We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

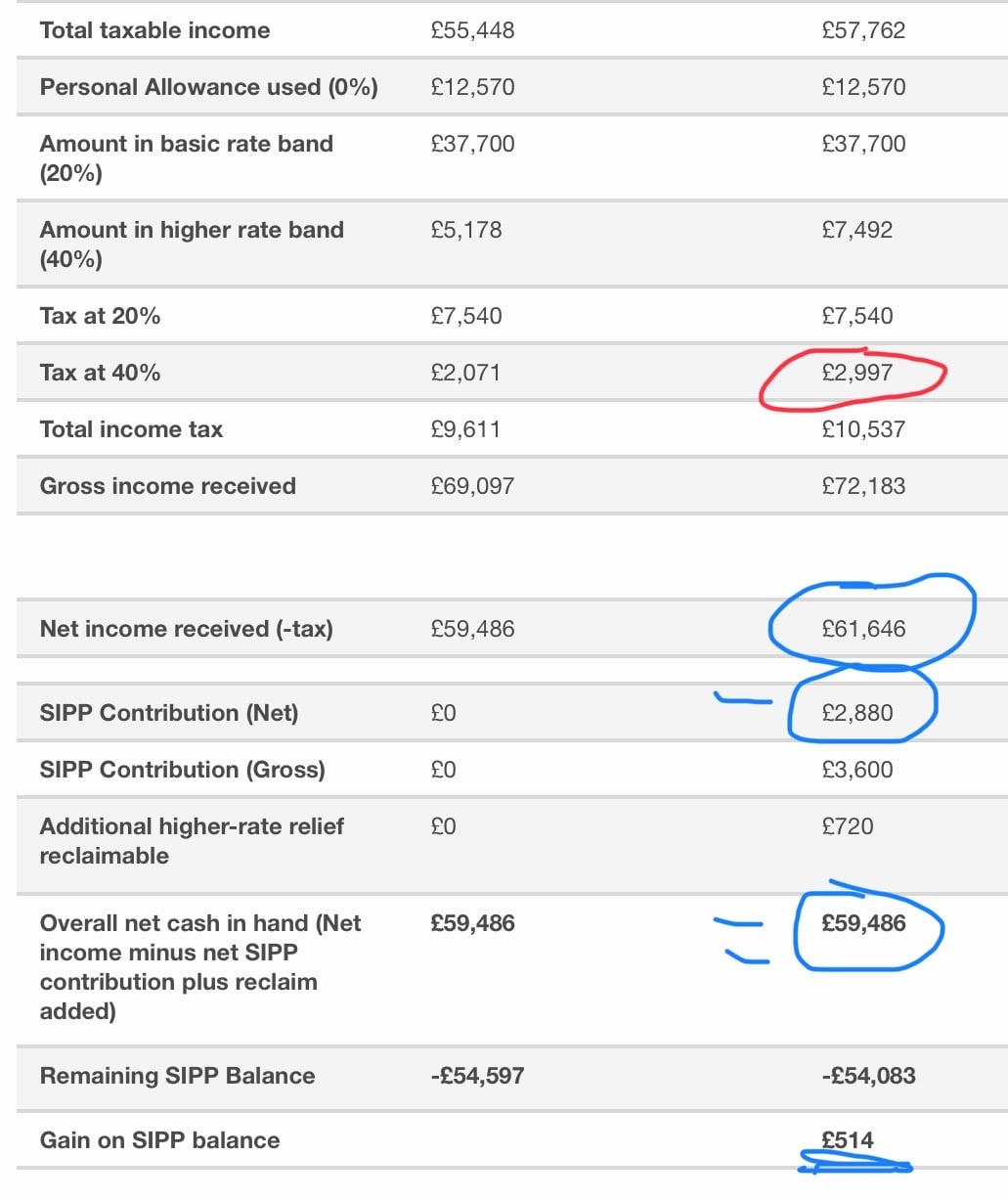

£2880 pay from drawdown

Comments

-

Easy Peasy. You have indeed ended up with the same cash in hand, but £514 more in your SIPP. To actually take that OUT of the SIPP though so you can spend it, you will have to pay 40% tax on three quarters of it. Which will leave you with the £360 that Molerat said.

Of course, if you are going to hit the lifetime limit for TFLS you make no profit whatsoever - which is why I don't do it.

4 -

but haven't I already accounted for the 40% tax that I needed to pay in order to take out the £2880 net and recycle it back in the first place? I can just keep doing this each year and the SIPP balance grows £514 each time, the cash I have left to spend £59,486 is the same as if I do nothing, am I missing something?

Absolutely fair point re the LSA

0

0 -

Mole rats original post was putting 2880 in snd taking it out again all at the 40% tax bracket.

You have only added 2880 at the 40% tax bracket. You haven’t taken the gain out. As pointed out if you take this 514 out at the 40% tax bracket you will get 360 same as molerat.

Now the real trick is to contribute at 40% tax rate then take it out at 20% or less later.

1 -

If you've hit the LSA, you can squeeze out a bit more tax free cash by using the 'small pots regime'. 25% of each pot is tax free and counts for 0% of the LSA.

If you've not already done so, you can do it 3 times with personal pensions, and an unlimited number of times from true occupational schemes. Most people will only be able to avail themselves of the personal pension route, but that's up to 3 pots of no more than £10K each, so a possible further £7,500 of tax free cash. Set up a SIPP with a provider who'll carve out small pots for you - I gather from other posters on this forum that HL will.

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

I finally figured out why you were taking £3086 more out, I thought that's a very odd number.

However, removing that amount from a pension at 25% tax free and then taxed at 40% gives you £2160. Which is exactly £720 below the £2880. So what you are doing is removing the minimum extra you can from the pension to feed back in £2880 (2160 + 720 higher rate tax relief) which becomes £3600 in pension, which is a gain of £514 over the original £3086. However if you then take his £514 out it becomes £360 which matches the gain that molerat calculated.

0 -

I'm hoping to try this HL small pots rule in three years time. I did a partial transfer out at 55 to minimise LTA charges (a blast from the past!). I didn't have enough to take the full tax free limit, so left enough behind to take the last £26k of tax free cash leveraging the old DB section. Those funds have grown, so I should now have enough left over to transfer to HL. I still find it hard to believe it will really work, but it will be a nice little bonus :)

0 -

it certainly works now. I have done the 3 small pots via HL in the last couple of months as I could get everything done at 20% tax

I’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.0 -

Yep, I've definitely gone the long way around to arrive at the same answer 😂

As you have correctly deduced from my ramblings I was trying to work out how much more I needed to take from the SIPP in order to recycle £2800 Net (£3600 Gross) back into the SIPP and still achieve the exact same cash in hand (after paying 40% tax and reclaiming higher rate tax relief on the £3600) and the answer left me with £514 more in the SIPP each year.

Your right, the key is when all of those £514 gains are taken out and at what tax rate, plus remembering to reclaim from HMRC each year, plus keeping an eye on the LSA.Repeat this for 10 years and with a decent growth rate and you could have an extra £6-8k of free money in your SIPP. Even if you do end up having already used up your LSA and paying 40% tax on your withdrawal then you're still up.

IF you are already going to be paying 40% on your withdrawals then apart from the admin hassle I'm not sure I'm seeing a downside on this.0 -

If you end up breaching the LSA you would have done better to withdraw it ASAP before it grew. £360 growing in an ISA is better than £514 in a pension with the tax rate steadily increasing as the LSA covers a smaller portion of it.

Better to withdraw TFLS immediately and stop contributing once you've used up LSA and small pot limits.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards