We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Should I change my gilt investments

Comments

-

Yes that is the fund, and thank you for taking the time to explain about the rise in annuity rates. Makes sense had I wanted to take an annuity. Although, I still feel that it was only by chance that the lifestyle fund has preserved the value of the annuity, and not because I was invested in guilts. Had I been invested in something other than the gilt fund, I may not have lost so much or even profited, and had more to purchase an annuity, or am I missing something?QrizB said:

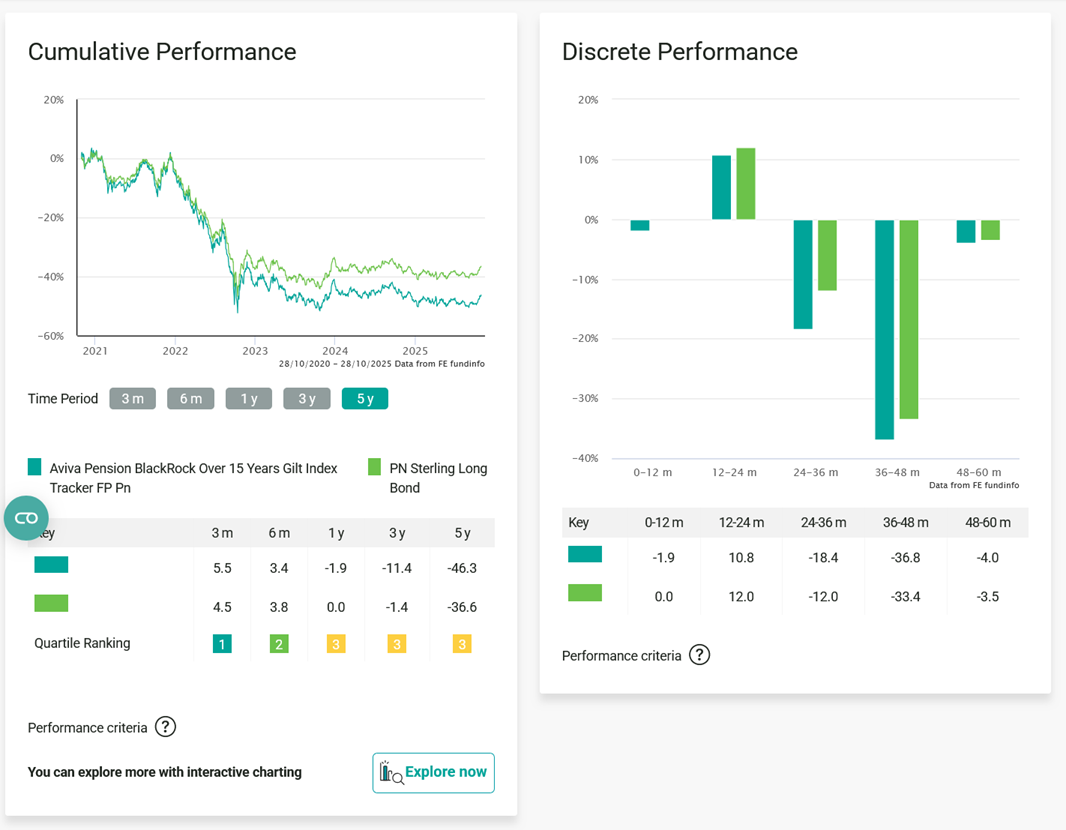

This one?Oranda said:

The fund is BlackRock Over 15 years Gilt Index Tracker.QrizB said:Oranda said:All I can see on performance of the guilt index tracker fund I’m in for the last 5 years is -12.0%, -37%, -12.9%,10% and latest is -9.5%. So that was the reason for my initial question as I’m 4 months from retirement.That's unusually poor.What's the name of the fund?https://www.trustnet.com/factsheets/p/lm60/aviva-pen-blackrock-over-15-year-gilt-index-tracker-fp-pnThe current performance isn't quite as you state, but even so it's down almost 50% over 5 years:

Over those same five years, however, annuity rates have doubled.Oranda said:I lost around 30% of my pension pot 5 years before my retirement.Look at this post, for example:In 2021, £100k would have bought a 65-year-old an RPI-linked annuity of £2685 a year.Take that £100k and knock off 46% (the loss in your gilt fund over 5 years). You've now got £54k.In 2025, £54k will buy a 65-year-old an RPI-linked annuity of £2918 a year.So the gilt fund as done what it was designed to do; it's preserved the value of the annuity you'll be able to buy with your pension.

It is a low-risk fund for anyone intending to buy an annuity, and is exactly what would be expected for a lifestyle fund targeting an annuity purchase.Oranda said:My own fault I guess for not keeping an eye on it, and naively thinking it should have been low risk and "set and forget" as part of the "suggested" lifestyle process.

Still I am where I am now as they say, and minded to go drawdown rather than annuity. So still need decide if I should move out of the gilt fund to be in a better position short term whilst I take tax free cash over next 2 years.1 -

It would be in cash for the amount you plan to draw out over the next five years.Oranda said:

I'm aware I cant change it (hence my reference to spilt milk).dunstonh said:Still, I have read that others have suffered similarly, and nobody saw Covid or guilt crash.It's not to do with Covid, other than perhaps Covid extending the period of quantitative easing longer than it would have otherwise.Split milk now but don't really want to leave it there as I cant see it will recover with the next 2-3 years.Although gilts are the best performers of all the defensive options over the last 3 months and beating STMM over 6 months.

The bonds crash has happened. You cannot change that. Now it is starting a recovery, you are looking to avoid that recovery.

If you had £24K in that guilt fund and needed to crystallise it to take TFLS's over the next 2 years, would you leave it there, or move it to another fund?Although, I still feel that it was only by chance that the lifestyle fund has preserved the value of the annuity, and not because I was invested in guilts.That is because you do not know what you are talking about (that reads blunter than intended). The biggest influence on annuity rates is gilt yields.

Here is a chart showing 15 year gilt yields:

And here are annuity rates over the same period:

Spot the similarity?Had I been invested in something other than the gilt fund, I may not have lost so much or even profited, and had more to purchase an annuity, or am I missing something?You mean, like investing on the stockmarket and there being a 50% market crash just before the annuity was bought?

Lifestyling is not about making more money. It is about protecting what you have. Using gilts in an annuity lifestyle strategy is the perfect way of doing that. Historically, lifestyling reduces returns in over 70% of cases.

Moving to cash also reduces returns in the majority of cases. But it is still common sense to do it

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.4 -

The deposit fund would be for the 25% tax free cash. Tax free cash would not have the hedge of gilt yields so needs to be in cash. The 75% needs a hedge to annuity rates and gilts providesDRS1 said:

Earlier posts suggested the total uncrystallised was c £30k and that £8k of that was in something called Pension Deposit (which sounded like a cash/cash equivalent fund).SVaz said:If you are going to be taking tax free cash over the next 2 years ( is it £24k or 25% of £24k)

then that amount needs to be in either cash or short term money market funds already.

It’s not worth taking any risk with for such a short amount of time.

I confess I don't know how that tallies with £24k in the gilts fund and some other amount in equities.I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

If the tax free cash is already in a cash fund then it just leaves the ‘problem’ of the £24k in the Gilt fund.

When will this be taken as income and how much per year?If it’s in the next 2-5 years then it really needs to be protected, if the Gilt fund is not appropriate then it’s pretty much cash or a short term money market fund, it will still be liable to inflation but not a lot can be done about that.

I’ve got nearly 5 years income in a short term money fund and yes, it’s annoying that if it had still been invested it would have made an extra 15% instead of 4% this year but that’s the trade off between being secure and risking losing 15% or even more, right when it’s needed.

It’s also an emergency fund of sorts and means if I pack in working tomorrow, I don’t have to raid savings to live on, so it’s tax efficient.2 -

The OP has mentioned that he has taken some TFLS already and the crystallised funds are in a fund which sounds like a multi asset fund. And he is happy with the performance of that fund.SVaz said:If the tax free cash is already in a cash fund then it just leaves the ‘problem’ of the £24k in the Gilt fund.

When will this be taken as income and how much per year?If it’s in the next 2-5 years then it really needs to be protected, if the Gilt fund is not appropriate then it’s pretty much cash or a short term money market fund, it will still be liable to inflation but not a lot can be done about that.

I’ve got nearly 5 years income in a short term money fund and yes, it’s annoying that if it had still been invested it would have made an extra 15% instead of 4% this year but that’s the trade off between being secure and risking losing 15% or even more, right when it’s needed.

It’s also an emergency fund of sorts and means if I pack in working tomorrow, I don’t have to raid savings to live on, so it’s tax efficient.

I am not sure if that was a fund the OP picked or if it is something the pension provider has as a default fund for drawdown monies.

The added issue with that is that it is closed to new money. So who knows where the drawdown money will go when the OP takes the next instalment of TFLS. Something similar. Whatever it is seems like a good home for the money currently in the gilts fund (and the equity fund for that matter).

If it were me (and this is why I would never do drawdown) I would be very worried that I was moving the money out of something which may perform well into something which has become toppy and which may fall in value. Just look at the threads on here about imminent crashes in equities.

As you say the timeframe is important. The OP mentions 2 or 3 years but that is for taking the TFLS. It is not clear how long he thinks the drawdown funds will last.1 -

Thank you. That is helpful to know what you might do.It would be in cash for the amount you plan to draw out over the next five years.dunstonh said:

Yes, I have found some of your comments to be blunt. And yes I probably do not know what Im talking about in regards to the subject, but I am not an IFA which is why I was seeking some advice/learning/sanity here.That is because you do not know what you are talking about (that reads blunter than intended). The biggest influence on annuity rates is gilt yields.

Erm, No. But possibly a diversified assets fund would have been a better as I am not wanting to go with an annuity.dunstonh said:

You mean, like investing on the stockmarket and there being a 50% market crash just before the annuity was bought?

1 -

It was one of a number of funds that the pension provider suggested for the drawdown monies.I am not sure if that was a fund the OP picked or if it is something the pension provider has as a default fund for drawdown monies.

Ideally I would like the drawdown funds (around £200K in total) to last until I expire. So I guess should be looking at balancing those for the longer term. Reasonably healthy, so hope for a few more years yet.As you say the timeframe is important. The OP mentions 2 or 3 years but that is for taking the TFLS. It is not clear how long he thinks the drawdown funds will last.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 352.5K Banking & Borrowing

- 253.7K Reduce Debt & Boost Income

- 454.5K Spending & Discounts

- 245.5K Work, Benefits & Business

- 601.4K Mortgages, Homes & Bills

- 177.6K Life & Family

- 259.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards