We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

We're aware that some users are currently experiencing errors on the Forum. Our tech team is working to resolve the issue. Thanks for your patience.

Canadian Will and POA for UK assets

jem16

Posts: 19,852 Forumite

Might be too niche a question but thought I’d ask anyway.

My son and his wife have been in Canada since 2012 and no intention of returning to the UK. They’re currently organising Wills and POA there. Their solicitor has of course advised finding out the situation about accessing UK assets via their Canadian wills and POA.

Assets here are really just a small amount in UK banks plus a pension for both from when they worked here.

The suggestion was that they also do a UK will and POA but sounds a bit of an overkill and obviously extra expense.

Is this needed or will UK banks and pension providers accept their Canadian wills and POA?

0

Comments

-

Google says "yes, but ..." (I'll let you read up about the but ...)

An expat forum might be more helpful?Signature removed for peace of mind1 -

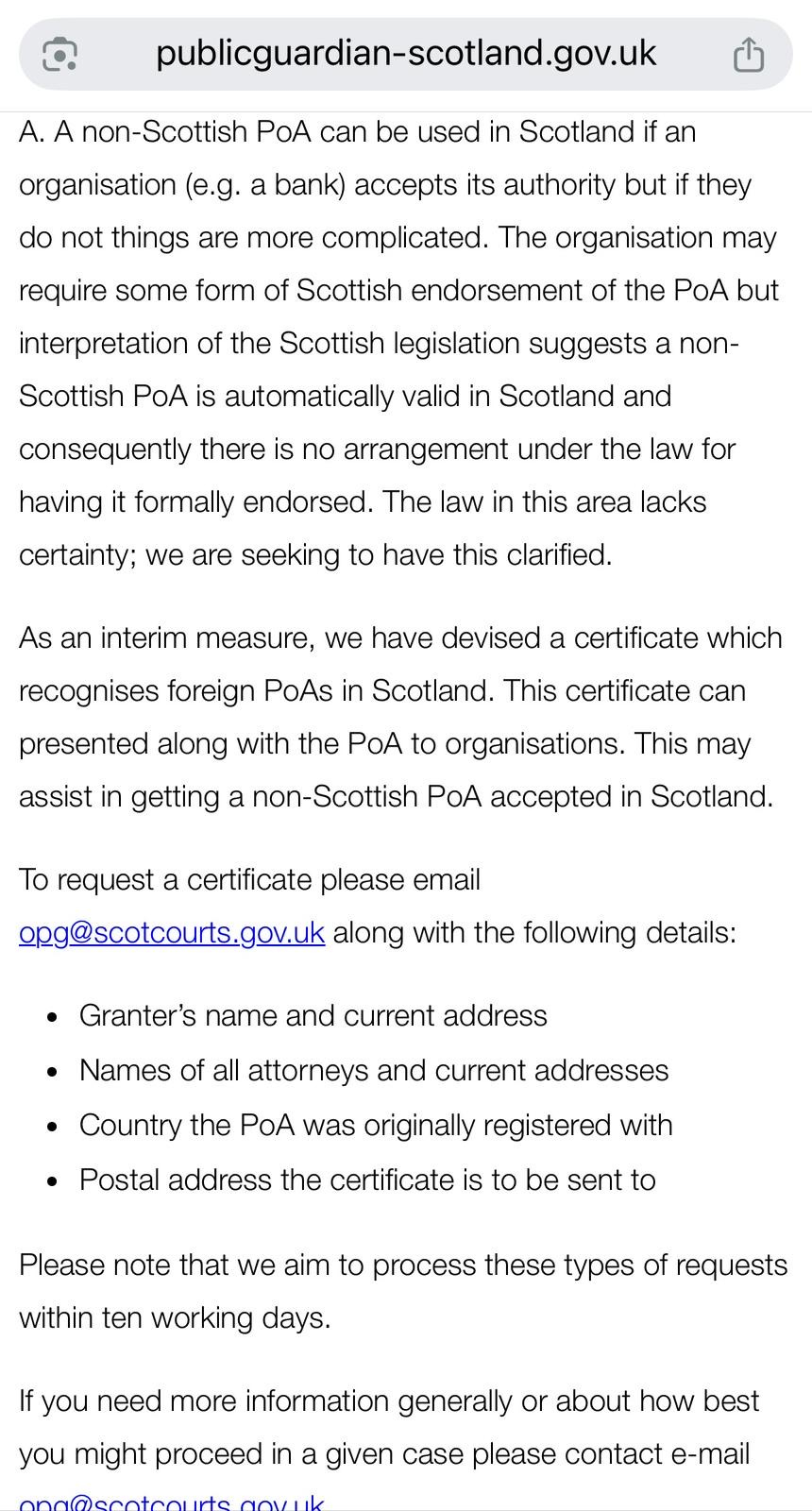

I suspect UK entities might question whether a foreign POA has been validly made in the foreign jurisdiction. Even among the jurisdictions within the UK there are different formalities required for POAs. So may be simpler just to make one in a format they'll recognise.1

-

If the amounts are small and the accounts not too complicated you can usually cover things by making sure there is a clear statement of the beneficiaries for any residual amounts in DC pensions or other death benefits. But it would be best to have a UK POA with someone who is a UK resident to make sure the amounts can be transferred to Canada. It's also best to have the executor of the Canadian will be someone who is in Canada.And so we beat on, boats against the current, borne back ceaselessly into the past.1

-

-

Thanks all. Situation is perhaps slightly more complicated as most of the assets are probably under Scottish law.Bank accounts are relatively small and all joint bar one. Mostly only kept to aid transferring of gifts from relatives at birthdays and Christmas.Both only worked for 8 or 9 years before moving so pension not large either. One is a DC pension and the other DB - local government. Perhaps the DC one may get transferred over to Canada at some point.With regards to the Will, their Canadian lawyer has informed them about the resealing process and just wants to know if they’re happy with that and if their UK assets should be mentioned in their Will or not.With regards to POA, that was mentioned too but although it may seem sensible to allow someone in Scotland to handle it here, it is of course making it more expensive and more involved. I’ve checked with the Public Guardian’s Office and they may just go down this route for now.

ill suggest they have a look on an expat forum too.0 -

From a practical perspective, resealing is discouraged in Scotland. While the legislation which allows resealing (Colonial Probates Act 1892) applies in Scotland, its operation in respect of a foreign domicile is treated as optional and an application may be declined by Edinburgh Sheriff Court in preference to applying for Confirmation for any Scottish estate.With regards to the Will, their Canadian lawyer has informed them about the resealing process and just wants to know if they’re happy with that and if their UK assets should be mentioned in their Will or not.1 -

Just on the will question:

Given my experience of trying to sort this out for a relative who was domociled abroad even when they had done everything they could to simplify matters (including having a sepatrate will covering the UK assets) I would really consider how much you (or rather they) benefit from having any assets held in UK.

It is not just the extra paperwork, it is that the UK systems just simply ignore any cases other than totally simple UK based ones. E.g. I have been waiting for the probate office simply to read my application (not do anything on it!) for nearly 6 months now. It is emotionally very draining.

Assuming it can be done in a realtively cost effective way, I would investigate moving the DC pension to Canada. Same with bank accounts. I don't know if the DB scheme would cease on death (in which case, no impact on will) or would have any benefit post that.

Just possibly worth at least investigating what transfer value you might get (though maybe that is not even an option for local govenrment scheme).

Obvioulsy you would want to weigh up the disadvantage in doing that from a financial point of view but you would really be doing a favour for the executor when the time does come.

Also I should note that I am a) a bit close to this and b) may have been very unlucky with my experience.1 -

Thanks buddy.buddy9 said:

From a practical perspective, resealing is discouraged in Scotland. While the legislation which allows resealing (Colonial Probates Act 1892) applies in Scotland, its operation in respect of a foreign domicile is treated as optional and an application may be declined by Edinburgh Sheriff Court in preference to applying for Confirmation for any Scottish estate.With regards to the Will, their Canadian lawyer has informed them about the resealing process and just wants to know if they’re happy with that and if their UK assets should be mentioned in their Will or not.

Having had to wait 15 weeks recently for Confirmation from Glasgow Sheriff Court for my late father’s estate who was a Scottish resident, nothing surprises me to be honest.So basically both pensions are outwith the Will anyway.

Bank accounts - keep to a minimum.0 -

Yes I think you’re right to be honest.SadCodeMan said:Just on the will question:

Given my experience of trying to sort this out for a relative who was domociled abroad even when they had done everything they could to simplify matters (including having a sepatrate will covering the UK assets) I would really consider how much you (or rather they) benefit from having any assets held in UK.

It is not just the extra paperwork, it is that the UK systems just simply ignore any cases other than totally simple UK based ones. E.g. I have been waiting for the probate office simply to read my application (not do anything on it!) for nearly 6 months now. It is emotionally very draining.

Assuming it can be done in a realtively cost effective way, I would investigate moving the DC pension to Canada. Same with bank accounts. I don't know if the DB scheme would cease on death (in which case, no impact on will) or would have any benefit post that.

Just possibly worth at least investigating what transfer value you might get (though maybe that is not even an option for local govenrment scheme).

Obvioulsy you would want to weigh up the disadvantage in doing that from a financial point of view but you would really be doing a favour for the executor when the time does come.

Also I should note that I am a) a bit close to this and b) may have been very unlucky with my experience.The DB scheme would continue on death if spouse is still alive but otherwise yes it would stop. You can transfer the LGPS pension out as it’s funded but whether it’s sensible at this stage is another matter.0 -

The DB plan might not be an issue for the will, depending on whether or not it has death benefits.And so we beat on, boats against the current, borne back ceaselessly into the past.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards