We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Are there any reasons not to invest in this?

I'm almost 41, and whilst I'm late to the game, I have become interested in investing in stocks.

Specifically, I narrowed it down to:

Platform: Trading 212 (Stocks & Shares ISA)

Fund: VUAG (Vanguard S&P 500 UCITS ETF – Accumulating).

Reason: Very low FX fee (0.15% per trade), no monthly account fee on the ISA.

I'm all about convenience, and I intend, if I go ahead with this, to automate monthly deposits. Initially, I was thinking £150 per month, but after doing the research, I now know it's not a bad idea to bang as much as you can in, as early as you can. So, I'd probably be better putting in £500 a month, and then increasing it to a higher figure as soon as I'm able to (or as soon as I decide to).

It's an idea that seems to be consistently on my radar because not only do I see stuff about this popping up everywhere on socials from FA's I follow, I also can't shake the sense that I'm missing out on an opportunity to build future wealth. Add to that the sense of regret that I'm "too late to the game", but we all know the sayings; the best time to start is yesterday, yadda yadda.

I can afford the £500 a month. I'm lucky enough to have created a situation for myself where I won't even notice it. Whereas 5 years ago, I was overworked and underpaid. That's not the case anymore. Aside from the £500 a month, I have around £15,000 of a "safety net" across my bank accounts, so I could easily do more than £500, but I don't think it's a bad starting point. I will increase it at some point, probably in 2026.

Is all this stuff I hear about an 8/10% average over 10/20 years too good to be true? I'm in it for the long haul, so I'm prepared to ride the waves, but market fluctuations aside, is there any reason not to go ahead with my plan?

Comments

-

This not very diversified. Why have you decide to restrict your investments to only shares traded on the US S&P500? What happens if the US Dollar weakens against Sterling?I am an Independent Financial Adviser. Any comments I make here are intended for information / discussion only. Nothing I post here should be construed as advice. If you are looking for individual financial advice, please contact a local Independent Financial Adviser.2

-

I'm in it for the long haul, so I'm prepared to ride the waves, but market fluctuations aside, is there any reason not to go ahead with my plan?

This is the key point. An S&P tracker can be potentially very volatile, a drop of 40% at some point would not be that shocking . So you need to be mentally prepared for that. On the other hand it will be a while until you have built up significant funds and if it happens soon, then you will be buying at cheap prices.

Most investors have been drifting away from the US in recent months over fears of a bubble, and diversifying into other regions. Have you thought about investing in a global index rather than just a US one?

Do you have a pension with your job? It can be better to invest via a pension, although it depends what sort it is.

2 -

HappyHarry said:This not very diversified. Why have you decide to restrict your investments to only shares traded on the US S&P500? What happens if the US Dollar weakens against Sterling?

I'd be going for this based on historical data, and historically (over the last 20 years, for instance) the S&P 500 has outperformed global. Diversifying sounds great, and I'm sure there are pros, but if you're looking ahead 20 years, the chances are much higher that you're better off with the S&P 500. That's based on all I've discovered, of course, not unless what I've found out isn't true.Albermarle said:I'm in it for the long haul, so I'm prepared to ride the waves, but market fluctuations aside, is there any reason not to go ahead with my plan?

This is the key point. An S&P tracker can be potentially very volatile, a drop of 40% at some point would not be that shocking . So you need to be mentally prepared for that. On the other hand it will be a while until you have built up significant funds and if it happens soon, then you will be buying at cheap prices.

Most investors have been drifting away from the US in recent months over fears of a bubble, and diversifying into other regions. Have you thought about investing in a global index rather than just a US one?

Do you have a pension with your job? It can be better to invest via a pension, although it depends what sort it is.

I only started paying into a pension (I hate that word, it's so depressing) 3 years ago and have been doing 8% + 3% from my employer. Until last month, I reduced it to 5% from me, because I'm launching a business and have high hopes for it, so I want to see how things go with that, since if things go better than expected, I'd eventually be leaving my job anyway. It's just a regular one with Smart Pension.

I've formulated a plan to retire at 50 with goals and targets to hit that get me to at least a couple of million total wealth. I'm far off it right now, but I'm gunna give it a good go.0 -

There's nothing more demotivating than seeing your investment losing value in early days and there is a higher chance than usual in the US market - my main issue is that Nvidia is currently valued more than entire UK..

But yeah, it could be true, it could be false - and putting all your money into one of these guesses is a gamble.

So spread your bets across, normally I'd say go for a global tracker but even they have 60%+ US exposure")

Id go for something like 20% into the one you suggested and 80% in VEU?

That's just my opinion. Good luck.

0 -

Apparently, the market is taking a battering at the moment, so would this not actually be a good time to strike?Newbie_John said:There's nothing more demotivating than seeing your investment losing value in early days and there is a higher chance than usual in the US market - my main issue is that Nvidia is currently valued more than entire UK..

But yeah, it could be true, it could be false - and putting all your money into one of these guesses is a gamble.

So spread your bets across, normally I'd say go for a global tracker but even they have 60%+ US exposure

Id go for something like 20% into the one you suggested and 80% in VEU?

That's just my opinion. Good luck.0 -

Your plan was a 10 years long investment with monthly top ups. Over that period there will be ups and downs. It may gain 40% one year it may lose 40% one year. Anything is possible and nobody knows for sure what next week, month, year will bring.

All we say here is that it's risky to put all your investment in just US equity, if you diversify than you're likely sustain lower loses if they occur.

It's really up to you what you decide, diversify and only invest money you can accept to lose.1 -

Specifically, I narrowed it down to:

Platform: Trading 212 (Stocks & Shares ISA)

Fund: VUAG (Vanguard S&P 500 UCITS ETF – Accumulating).

Reason: Very low FX fee (0.15% per trade), no monthly account fee on the ISA.

That is poor quality investing.

Remember that US equities cycle against global. Part of that reason is currency movements. You are not based in dollars but Sterling. If Sterling goes up 30% against the dollar then you need the S&P500 to gain 30% just to stand still.

Clearly, this cycle has had US equities as best. Nobody know when the cycles will switch to Global. However, this year global has beaten US. The pound has risen in that period. You are gambling on US equities after a significant gain cycle, when it's not far off the time you usually see it swing the other way. It may have already started. It may be a blip. However, you are putting all your eggs in one basket.

A global tracker would include around 60% US equities but the rest of the world too.

Going by the more suitable global tracker and not picking the S&P500 due to recency gains (remember that the previous cycle had is as the wost major market. Looking only at recency gives you a false picture)

Annualised returns (nominal - not inflation adjusted):

Over any 12 month period since 2015, the median return is 12%. With the worst being -37% and best +66%

However, over a 120-month period, the median is 10% with worst being -1% and best being 25%. (noting that the worst is the decade that took place just before the above-average gains from the US.

Over a 240 month period, the median is 11%, worst is 4% and best is 18%.

The longer you leave the investment, the closer it will gravitate towards the long term average. 10 years is very short term for a regular contribution and only the first contribution gets 10 years. Every contribution thereafter gets one month less than the one before. Your timescale is still fine though.I'd be going for this based on historical data, and historically (over the last 20 years, for instance) the S&P 500 has outperformed global.

That is not historical. That is recency and has bias. You are effectively picked a timescale that starts just after one of the biggest US equities crashes in generations.

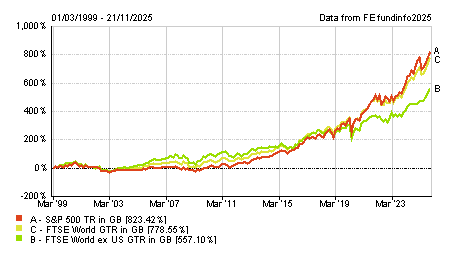

This chart starts from March 1999 to date. It is effectively bringing two cycles together and as a result, not much in it. You can see all world is better at the start and US better at the end.

the previous tech boom cycle started around 1995 and we can see below that the US pulled ahead (plus US had underperformed global in the previous

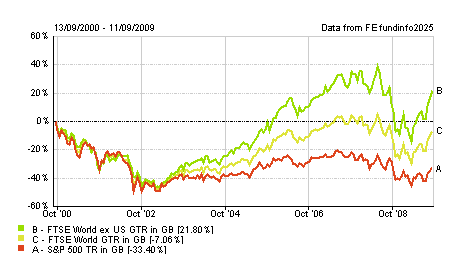

The dot.com crash started 13th Sept 2000 and this is the decade that followed. Much of that was down to exchange rates.

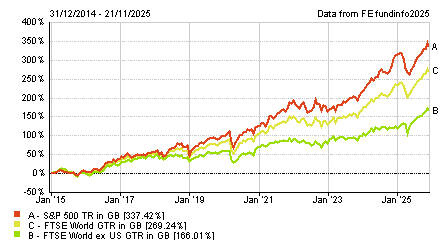

The US only started outperforming global from around 2015

Under Trump, the dollar has fallen and global has been better. Is the start of the next cycle? - we don't know but you are betting on US being best all of the time when history does not support that.

but if you're looking ahead 20 years, the chances are much higher that you're better off with the S&P 500.

The historical data does not suggest that.I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.10 -

Newbie_John said:There's nothing more demotivating than seeing your investment losing value in early days and there is a higher chance than usual in the US market - my main issue is that Nvidia is currently valued more than entire UK..

But yeah, it could be true, it could be false - and putting all your money into one of these guesses is a gamble.

So spread your bets across, normally I'd say go for a global tracker but even they have 60%+ US exposure

Id go for something like 20% into the one you suggested and 80% in VEU?

That's just my opinion. Good luck.

With specific regard to Navidia and the tech sector in general there is a potential dark cloud approaching in 2027.

Pretty much all of Navidia chips are manufactured by TSMC in Taiwan.

As everyone should be aware, China has intimated that Taiwan should 'return' to the comforting embrace of the PRC in 2027 -

https://dominotheory.com/is-china-invading-taiwan-in-2027/#:~:text=However, China has dismissed 2027,change quickly,” Milley said.

Sensibly TSMC is trying to mitigate this geopolitical risk, by expanding its Chip fab centres in other countries, but the fact remains Taiwan's independence and TSMC's manufacturing within that border remains critically important to the likes of Navidia in producing the high end chips driving the AI boom.

This alone should give the OP pause for thought in betting his long term investment returns on a single tech heavy index rather than a more widely spread global index.

0 -

Not sure where you got that idea ?Dannydee333 said:

Apparently, the market is taking a battering at the moment, so would this not actually be a good time to strike?Newbie_John said:There's nothing more demotivating than seeing your investment losing value in early days and there is a higher chance than usual in the US market - my main issue is that Nvidia is currently valued more than entire UK..

But yeah, it could be true, it could be false - and putting all your money into one of these guesses is a gamble.

So spread your bets across, normally I'd say go for a global tracker but even they have 60%+ US exposure

Id go for something like 20% into the one you suggested and 80% in VEU?

That's just my opinion. Good luck.

The facts are that the index in question - the S&P 500 - is down in the last month by 2%, but since Jan 1st, it is still up 12 %.

The media tend to go OTT about small corrections downwards, and rarely report any upswings.

Bad news makes better headlines/clickbait.

1 -

The S&P500 is within a few percent of its all time high, and has recently experienced double digit growth in the space of just 6 months. Social media can paint a rather different picture, and is not a great place to do research about investing.Dannydee333 said:

Apparently, the market is taking a battering at the moment, so would this not actually be a good time to strike?Newbie_John said:There's nothing more demotivating than seeing your investment losing value in early days and there is a higher chance than usual in the US market - my main issue is that Nvidia is currently valued more than entire UK..

But yeah, it could be true, it could be false - and putting all your money into one of these guesses is a gamble.

So spread your bets across, normally I'd say go for a global tracker but even they have 60%+ US exposure

Id go for something like 20% into the one you suggested and 80% in VEU?

That's just my opinion. Good luck.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.4K Banking & Borrowing

- 254.1K Reduce Debt & Boost Income

- 455K Spending & Discounts

- 246.5K Work, Benefits & Business

- 602.8K Mortgages, Homes & Bills

- 178K Life & Family

- 260.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards