dollars to buy and sell securities, and I don't convert the dollar back to pounds in between different transactions, as I plan to continue to invest on dollar base securities. This will minimise the FX fee.

I understand the foreign currency on a bank account is not subject to capital gain tax (from exchange rate fluctuation), but would the same apply to the brokerage account, or even one step further, to Money Market Fund (especially those with constant NAV)?

If it is chargeable, should the gain be calculated according to a section 104 pool over all brokerage accounts (if there is more than one)?

Any thought or suggestion would be much appreciated.

0

Comments

-

You would disregard a cash balance in a foreign currency (although this may earn taxable interest), but if it is held in another financial instrument such as a MMF, then it would be treated as an investment and subject to CGT rules. There would only be a s104 pool if you held the same financial instrument across multiple accounts, you would not pool different USD MMF for example.This sort of thing has caught some people out because unbeknownst to them, their investment provider held their "uninvested cash" in QMMF, which means they made a matching disposal each time they placed a buy order. Degiro does this, for example. If the total value of disposals exceeds £50k then that brings them into CGT reporting, even though they had no taxable gain and didn't consider they made a disposal both when they sold a security and again when they reinvested, essentially doubling up the value of disposals in their account (e.g. Investment1 -> USD cash -> USD QMMF, then USD QMMF -> USD cash -> Investment2).1

-

De Giro fixed that particular issue.masonic said:You would disregard a cash balance in a foreign currency (although this may earn taxable interest), but if it is held in another financial instrument such as a MMF, then it would be treated as an investment and subject to CGT rules. There would only be a s104 pool if you held the same financial instrument across multiple accounts, you would not pool different USD MMF for example.This sort of thing has caught some people out because unbeknownst to them, their investment provider held their "uninvested cash" in QMMF, which means they made a matching disposal each time they placed a buy order, and the total value of disposals therefore exceeded £50k and brought them into CGT reporting, even though they had no taxable gain and didn't consider they made a disposal both when they sold a security and again when they reinvested. Degiro does this, for example.

"Since Brexit, we were required to use MMFs instead of cash accounts for our UK clients as our European banking license was no longer valid. Since April 2024, we are once again able to offer our new UK clients a cash account along with their investment account."1 -

That's great and exactly what I needed to know. It'd make the the life much easier. Hopefully my brokers (interactive brokers and Schwab) hasn't gone down the QMMF route.

Are you aware of any HMRC reference on discarding the foreign cash balance, or is it implicitly the same under the "bank accounts" rule?

One further thought is how should one maximize earning some interest on the "Uninvested cash" - maybe the safest option is probably just leave it on the brokerage account at a lightly lower interest rate? Investing in MMF or even Bond would have to be worthwhile to compensate the loss (or gain when it's lucky!) on CGT, which looks a bit tricky to manage.

Thanks again.0 -

megatower said:Are you aware of any HMRC reference on discarding the foreign cash balance, or is it implicitly the same under the "bank accounts" rule?As you say, you should establish that your broker holds your cash in a bank account rather than another type of currency-related asset.

It will add complexity and could equally likely create a tax liability as relieve one, so the extra return would have to be worth it.megatower said:

One further thought is how should one maximize earning some interest on the "Uninvested cash" - maybe the safest option is probably just leave it on the brokerage account at a lightly lower interest rate? Investing in MMF or even Bond would have to be worthwhile to compensate the loss (or gain when it's lucky!) on CGT, which looks a bit tricky to manage.

1 -

I've been in a similar situation to the OP in that I have converted some GBP to USD some time back to invest in US shares. Since then I have done some buying and selling of US shares, including reinvesting USd dividends and I have also converted some GBP to USD and vice versa within the interactve investor to buy US and UK shares respectively.The original (large) amount I converted a number of years back from GBP to USD was using Transferwise. I have not since used anyone to convert the USD back to GBP, the only conversions I have done has been within the ii platform as mentioned in the above para.All the above related to my GIA.When doing my CGT calculations for tax return, I have only ever included gains/losses on shares bought/sold and for any US shares I have converted the USD amount to GBP using FX rates at the time of the buys and sells.Have I missed anything with regards to CGT, particularly around FX conversions? I suspect not given the previous posts on this thread if I assume ii fx conversions I have done (back and forth gbp usd) is inside bank accounts(s) held by ii?What about the initial conversion from GBP to USD done via transferwise? the conversions in ii I have done might relate to some cash that was initially converted to USD in transferwise? But if both transferwise and ii conversions were all done by bank accounts in respective platforms, then I have not missed anything?If and when I convert USD to GBP via transferwise, I assume nothing to do for CGT?0

-

Given your use of the USD was in the course of running the account and FX gains and losses will have been incorporated in your CGT calculations when selling shares I'd say no. This is how I've always treated it and I think it fits with HMRC's guidance.itwasntme001 said:I've been in a similar situation to the OP in that I have converted some GBP to USD some time back to invest in US shares. Since then I have done some buying and selling of US shares, including reinvesting USd dividends and I have also converted some GBP to USD and vice versa within the interactve investor to buy US and UK shares respectively.The original (large) amount I converted a number of years back from GBP to USD was using Transferwise. I have not since used anyone to convert the USD back to GBP, the only conversions I have done has been within the ii platform as mentioned in the above para.All the above related to my GIA.When doing my CGT calculations for tax return, I have only ever included gains/losses on shares bought/sold and for any US shares I have converted the USD amount to GBP using FX rates at the time of the buys and sells.Have I missed anything with regards to CGT, particularly around FX conversions? I suspect not given the previous posts on this thread if I assume ii fx conversions I have done (back and forth gbp usd) is inside bank accounts(s) held by ii?What about the initial conversion from GBP to USD done via transferwise? the conversions in ii I have done might relate to some cash that was initially converted to USD in transferwise? But if both transferwise and ii conversions were all done by bank accounts in respective platforms, then I have not missed anything?If and when I convert USD to GBP via transferwise, I assume nothing to do for CGT?

The only time I've declared CGT gains on conversion is when I've specifically bought and sold sterling to speculate on movements between it and other currencies.1 -

wmb194 said:

Given your use of the USD was in the course of running the account and FX gains and losses will have been incorporated in your CGT calculations when selling shares I'd say no. This is how I've always treated it and I think it fits with HMRC's guidance.itwasntme001 said:I've been in a similar situation to the OP in that I have converted some GBP to USD some time back to invest in US shares. Since then I have done some buying and selling of US shares, including reinvesting USd dividends and I have also converted some GBP to USD and vice versa within the interactve investor to buy US and UK shares respectively.The original (large) amount I converted a number of years back from GBP to USD was using Transferwise. I have not since used anyone to convert the USD back to GBP, the only conversions I have done has been within the ii platform as mentioned in the above para.All the above related to my GIA.When doing my CGT calculations for tax return, I have only ever included gains/losses on shares bought/sold and for any US shares I have converted the USD amount to GBP using FX rates at the time of the buys and sells.Have I missed anything with regards to CGT, particularly around FX conversions? I suspect not given the previous posts on this thread if I assume ii fx conversions I have done (back and forth gbp usd) is inside bank accounts(s) held by ii?What about the initial conversion from GBP to USD done via transferwise? the conversions in ii I have done might relate to some cash that was initially converted to USD in transferwise? But if both transferwise and ii conversions were all done by bank accounts in respective platforms, then I have not missed anything?If and when I convert USD to GBP via transferwise, I assume nothing to do for CGT?

The only time I've declared CGT gains on conversion is when I've specifically bought and sold sterling to speculate on movements between it and other currencies.So are the rules around FX not being taxable on conversion due to the FX conversion transaction occuring in a bank account, or due to the FX conversion being in the course of running the account, or due to both?Just to confirm, in my situaiton (as outline din my previous post), the only gains/losses due to FX that need to be incorporated into any CGT calculation is when the shares are bought/sold? Not when its simply just a FX conversion (wherever that takes places)?0 -

itwasntme001 said:wmb194 said:

Given your use of the USD was in the course of running the account and FX gains and losses will have been incorporated in your CGT calculations when selling shares I'd say no. This is how I've always treated it and I think it fits with HMRC's guidance.itwasntme001 said:I've been in a similar situation to the OP in that I have converted some GBP to USD some time back to invest in US shares. Since then I have done some buying and selling of US shares, including reinvesting USd dividends and I have also converted some GBP to USD and vice versa within the interactve investor to buy US and UK shares respectively.The original (large) amount I converted a number of years back from GBP to USD was using Transferwise. I have not since used anyone to convert the USD back to GBP, the only conversions I have done has been within the ii platform as mentioned in the above para.All the above related to my GIA.When doing my CGT calculations for tax return, I have only ever included gains/losses on shares bought/sold and for any US shares I have converted the USD amount to GBP using FX rates at the time of the buys and sells.Have I missed anything with regards to CGT, particularly around FX conversions? I suspect not given the previous posts on this thread if I assume ii fx conversions I have done (back and forth gbp usd) is inside bank accounts(s) held by ii?What about the initial conversion from GBP to USD done via transferwise? the conversions in ii I have done might relate to some cash that was initially converted to USD in transferwise? But if both transferwise and ii conversions were all done by bank accounts in respective platforms, then I have not missed anything?If and when I convert USD to GBP via transferwise, I assume nothing to do for CGT?

The only time I've declared CGT gains on conversion is when I've specifically bought and sold sterling to speculate on movements between it and other currencies.So are the rules around FX not being taxable on conversion due to the FX conversion transaction occuring in a bank account, or due to the FX conversion being in the course of running the account, or due to both?Just to confirm, in my situaiton (as outline din my previous post), the only gains/losses due to FX that need to be incorporated into any CGT calculation is when the shares are bought/sold? Not when its simply just a FX conversion (wherever that takes places)?I'd suggest a read through of the foreign currency pages starting here to understand the nuances: https://www.gov.uk/hmrc-internal-manuals/capital-gains-manual/cg78300But a summary would be that if you are holding foreign currency in a bank account (including the client money account of your investment platform, to which you have a trust claim) and it gains or loses value relative to your home currency, then your bank deposits are considered a simple debt and will therefore not give rise to a chargeable gain. Likewise foreign currency held for personal expenditure outside the UK is exempt. But there are caveats, such as where the foreign currency was received as income, and likely where the individual is explicitly engaged in currency speculation.When shares are bought and sold, then the sterling value of the shares is likely to be equal to the value in base currency at the prevailing exchange rate. So any FX that needs to be incorporated will already be included in the normal CGT calculations where you would determine the GBP value at acquisition and disposal.1 -

If you want to pay CGT on your FX gains twice HMRC won't stop you but I'd contend 1. you've already been taxed on the FX gain or given relief on the loss when you sold the investment and made the conversion to sterling for calculation purposes, and 2. the brokerage account falls under the foreign currency bank account simplification introduced in 2012. (My US brokerage account can be used for day to day spending - it even came with a cheque book.)itwasntme001 said:wmb194 said:

Given your use of the USD was in the course of running the account and FX gains and losses will have been incorporated in your CGT calculations when selling shares I'd say no. This is how I've always treated it and I think it fits with HMRC's guidance.itwasntme001 said:I've been in a similar situation to the OP in that I have converted some GBP to USD some time back to invest in US shares. Since then I have done some buying and selling of US shares, including reinvesting USd dividends and I have also converted some GBP to USD and vice versa within the interactve investor to buy US and UK shares respectively.The original (large) amount I converted a number of years back from GBP to USD was using Transferwise. I have not since used anyone to convert the USD back to GBP, the only conversions I have done has been within the ii platform as mentioned in the above para.All the above related to my GIA.When doing my CGT calculations for tax return, I have only ever included gains/losses on shares bought/sold and for any US shares I have converted the USD amount to GBP using FX rates at the time of the buys and sells.Have I missed anything with regards to CGT, particularly around FX conversions? I suspect not given the previous posts on this thread if I assume ii fx conversions I have done (back and forth gbp usd) is inside bank accounts(s) held by ii?What about the initial conversion from GBP to USD done via transferwise? the conversions in ii I have done might relate to some cash that was initially converted to USD in transferwise? But if both transferwise and ii conversions were all done by bank accounts in respective platforms, then I have not missed anything?If and when I convert USD to GBP via transferwise, I assume nothing to do for CGT?

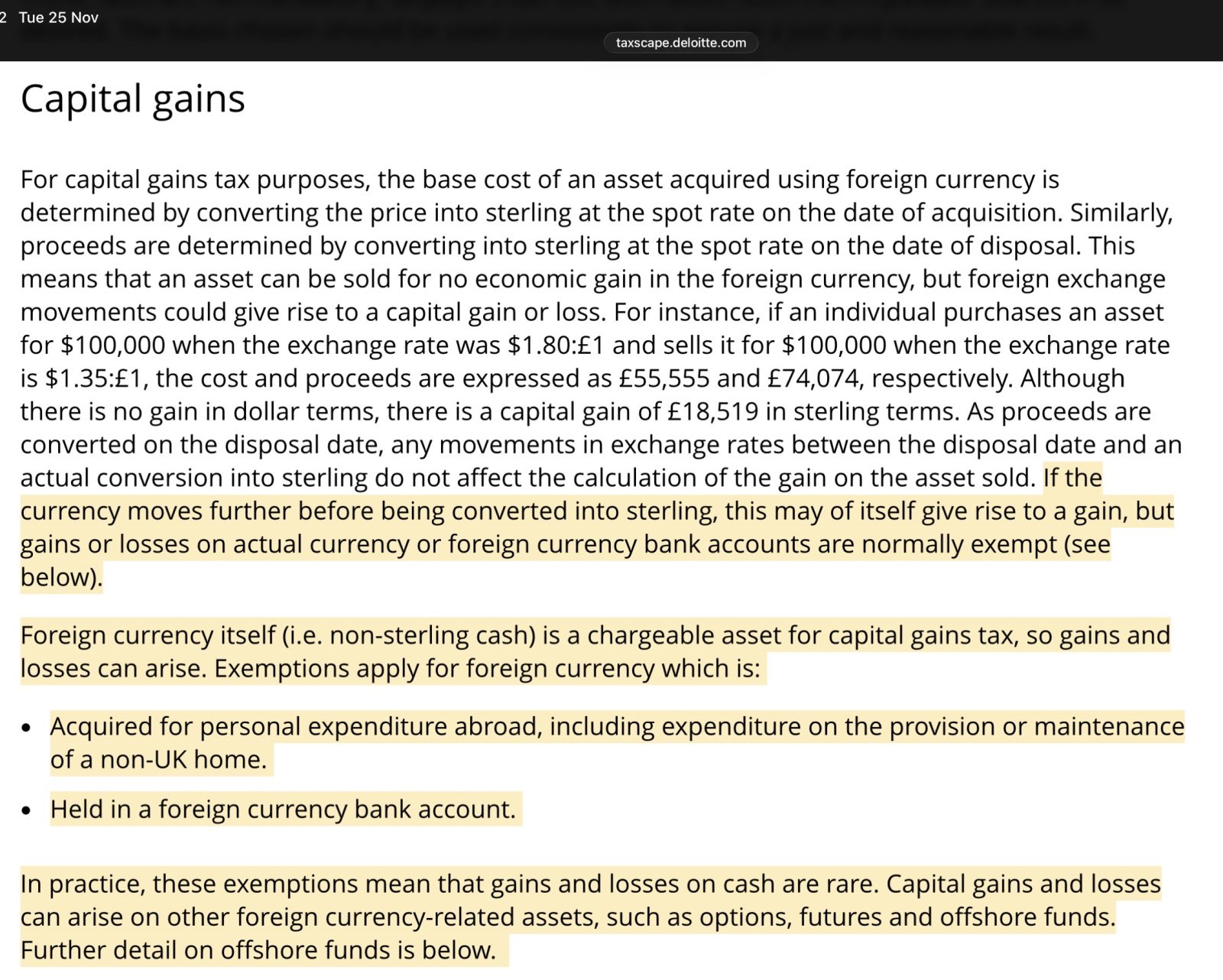

The only time I've declared CGT gains on conversion is when I've specifically bought and sold sterling to speculate on movements between it and other currencies.So are the rules around FX not being taxable on conversion due to the FX conversion transaction occuring in a bank account, or due to the FX conversion being in the course of running the account, or due to both?Just to confirm, in my situaiton (as outline din my previous post), the only gains/losses due to FX that need to be incorporated into any CGT calculation is when the shares are bought/sold? Not when its simply just a FX conversion (wherever that takes places)?https://taxscape.deloitte.com/article/foreign-exchange.aspx#:~:text=If%20the%20currency%20moves%20further,rather%20than%20capital%20gains%20tax.

https://www.gov.uk/hmrc-internal-manuals/capital-gains-manual/cg78320

"From 6 April 2012 the treatment of foreign currency bank accounts was simplified. From that date the treatment of foreign currency bank accounts for individuals ... were aligned with the treatment of ‘simple debts’. TCGA92/S252. Such debts will not give rise to chargeable gains (or allowable losses) in the hands of the original creditor." 1

1 -

Thanks both. Just to be clear, is the wording on FX exemption for CGT on gains/losses in the market moves in currency held in a foreign bank account or when an actual conversion takes place in the foreign account.If I convert from USD to GBP, the USD in the foreign account is moved to GBP in the local account. And vice versa. So confusing what the exemption actually relates to - just the value moving due to FX (mark to market) or actual FX conversion.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards