We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Defined Benefit Pension

confusedpension

Posts: 3 Newbie

Hi, I have a Defined Benefit Pension which is less than £30k. I wanted to transfer this across to a Defined Contribution Scheme, but so far I cannot find a provider who is will to take it. This means I am going to have to take 25% tax free, which is just under £6k, an the remainder as an annuity - works out about £80 per month. Just feeling annoyed because I don't have any other pension & would have preferred to transfer it to a drawdown scheme which would have given me more flexibility. Why am I unable to transfer it? Thanks

0

Comments

-

If you have a transfer value under £30k and no safeguarded benefits then most providers should accept it. What are you asking them that gets the negative response?I’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.0 -

Why do you think you will be better off transferring it out? The £80 pm is not an annuity and will almost certainly have some form of index linking to it.0

-

Doesn't sound like a DB from the way you describe having to take it.........Gettin' There, Wherever There is......

I have a dodgy "i" key, so ignore spelling errors due to "i" issues, ...I blame Apple 0

0 -

Are you sure your existing scheme is defined benefit? When you talk about 25% tax free and buying an annuity with the rest that sounds like a defined contribution scheme.

Maybe the receiving schemes hear defined benefit and just say No.0 -

Sounds like a DB scheme, just OP using a spot of DC terminology.confusedpension said:Hi, I have a Defined Benefit Pension which is less than £30k. I wanted to transfer this across to a Defined Contribution Scheme, but so far I cannot find a provider who is will to take it. This means I am going to have to take 25% tax free, which is just under £6k, a the remainder as an annuity - works out about £80 per month. Just feeling annoyed because I don't have any other pension & would have preferred to transfer it to a drawdown scheme which would have given me more flexibility. Why am I unable to transfer it? Thanks

It's entirely up to providers what they will or won't accept - with one exception: stakeholder pensions. Set up one of those (still a couple open to new direct customer business) and use that.

Alternatively, if you have no other (non-state) pension provision, you could ask the scheme about 'total commutation on the grounds of triviality' if you have reached the age of at least 55.

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1 -

The biggest issue here is “I don’t have any other pension”.In that case you shouldn’t touch the other “pension” but take immediate steps to start a pension which will support you post working life.Mortgage free

Vocational freedom has arrived0 -

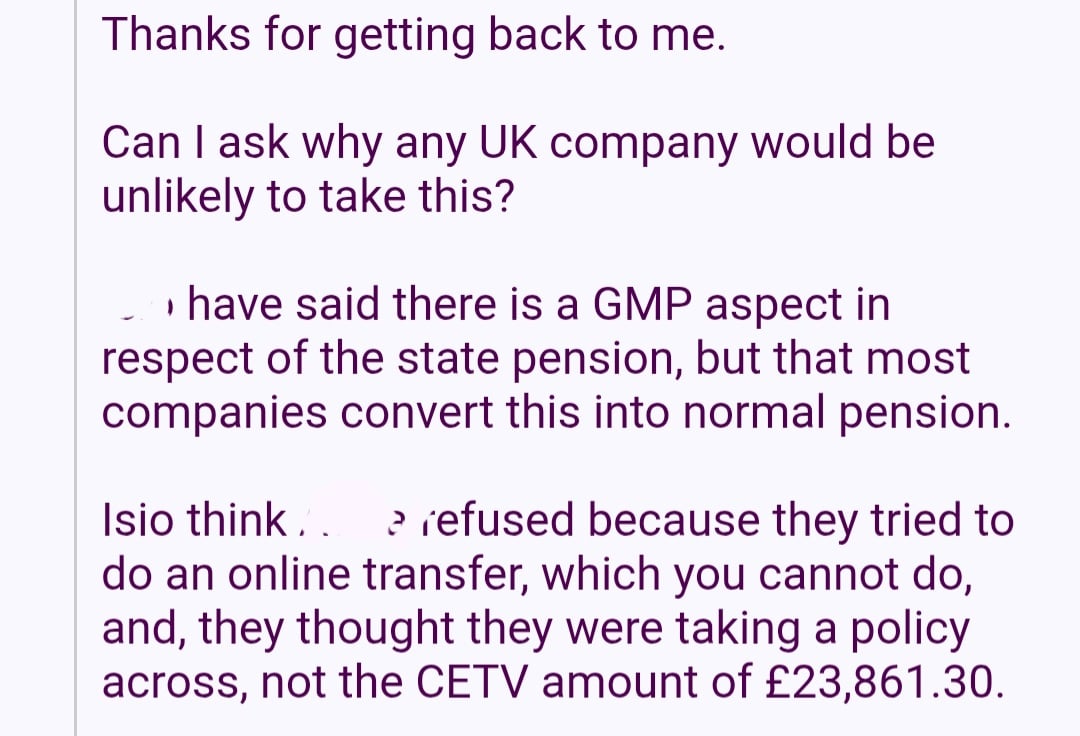

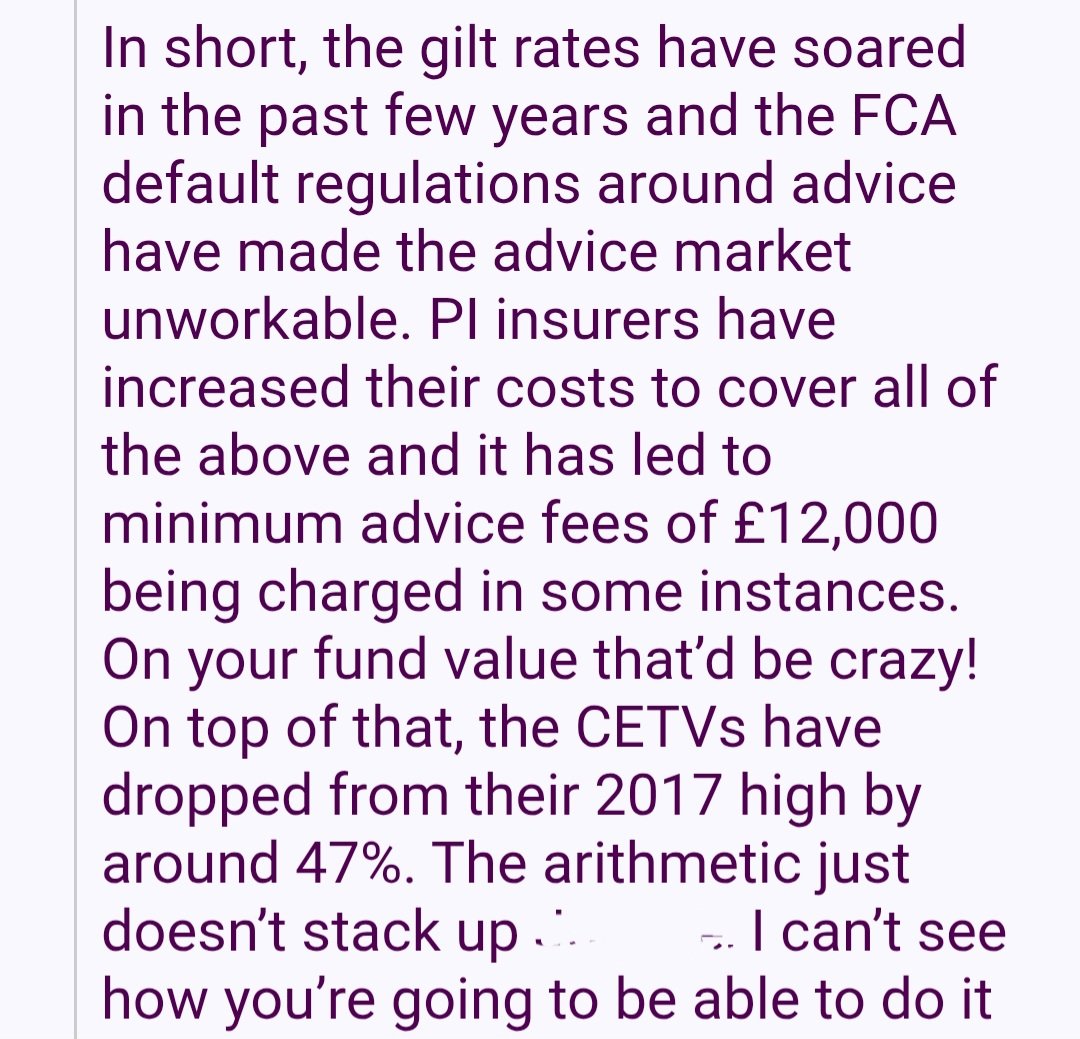

Hi, have attached my question & FA response.

0

0 -

The transfer value is under £30K so advice isn't mandatory, so that's irrelevant.

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

...depending on how that interacts with state benefits, especially if OP's state pension is going to less than full (meaning they may be eligible for Pension Credit or whatever is around at the time).sheslookinhot said:The biggest issue here is “I don’t have any other pension”.In that case you shouldn’t touch the other “pension” but take immediate steps to start a pension which will support you post working life.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

Thanks all0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards