We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Refused renewal

ripplyuk

Posts: 2,965 Forumite

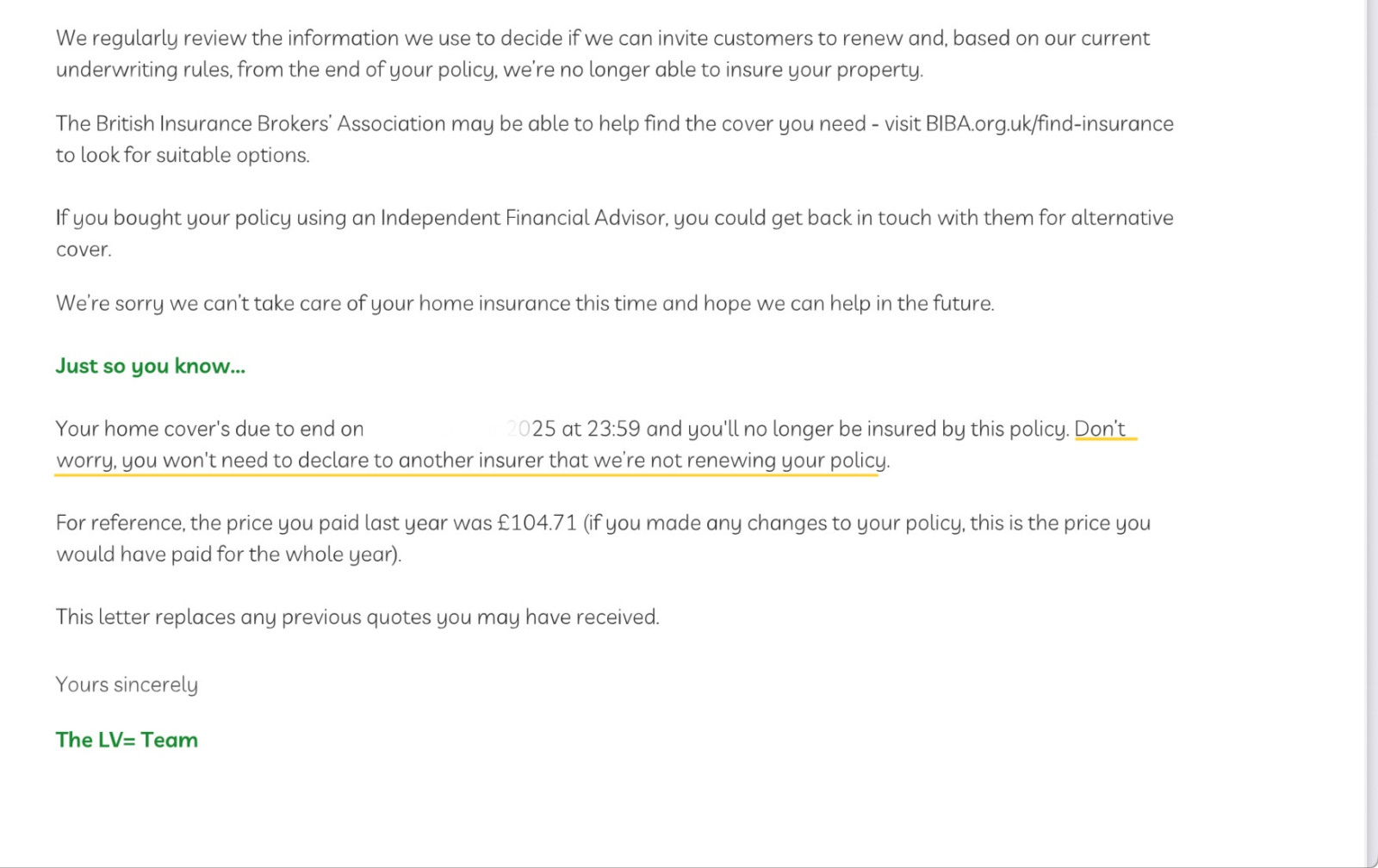

This is home insurance with LV. I’ve been with them for over 10yrs with no changes and have never made a claim on this or any other type of insurance.

They don’t give a reason but I remember some years back, they stopped offering insurance for those with oil heating, which I have. It could be something to do with that. What’s confusing me is that every insurer will ask ‘Have you ever had insurance denied, cancelled or declined on renewal?’, so why are LV stating that I don’t need to declare this?

I’m worried it will not only affect my home insurance but also my car insurance.

0

Comments

-

Hi, they say you do not need to declare because they are not refusing you insurance but rather dont have a policy to offer you. Insurers every so often go through their insurance criteria/ what they are willing to insure and change their policies which can result in people not being offered insurance for whatever reason. This can be postcode, what items, occupation, environment etc - it is they do not have a policy to offer you so it is nothing you have done so you dont have to declare it.4

-

Because the traditional question is limited to you ever having insurance cancelled, voided, declined or special terms applied, for which you won't have to declare this because it's none of those.ripplyuk said:This is home insurance with LV. I’ve been with them for over 10yrs with no changes and have never made a claim on this or any other type of insurance.They don’t give a reason but I remember some years back, they stopped offering insurance for those with oil heating, which I have. It could be something to do with that. What’s confusing me is that every insurer will ask ‘Have you ever had insurance denied, cancelled or declined on renewal?’, so why are LV stating that I don’t need to declare this?I’m worried it will not only affect my home insurance but also my car insurance.

There is an emerging trend however for insurers to now tack on another element which is if an insurer has refused to renew you. On this question you would have to answer "yes" to however.

It ultimately comes down to the exact question asked, the most common non-standard question I've seen asks if someone has refused to renew you, which the OP would have to answer "yes" to even if its not their fault.Auti said:Hi, they say you do not need to declare because they are not refusing you insurance but rather dont have a policy to offer you. Insurers every so often go through their insurance criteria/ what they are willing to insure and change their policies which can result in people not being offered insurance for whatever reason. This can be postcode, what items, occupation, environment etc - it is they do not have a policy to offer you so it is nothing you have done so you dont have to declare it.

1 -

That's a bit worrying. LV didn't refuse to renew my travel insurance recently, but they said they couldn't cover my medical conditions. I took that to be, in essence, the same thing as a refusal. I know it's not, because it sounded like they would have covered all other sections of the policy. This new question of, has someone refused to renew you, could be a concern.MyRealNameToo said:

Because the traditional question is limited to you ever having insurance cancelled, voided, declined or special terms applied, for which you won't have to declare this because it's none of those.ripplyuk said:This is home insurance with LV. I’ve been with them for over 10yrs with no changes and have never made a claim on this or any other type of insurance.They don’t give a reason but I remember some years back, they stopped offering insurance for those with oil heating, which I have. It could be something to do with that. What’s confusing me is that every insurer will ask ‘Have you ever had insurance denied, cancelled or declined on renewal?’, so why are LV stating that I don’t need to declare this?I’m worried it will not only affect my home insurance but also my car insurance.

There is an emerging trend however for insurers to now tack on another element which is if an insurer has refused to renew you. On this question you would have to answer "yes" to however.

It ultimately comes down to the exact question asked, the most common non-standard question I've seen asks if someone has refused to renew you, which the OP would have to answer "yes" to even if its not their fault.Auti said:Hi, they say you do not need to declare because they are not refusing you insurance but rather dont have a policy to offer you. Insurers every so often go through their insurance criteria/ what they are willing to insure and change their policies which can result in people not being offered insurance for whatever reason. This can be postcode, what items, occupation, environment etc - it is they do not have a policy to offer you so it is nothing you have done so you dont have to declare it.0 -

There are many occasions where it's a consumer choice to end the policy/not take up a renewal and those dont have to be declared. If you phone up and say your planning on moving home but the insurer won't cover your proposed new address its really you cancelling the policy as in principle you had the option to not move and thus keep the policy going. By the sounds of it you could have renewed but chose not to because you could get better coverage elsewhere.luci said:

That's a bit worrying. LV didn't refuse to renew my travel insurance recently, but they said they couldn't cover my medical conditions. I took that to be, in essence, the same thing as a refusal. I know it's not, because it sounded like they would have covered all other sections of the policy. This new question of, has someone refused to renew you, could be a concern.MyRealNameToo said:

Because the traditional question is limited to you ever having insurance cancelled, voided, declined or special terms applied, for which you won't have to declare this because it's none of those.ripplyuk said:This is home insurance with LV. I’ve been with them for over 10yrs with no changes and have never made a claim on this or any other type of insurance.They don’t give a reason but I remember some years back, they stopped offering insurance for those with oil heating, which I have. It could be something to do with that. What’s confusing me is that every insurer will ask ‘Have you ever had insurance denied, cancelled or declined on renewal?’, so why are LV stating that I don’t need to declare this?I’m worried it will not only affect my home insurance but also my car insurance.

There is an emerging trend however for insurers to now tack on another element which is if an insurer has refused to renew you. On this question you would have to answer "yes" to however.

It ultimately comes down to the exact question asked, the most common non-standard question I've seen asks if someone has refused to renew you, which the OP would have to answer "yes" to even if its not their fault.Auti said:Hi, they say you do not need to declare because they are not refusing you insurance but rather dont have a policy to offer you. Insurers every so often go through their insurance criteria/ what they are willing to insure and change their policies which can result in people not being offered insurance for whatever reason. This can be postcode, what items, occupation, environment etc - it is they do not have a policy to offer you so it is nothing you have done so you dont have to declare it.

The OP is different, they've changed nothing but for some reason the insurer has refused to renew them. Fine under the old question, a problem under the new question. I dont see most insurers using the new style question but of cause the aggregators have to deal with the lowest requirements of their medium/large panel members so if just one of them wants it asked they are likely to add it so it appears more wide spread. In principle it could have follow on questions and the other panel insurers update their integration to factor in the lower questions but these things cost money and sometimes they arent considered the highest priority for IT investment.1 -

Yes, I could have renewed, but a policy that doesn't cover major medical conditions is not worth the paper it's written on.MyRealNameToo said:

There are many occasions where it's a consumer choice to end the policy/not take up a renewal and those dont have to be declared. If you phone up and say your planning on moving home but the insurer won't cover your proposed new address its really you cancelling the policy as in principle you had the option to not move and thus keep the policy going. By the sounds of it you could have renewed but chose not to because you could get better coverage elsewhere.luci said:

That's a bit worrying. LV didn't refuse to renew my travel insurance recently, but they said they couldn't cover my medical conditions. I took that to be, in essence, the same thing as a refusal. I know it's not, because it sounded like they would have covered all other sections of the policy. This new question of, has someone refused to renew you, could be a concern.MyRealNameToo said:

Because the traditional question is limited to you ever having insurance cancelled, voided, declined or special terms applied, for which you won't have to declare this because it's none of those.ripplyuk said:This is home insurance with LV. I’ve been with them for over 10yrs with no changes and have never made a claim on this or any other type of insurance.They don’t give a reason but I remember some years back, they stopped offering insurance for those with oil heating, which I have. It could be something to do with that. What’s confusing me is that every insurer will ask ‘Have you ever had insurance denied, cancelled or declined on renewal?’, so why are LV stating that I don’t need to declare this?I’m worried it will not only affect my home insurance but also my car insurance.

There is an emerging trend however for insurers to now tack on another element which is if an insurer has refused to renew you. On this question you would have to answer "yes" to however.

It ultimately comes down to the exact question asked, the most common non-standard question I've seen asks if someone has refused to renew you, which the OP would have to answer "yes" to even if its not their fault.Auti said:Hi, they say you do not need to declare because they are not refusing you insurance but rather dont have a policy to offer you. Insurers every so often go through their insurance criteria/ what they are willing to insure and change their policies which can result in people not being offered insurance for whatever reason. This can be postcode, what items, occupation, environment etc - it is they do not have a policy to offer you so it is nothing you have done so you dont have to declare it.

The OP is different, they've changed nothing but for some reason the insurer has refused to renew them. Fine under the old question, a problem under the new question. I dont see most insurers using the new style question but of cause the aggregators have to deal with the lowest requirements of their medium/large panel members so if just one of them wants it asked they are likely to add it so it appears more wide spread. In principle it could have follow on questions and the other panel insurers update their integration to factor in the lower questions but these things cost money and sometimes they arent considered the highest priority for IT investment.

Sorry, I didn't mean to derail the discussion. I was just interested in this new question that may be asked0 -

@MyRealNameToo So LV are wrong in saying I don’t have to declare it? They don’t specify what questions I’d be answering; it’s just a blanket statement that I don’t need to declare it.0

-

Until @MyRealNameToo comes back to you.ripplyuk said:@MyRealNameToo So LV are wrong in saying I don’t have to declare it? They don’t specify what questions I’d be answering; it’s just a blanket statement that I don’t need to declare it.

My understanding is this. It will be up to any future provider to decide whether you need to declare it or not, nothing to do with LV. You only need to answer the specific question that's being asked. If they ask if you've had insurance cancelled, declined or voided by the insurer (not by you), you can answer honestly, no. If they ask if any insurer has declined to quote, then you will have to say yes.1 -

ripplyuk said:@MyRealNameToo So LV are wrong in saying I don’t have to declare it? They don’t specify what questions I’d be answering; it’s just a blanket statement that I don’t need to declare it.

They can tell you how you can answer the typical question, which I agree would be a no.

They can also tell you what they will be loading to CUE which is how most insurers would catch you out if you lied.

They have no authority to tell you how to answer absolutely any question any future insurer may choose to ask.

I mean you could take a punt and answer no because they said you could, you could raise a complaint to them in the future if this is found out to be incorrect. The chances of it being found out are small if they arent loading it to CUE however a good proportion of cases are found out because customers tell insurers at a later date in claims and then you have a large argument to be having if that insurer agrees with me that the answer "no" was incorrect and therefore the policy is void.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards