We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Getting slightly cold feet about SIPPs

Comments

-

Moving into high Bonds funds will do precisely nothing to protect against a Bond crash and Stocks/Bonds can crash together. It would be a massive gamble to only expect a Stocks crash. The world is currently mental and very unpredictable.

The only things that will protect are either Cash /short term money market funds or individual Gilts.With an amount as huge as OP has, I’m not sure how much of a fund switch will protect such a big lump sum, half the whole pot maybe?I suppose it depends when a regular income will start being drawn.People may well protect the 25% they expect and not consider the other 75% that could drop 10/20/30% , thus reducing the tax free element by £50k or more.With that size of pot I would take professional advice.0 -

Moving into high Bonds funds will do precisely nothing to protect against a Bond crash and Stocks/Bonds can crash together. It would be a massive gamble to only expect a Stocks crash.SVaz said:Moving into high Bonds funds will do precisely nothing to protect against a Bond crash and Stocks/Bonds can crash together. It would be a massive gamble to only expect a Stocks crash. The world is currently mental and very unpredictable.

The only things that will protect are either Cash /short term money market funds or individual Gilts.With an amount as huge as OP has, I’m not sure how much of a fund switch will protect such a big lump sum, half the whole pot maybe?I suppose it depends when a regular income will start being drawn.People may well protect the 25% they expect and not consider the other 75% that could drop 10/20/30% , thus reducing the tax free element by £50k or more.With that size of pot I would take professional advice.

Corporate bond funds may well follow stocks down.

However you would not expect a fund based on Government bonds ( UK only or a mix) to follow stocks down.1 -

Just because it’s unlikely to happen again so soon after the last time, I certainly wouldn’t be putting a huge lump of cash in them.Gilts held to maturity may be a safe bet, Bond funds, even if holding all Govt. ones, I wouldn’t be trusting them.So many people were badly burned last time because they thought their lifestyled funds were totally safe, I can’t imagine the distress of being ready to retire and seeing your pot reduce by 25%.

0

0 -

So many people were badly burned last time because they thought their lifestyled funds were totally safe, I can’t imagine the distress of being ready to retire and seeing your pot reduce by 25%.But annuity rates are up by an equivalent amount. So, they were safe for the purpose they were designed for.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

I noticed from your first post that you set up SIPPs accessible from 55 when you are 50/51. The usual age to access a SIPP for a 51 year old is 57. However, you can use the ISAs to fill the 55-57 gap, providing there is sufficient funds in your ISA element.

Regarding the 100% equities, At least VLS doesn't have as many eggs as in US stocks as many out there as there is a somewhat disporportioante 20% or so in UK, but if this is a good or bad thing for the future remains to be seen. I would feel uncomfortable to be 100% in equities right now, but everyone's opinion is different.

It looks like you may also want to take money in the next 3-4 years. Do you have any funds sitting as cash to prevent the risk of having to sell depressed assets in your 100% equity SIPPs and ISAs "if" the markets take a dive?

One thing I have just personally done is open up an additional SIPP which is entirely in ETF's (one world index fund ETF and one short term UK Gilt ETF), so that I can redistribute / rebalance, or move my entire holding of either between either (or into cash) in literally minutes. This gives me peace of mind. And as long as you have that, you're probably invested as best as you can be for yourself.

• The rich buy assets.

• The poor only have expenses.

• The middle class buy liabilities they think are assets.1 -

Hi. About 10-20k in cash, but otherwise yesDazed_and_C0nfused said:

Do you have other funds invested in anything else or is the £920k everything from a DC pension and ISA perspective?justcheckin said:Hi,

I consulted the forum before setting up SIPPs for myself and DH accessible at 55th birthdays now aged 50 and 51. These are both fully invested in VLS lifestrategy 100% equity as at the time, the horizon was quite long.

Plan is to use TFLS/PCLS as uni fees/help for children.

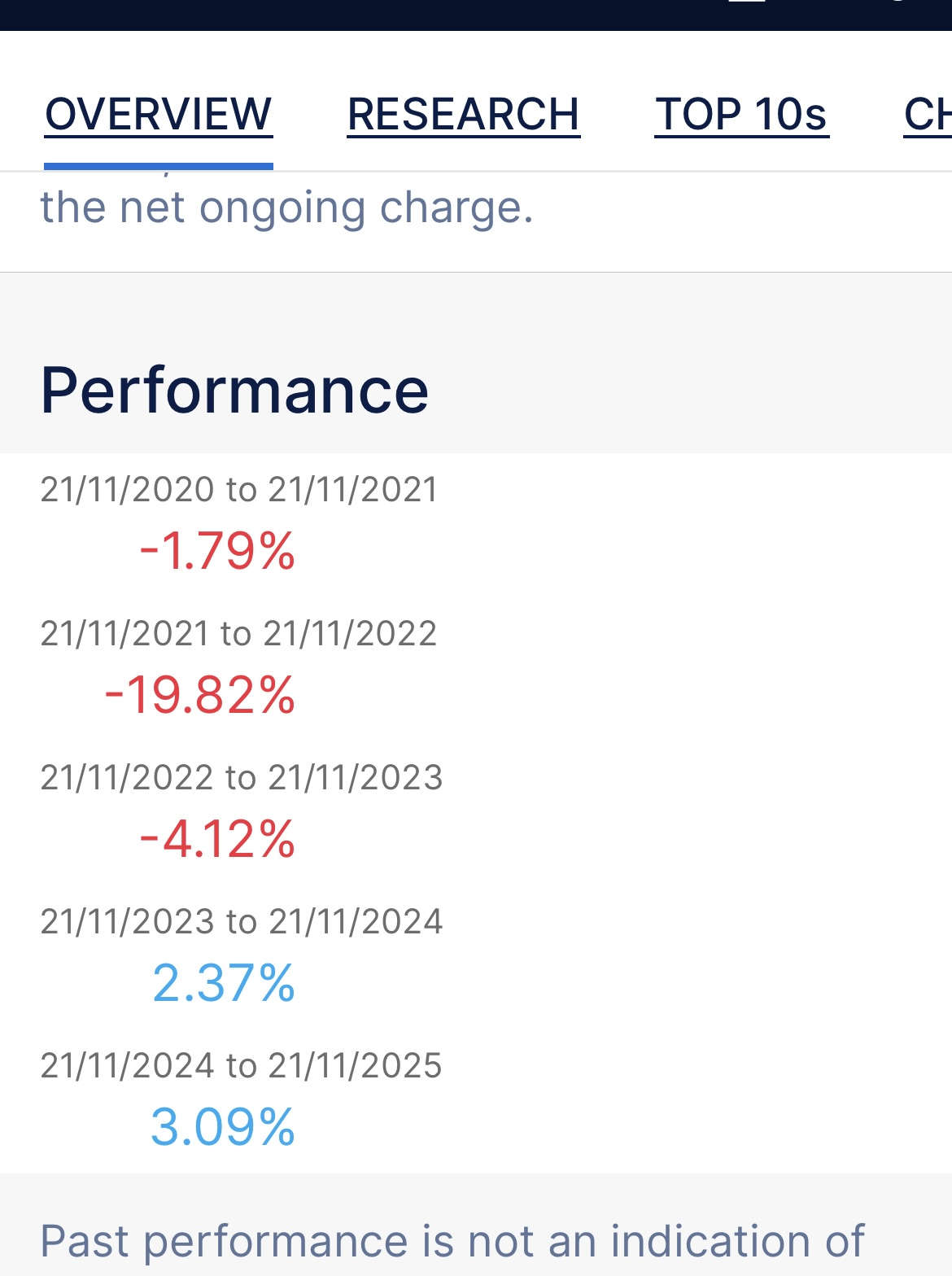

Increasingly as we approach the time we could take the TFLS, I am concerned about a tech-related market crash. We have combined (also in ISAs) £920k in vls 100 equity.

Would you consider rebalancing SIPPs/isas? We both also have DB pensions and likely full new SP.0 -

Fidelity SIPPs have a protected age if opened before 2021 of 55, due to the way they promoted the product, I understood?molerat said:First blip is MPA is changing to 57 from 6 April 2028 so you need to replan where your age 55 funds are coming from !0 -

Thank you everyone.

The idea was to use the TFLS to fund children's university. 4 children, going to uni in (just under) 2 yrs, 3 yrs, 6 and 7 yrs assuming no gap years and all go.0 -

Yes it was down to how the scheme rules were drafted at the timejustcheckin said:Fidelity SIPPs have a protected age if opened before 2021 of 55, due to the way they promoted the product, I understood?

https://www.fidelity.co.uk/normal-minimum-pension-age-nmpa/

"If you opened a SIPP with us or applied to transfer your pension to us before 4 November 2021 - you'll benefit from the Protected Pension Age of 55. This applies to any transfers or contributions you made to your pension on/before 3 November 2021, as well any future contributions."

You no longer have a suitable investment timescale to be in VLS100 (unless you just want a gamble) so it's time to reduce risk by building a multi asset portfolio aligning asset volatility to likely withdrawal dates. Money market funds and inflation linked gilts are offering a much better return these days so there isn't much opportunity-cost to being diversified anyway especially if equites are offering a likely lower than normal medium term return because of current valuations.

1 -

Plan 5 student loans are cheap enough that (in my opinion) they'd be better off taking the loans and placing your TFLS into ISAs and LISAs of their own.justcheckin said:The idea was to use the TFLS to fund children's university. 4 children, going to uni in (just under) 2 yrs, 3 yrs, 6 and 7 yrs assuming no gap years and all go.N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.8K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.4K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards