We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

How to read a Gilt for a pension gilt ladder?

MetaPhysical

Posts: 576 Forumite

Looking at the Gilt example above on Interactive Investor, please sanity check my understanding.

So I'd buy the £100 Gilt for £96.60 if I were to buy it today and I'd get back £100 upon maturity making me £3.40 profit which would be free from CGT (good to hold in a GIA). 3.40/96.60 = 3.52%

I'd also get a 37.5p coupon in December and another one in June (?) - so another 75p (taxable).

Therefore I made - before tax - 3.40 + 37.5p +37.5p = 4.15 4.15/96.60. = 4.3%

So is the Yield To maturity 4.3% or is it 3.52% please?

When you spit this out on a tax return, how is this reported? Presumably the CGT can be ignored because it's a gilt and the coupon is interest (20/40/45%) or a dividend? And presumably the coupon profit is reported every year but the CGT - if it is reportable - upon maturity?

Many thanks in advance.

0

Comments

-

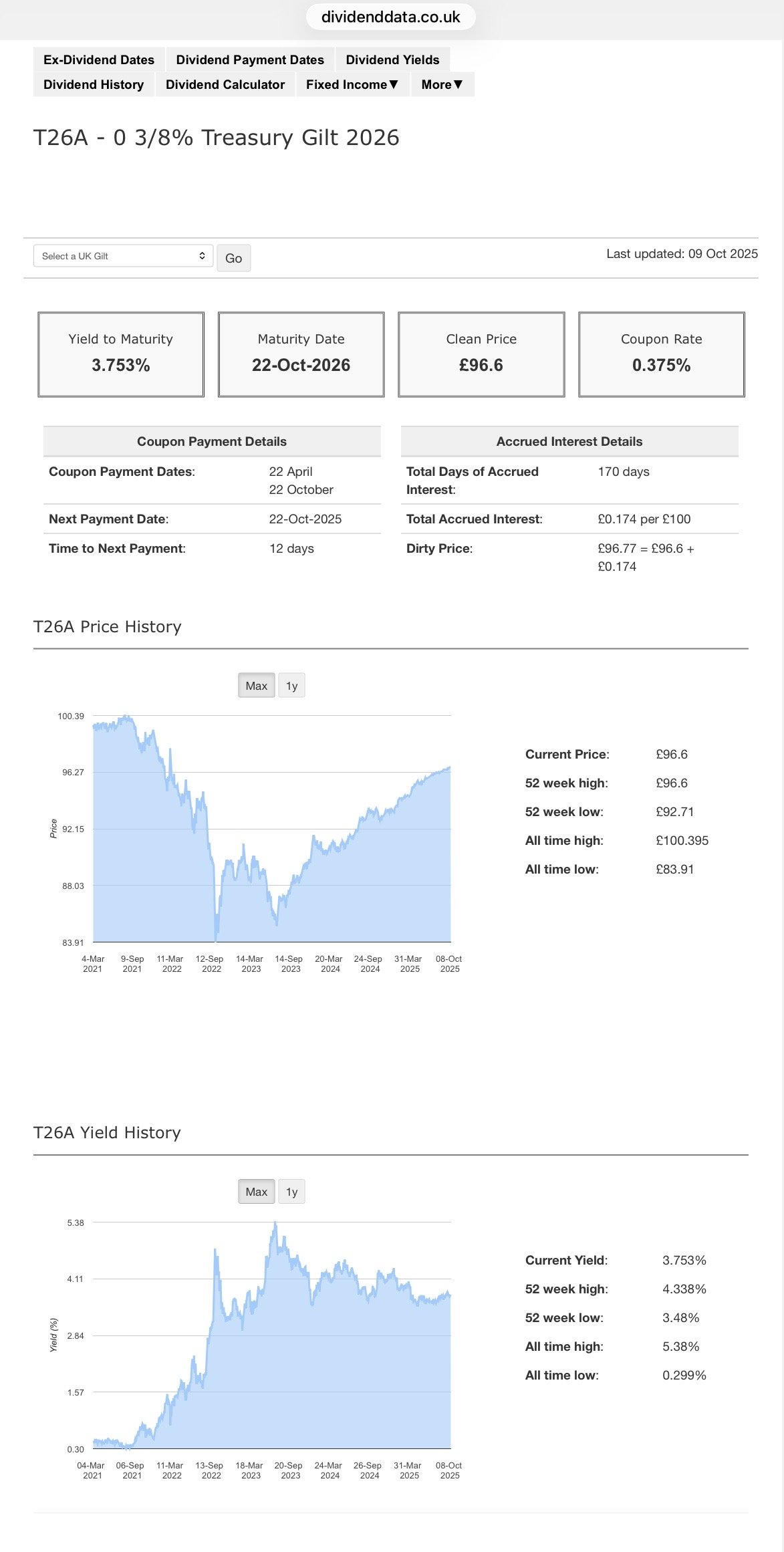

Dividend data gives these figures if it helps.MetaPhysical said:

Looking at the Gilt example above on Interactive Investor, please sanity check my understanding.

So I'd buy the £100 Gilt for £96.60 if I were to buy it today and I'd get back £100 upon maturity making me £3.40 profit which would be free from CGT (good to hold in a GIA). 3.40/96.60 = 3.52%

I'd also get a 37.5p coupon in December and another one in June (?) - so another 75p (taxable).

Therefore I made - before tax - 3.40 + 37.5p +37.5p = 4.15 4.15/96.60. = 4.3%

So is the Yield To maturity 4.3% or is it 3.52% please?

When you spit this out on a tax return, how is this reported? Presumably the CGT can be ignored because it's a gilt and the coupon is interest (20/40/45%) or a dividend? And presumably the coupon profit is reported every year but the CGT - if it is reportable - upon maturity?

Many thanks in advance.

Note that 96.60 is the clean price, you buy (and sell) at the dirty price which reflects accrued interest.

1 -

The 0.375% coupon is per annum so I think you have one too many 37.5p in your sums.1

-

Oh and don't forget that you can deduct the accrued income (0.174 in @FIREDreamer's post) from the coupon received when you do your tax return.1

-

Doh of course! Yes indeed. However, I then make the YtM 3.9%:DRS1 said:The 0.375% coupon is per annum so I think you have one too many 37.5p in your sums.

3.40 + 0.375 / 96.60 = 0.03907. ??? I'm clearly not following something.

DRS1 said:

Really? Any more information on that please and why?Oh and don't forget that you can deduct the accrued income (0.174 in @FIREDreamer's post) from the coupon received when you do your tax return.

Many thanks.0 -

Not sure about the yield. The page I look at shows 3.754% but then it also shows the accrued interest as -0.009 so I think the ex div date (if gilts have such a thing) has passed.MetaPhysical said:

Doh of course! Yes indeed. However, I then make the YtM 3.9%:DRS1 said:The 0.375% coupon is per annum so I think you have one too many 37.5p in your sums.

3.40 + 0.375 / 96.60 = 0.03907. ??? I'm clearly not following something.

DRS1 said:

Really? Any more information on that please and why?Oh and don't forget that you can deduct the accrued income (0.174 in @FIREDreamer's post) from the coupon received when you do your tax return.

Many thanks.

Gilts in Issue - giltsyield.com

On the second point it is just applying the accrued interest scheme. See below

HS343 Accrued Income Scheme (2025) - GOV.UK1 -

Many thanks @DRS1. I'll have a read of that.0

-

I note from one of the other threads that you're not yet retired but planning to be next year. Is there a reason why you are looking at holding Gilts outside a SIPP? Not meaning to be nosey!MetaPhysical said:

Looking at the Gilt example above on Interactive Investor, please sanity check my understanding.

So I'd buy the £100 Gilt for £96.60 if I were to buy it today and I'd get back £100 upon maturity making me £3.40 profit which would be free from CGT (good to hold in a GIA). 3.40/96.60 = 3.52%

I'd also get a 37.5p coupon in December and another one in June (?) - so another 75p (taxable).

Therefore I made - before tax - 3.40 + 37.5p +37.5p = 4.15 4.15/96.60. = 4.3%

So is the Yield To maturity 4.3% or is it 3.52% please?

When you spit this out on a tax return, how is this reported? Presumably the CGT can be ignored because it's a gilt and the coupon is interest (20/40/45%) or a dividend? And presumably the coupon profit is reported every year but the CGT - if it is reportable - upon maturity?

Many thanks in advance.") We are planning on retiring next year as well and I'm considering moving a portion of my pot to Gilts to provide a guaranteed income stream, but we also have a recent inheritance meaning quite a bit of cash floating about which for now is in high interest savings accounts. We will be maxing out our Stocks&Shares ISA allowances next tax year but then still have a fair bit on money knocking around which I haven't yet decided what to do with.0

We are planning on retiring next year as well and I'm considering moving a portion of my pot to Gilts to provide a guaranteed income stream, but we also have a recent inheritance meaning quite a bit of cash floating about which for now is in high interest savings accounts. We will be maxing out our Stocks&Shares ISA allowances next tax year but then still have a fair bit on money knocking around which I haven't yet decided what to do with.0 -

MetaPhysical said:I'm clearly not following something.T26A pays coupons in October and April, not December and June.Note it pays the final coupon on redemption on 22/10/26.The ex-div date for the October 2025 coupon is tomorrow so it is too late to purchase the gilt and receive this coupon.Thus you would receive two coupons between now and redemption, plus the capital gain.Thus the YTM, assuming cash flows on 13/10/25 (purchase at dirty price on giltsyield.com), 22/4/26 (coupon), 22/10/26 (coupon and redemption) is 3.75%.Note that the YTM assumes coupons are reinvested at the same rate as the YTM.Your own calculation is trying to do something different -- you are calculating the total income and gains as a percentage of your purchase price.1

-

You’re not being nosey at all and it’s a good question. Because I have used all my ISA allowance and need to load some money in a GIA. Looking for a tax efficient way of doing so. Just chucking it all in a MM fund at 40% tax doesn’t keep pace with inflation and now is not the time for more equities for me. Low coupon gilts with their CGT exempt status offers some useful options.GenX0212 said:

I note from one of the other threads that you're not yet retired but planning to be next year. Is there a reason why you are looking at holding Gilts outside a SIPP? Not meaning to be nosey!MetaPhysical said:

Looking at the Gilt example above on Interactive Investor, please sanity check my understanding.

So I'd buy the £100 Gilt for £96.60 if I were to buy it today and I'd get back £100 upon maturity making me £3.40 profit which would be free from CGT (good to hold in a GIA). 3.40/96.60 = 3.52%

I'd also get a 37.5p coupon in December and another one in June (?) - so another 75p (taxable).

Therefore I made - before tax - 3.40 + 37.5p +37.5p = 4.15 4.15/96.60. = 4.3%

So is the Yield To maturity 4.3% or is it 3.52% please?

When you spit this out on a tax return, how is this reported? Presumably the CGT can be ignored because it's a gilt and the coupon is interest (20/40/45%) or a dividend? And presumably the coupon profit is reported every year but the CGT - if it is reportable - upon maturity?

Many thanks in advance.We are planning on retiring next year as well and I'm considering moving a portion of my pot to Gilts to provide a guaranteed income stream, but we also have a recent inheritance meaning quite a bit of cash floating about which for now is in high interest savings accounts. We will be maxing out our Stocks&Shares ISA allowances next tax year but then still have a fair bit on money knocking around which I haven't yet decided what to do with.

2 -

...I'm also planning what to do with my TFC as well. Some of it will have to exist in a GIA until I can squirrel it away into ISAs. I follow all the will she/won't she about the TFC possible reduction but I am a "bird in the hand" kind of person who likes to take matters into my own hands; if I am wrong of my own accord then I am happy to live with the consequences but I do not want others making decisions for me that I possibly circumvent. I do not trust this government, they are not on the side of achievers, those who worked hard and those who tried their best and have provided for themselves, and I am taking a big chunk of my TFC out now, though not all of it. Even if she doesn't do it this year, there are three more years where she could. I've had enough of this speculation every year, and there could even be a percentage tax on what's in your pot - dystopian to say the least - and I am taking it now.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards