We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

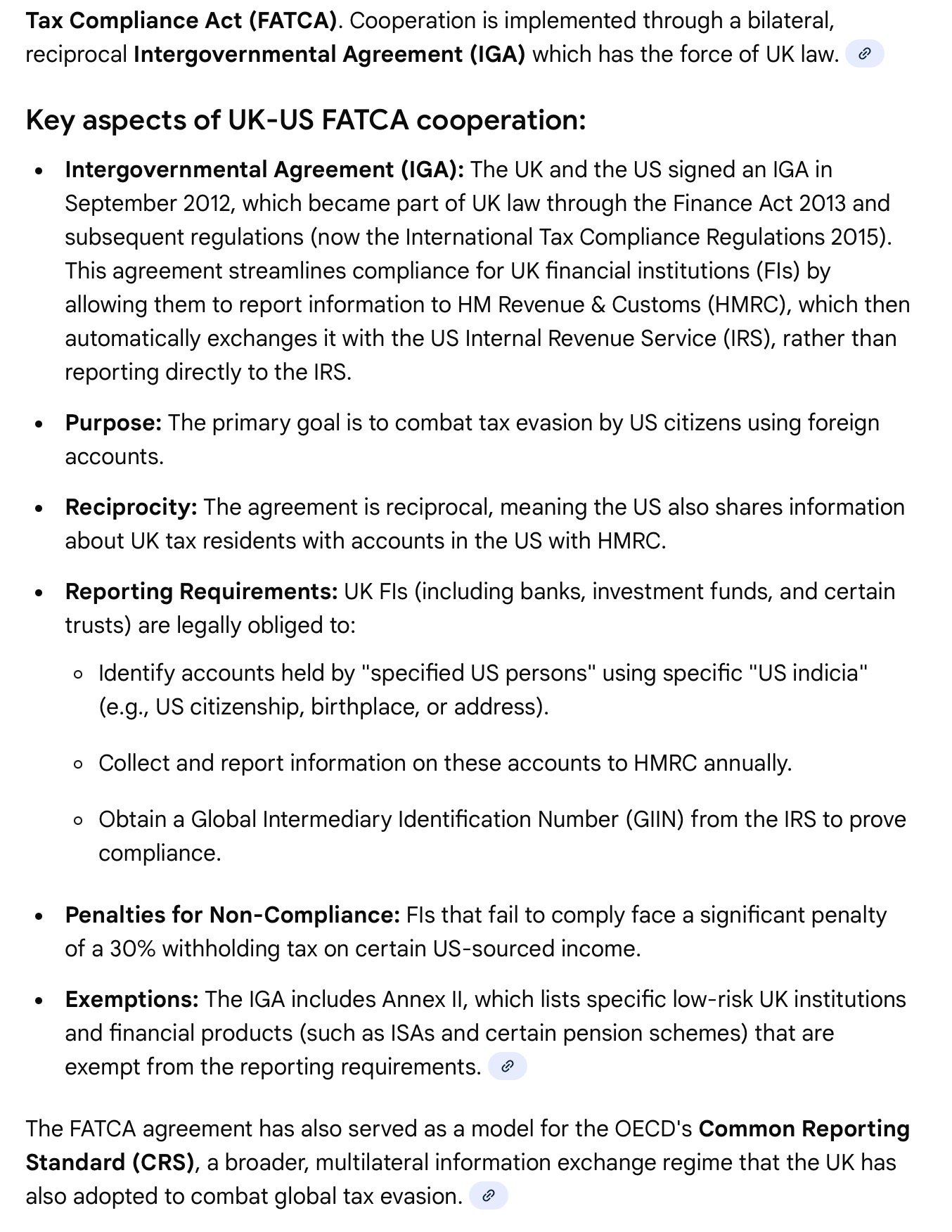

US Citizen

My mother was born and raised in the USA, but in the mid 60’s while working as a nurse overseas, she met then married my father, who worked for the Crown in the diplomatic service.

In the early 90’s she started opening ISA’s and investment accounts without issue.

Now this month, financial institutions (Fidelity Investments and Aviva), are starting to report they will be closing down her ISA’s and investment accounts (within 30 days), because she was born in the USA, and is still a US citizen, even though they have and are retired here in the UK for over 25 years.

Supposedly, if my father wasn’t retired, he would still be current Crown Employee, so everything would still be okay but he’s 84 and receiving his Crown pension.

Can they really do this is, it’s sounds totally unfair and madness!

Comments

-

Yup, look up Facta. Lots of companies don't want to deal with the reporting requirements and potential liabilities of US citizens. It's been a thing for a long time so I'm surprised you're not aware of it.Divefrosty said:My mother was born and raised in the USA, but in the mid 60’s while working as a nurse overseas, she met then married my father, who worked for the Crown in the diplomatic service.

In the early 90’s she started opening ISA’s and investment accounts without issue.

Now this month, financial institutions (Fidelity Investments and Aviva), are starting to report they will be closing down her ISA’s and investment accounts (within 30 days), because she was born in the USA, and is still a US citizen, even though they have and are retired here in the UK for over 25 years.

Supposedly, if my father wasn’t retired, he would still be current Crown Employee, so everything would still be okay but he’s 84 and receiving his Crown pension.

Can they really do this is, it’s sounds totally unfair and madness!

https://en.wikipedia.org/wiki/Foreign_Account_Tax_Compliance_Act

2 -

She could always renounce her US citizenship?

Blame the US tax policy for taxing citizens on their worldwide income even if they have long left..3 -

Presumably she has been correctly filing US tax returns every year? Given that the US doesn't recognise ISAs as tax exempt and so she would have needed to pay tax on the income that they generated...5

-

Is this because the USA IRS operate Global Taxation?Divefrosty said:My mother was born and raised in the USA, but in the mid 60’s while working as a nurse overseas, she met then married my father, who worked for the Crown in the diplomatic service.

In the early 90’s she started opening ISA’s and investment accounts without issue.

Now this month, financial institutions (Fidelity Investments and Aviva), are starting to report they will be closing down her ISA’s and investment accounts (within 30 days), because she was born in the USA, and is still a US citizen, even though they have and are retired here in the UK for over 25 years.

Supposedly, if my father wasn’t retired, he would still be current Crown Employee, so everything would still be okay but he’s 84 and receiving his Crown pension.

Can they really do this is, it’s sounds totally unfair and madness!

https://www.irs.gov/individuals/international-taxpayers/frequently-asked-questions-about-international-individual-tax-matters

Possibly, the UK-based financial institutions do not wish to be incurring the costs of reporting for a minority of customers and prefer to suffer the loss of that volume of business. Particularly since the commercial relationships with USA and demands placed on foreign institutions have tightened in the recent months.

Is there an option for the accounts in your Mother's name to be transferred to accounts in your Father's name?

Has your Mother been filing tax returns and paying any liabilities arising over the past 25-years that she has been resident in UK?0 -

Isthisforreal99 said:She could always renounce her US citizenship?I read recently that, as part of the process to renounce US citizenship, you have to show that your US tax returns are up to date.Which might be a problem.N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.5 -

The US taxes its citizens in perpetuity no matter where on (or off) the planet they live. The US/UK tax treaty covers pensions reasonably well, so if your mother has any of those they are probably okay, but gains and interest anywhere else might be taxable to the US.Divefrosty said:

In the early 90’s she started opening ISA’s and investment accounts without issue.

In particular, the US doesn't recognise an ISA as any form of tax shelter. Problems compound if your mother holds any funds, OEICs, investment trusts, or ETFs, whether in an ISA or in a general investing account. These will be non-US domiciled, and the US has a special punitive tax rule for any US person who has the temerity to hold non-US funds or ETFs - Google "PFIC" and weep.

The bottom line is that your mother may have a large and possibly expensive US tax cleanup operation on her hands.

As you're seeing, because of FATCA's punitive and extraterritorial nature, most UK providers will now refuse to accept US citizen clients. A few still do, however. Reportedly, Hargreaves Lansdown, Interactive Brokers and Charles Stanley. Moving to one of these before the 30-day deadline given by Aviva and Fidelity would at least preserve your mother's ISA allowances and any unrealised capital gains while you look for a more permanent option.Divefrosty said:

Now this month, financial institutions (Fidelity Investments and Aviva), are starting to report they will be closing down her ISA’s and investment accounts (within 30 days), because she was born in the USA, and is still a US citizen, even though they have and are retired here in the UK for over 25 years.

For your mother, assuming she has absolutely no plan to ever live in the US in future, renouncing her US citizenship looks like it could be a good option. She'll give up nothing of any value, but gain the freedom to live her life in the UK now free from the many restrictions of US tax rules. One thing to watch for there though is the US's spiteful 'expatriation tax', which has the capacity to destroy future planned finances. If thinking of that route, take extreme care to first understand the full US tax implications of this piece of congressional nastiness.

Finally, you might want to check your own situation. It is possible (depending on some fiddly rules) that because your mother is a US citizen, you might also be an "accidental American" - that is, you yourself could be a US citizen, even though you might never have set foot in the US.

Charming, isn't it?

8 -

-

Your mother is a US citizen so must do an annual US tax return every year for life, the US are in a minority that says their citizens always are liable for taxes no matter where in the world they live, in principle. In practice the UK and US have a tax treaty meaning that whilst she has to do the return she can net off whatever taxes she has paid in the UK. Given the UK is generally a higher tax regime than the US very few end up having to pay any tax but the return must still be done. There are exceptions though, like an ISA is a tax free wrapper for HMRC but not for the IRSDivefrosty said:My mother was born and raised in the USA, but in the mid 60’s while working as a nurse overseas, she met then married my father, who worked for the Crown in the diplomatic service.

In the early 90’s she started opening ISA’s and investment accounts without issue.

Now this month, financial institutions (Fidelity Investments and Aviva), are starting to report they will be closing down her ISA’s and investment accounts (within 30 days), because she was born in the USA, and is still a US citizen, even though they have and are retired here in the UK for over 25 years.

Supposedly, if my father wasn’t retired, he would still be current Crown Employee, so everything would still be okay but he’s 84 and receiving his Crown pension.

Can they really do this is, it’s sounds totally unfair and madness!

Most governments and HMRC/IRS equivalents are concerned their citizens may not be declaring all the money they are making to avoid paying taxes. Hence all the hype last year when it was said eBay, Vinted etc now have to report people with anything above token annual sales.

Banks have a long time had to report to their local tax office in many countries on their customers earnings etc but given the US considers tax globally they require banks globally to do so the same for any US citizens that may be their customer.

This has being going for some time and when it was originally introduced some financial institutes decided it was too much hard work for how little those customers bring to their P&L so withdrew services from them. The rules are changing again in 2027 but FIs have been told to be ready for it in 2026, as such some will be making changes to become/stay compliant and others will withdraw services to US citizens to avoid the cost of the regulation.1 -

So you have to pay what can only be described as a fine of $2,350 for giving up your citizenship. That's outrageous!Emmia said:

This thread reminds me of when you were asked if you had Canadian citizenship, although that may have been only for buying shares.0 -

Depending on your financial position, giving it up could be cheap at two, three or four times the price.nottsphil said:

So you have to pay what can only be described as a fine of $2,350 for giving up your citizenship. That's outrageous!Emmia said:

This thread reminds me of when you were asked if you had Canadian citizenship, although that may have been only for buying shares.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards