We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Considering an annuity with another provider. Is an IFA really needed to do this?

Comments

-

IFAs or website distribution will use the real-time pricing tools for the whole of market.grn99 said:

Thanks. I assume the whole of market prices only available to IFA’s??dunstonh said:Their quote also says they are the best one.Ignore that. It's broken. It uses the MoneyHelper tables. You often see that on quotes that are not the best.

You need to see the whole of market prices to see for yourself.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

Hargreaves Lansdown can provide annuity quotes - with health issues allowed for.grn99 said:

Thanks. I assume the whole of market prices only available to IFA’s??dunstonh said:Their quote also says they are the best one.Ignore that. It's broken. It uses the MoneyHelper tables. You often see that on quotes that are not the best.

You need to see the whole of market prices to see for yourself.

EDIT: All the main providers are there I believe.0 -

Thanks. Too late now. I accepted the quote (and to be fair it was higher than I expected)dunstonh said:Their quote also says they are the best one.Ignore that. It's broken. It uses the MoneyHelper tables. You often see that on quotes that are not the best.

You need to see the whole of market prices to see for yourself.0 -

yes, and I have found them cheaper than IFA route for both large and small annuities. Having said that, I went for IFA each time as I wanted some advice and considered the post commission price difference worthwhile "payment" for the advice received.Hargreaves Lansdown can provide annuity quotes - with health issues allowed for.

EDIT: All the main providers are there I believe.1 -

Have confirmed his morning direct with SLAC that they won't deal with new customer direct, only to an IFA. SW did of course talk to me and the numbers were actually better than the HL or Money Helper quotes (which I don't profess to understand).0

-

There are three quote levels. Snapshot on a given date using remuneration assumptions (moneyhelper). Online quote engines (3 main ones available to IFAs and other distribution arms) and manual underwritten quotes.grn99 said:Have confirmed his morning direct with SLAC that they won't deal with new customer direct, only to an IFA. SW did of course talk to me and the numbers were actually better than the HL or Money Helper quotes (which I don't profess to understand).

Manual quotes often come in best for those with more significant health conditions, as it's passed to a doctor to look at rather than the computer. Typically, you need an IFA to go down that route as it's a manual process and the website quote services tend to stick to what you input and what the online quote says.

There is actually a fourth method, which only applies to a couple of providers who offer quotes based on current gilt yields in real time and a sales team with the ability to lock in a rate higher than their online rate, if the live rate is better than the official rate.

This is part of the reason the "best quote" is often incorrect, as it relies on snapshot data and assumptions about commercial terms.

SW tend to have low uplifts on many health conditions quote better on clean health. So, this often sees them come in higher up the pricing table when health is less of an issue but lower down when health is an issue.

Indeed, I did a quote last week, and SW were second from the bottom. They gave no uplift. SL was best last week by some way but a refresh now shows SL and Just were the top two, with just a few pounds in it on the computer quote, but SL was better with a manual underwriting quote (which the refresh still didnt beat). Based on that refresh, I am just waiting for Just to come back to see if they will beat the manual underwritten quote from SL.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

When I looked at annuity quotes in 2023 and 2025 I used two quote emails to see the difference. One was for all my proper health details and one with no details completed.dunstonh said:

There are three quote levels. Snapshot on a given date using remuneration assumptions (moneyhelper). Online quote engines (3 main ones available to IFAs and other distribution arms) and manual underwritten quotes.grn99 said:Have confirmed his morning direct with SLAC that they won't deal with new customer direct, only to an IFA. SW did of course talk to me and the numbers were actually better than the HL or Money Helper quotes (which I don't profess to understand).

Manual quotes often come in best for those with more significant health conditions, as it's passed to a doctor to look at rather than the computer. Typically, you need an IFA to go down that route as it's a manual process and the website quote services tend to stick to what you input and what the online quote says.

There is actually a fourth method, which only applies to a couple of providers who offer quotes based on current gilt yields in real time and a sales team with the ability to lock in a rate higher than their online rate, if the live rate is better than the official rate.

This is part of the reason the "best quote" is often incorrect, as it relies on snapshot data and assumptions about commercial terms.

SW tend to have low uplifts on many health conditions quote better on clean health. So, this often sees them come in higher up the pricing table when health is less of an issue but lower down when health is an issue.

Indeed, I did a quote last week, and SW were second from the bottom. They gave no uplift. SL was best last week by some way but a refresh now shows SL and Just were the top two, with just a few pounds in it on the computer quote, but SL was better with a manual underwriting quote (which the refresh still didnt beat). Based on that refresh, I am just waiting for Just to come back to see if they will beat the manual underwritten quote from SL.

All providers were higher with the health details (some by over 10%) except for Just where health details made no difference whatsoever in the annuity quotes on both occasions.

Regardless, Just were the best quote by a long way and so I took their quotes on both occasions.

Maybe a coincidence, but medical details seem to have no impact on the rates offered by Just.

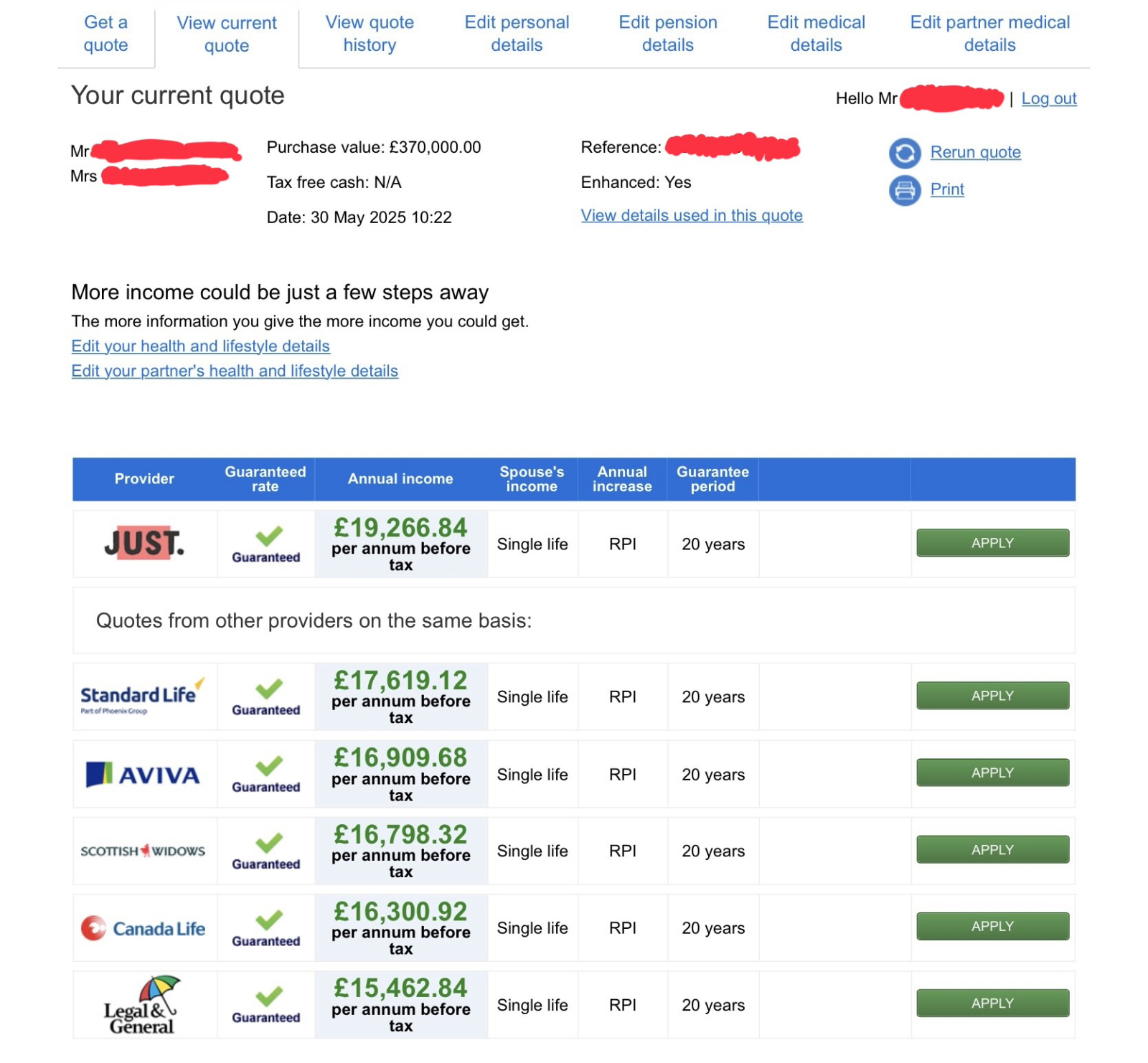

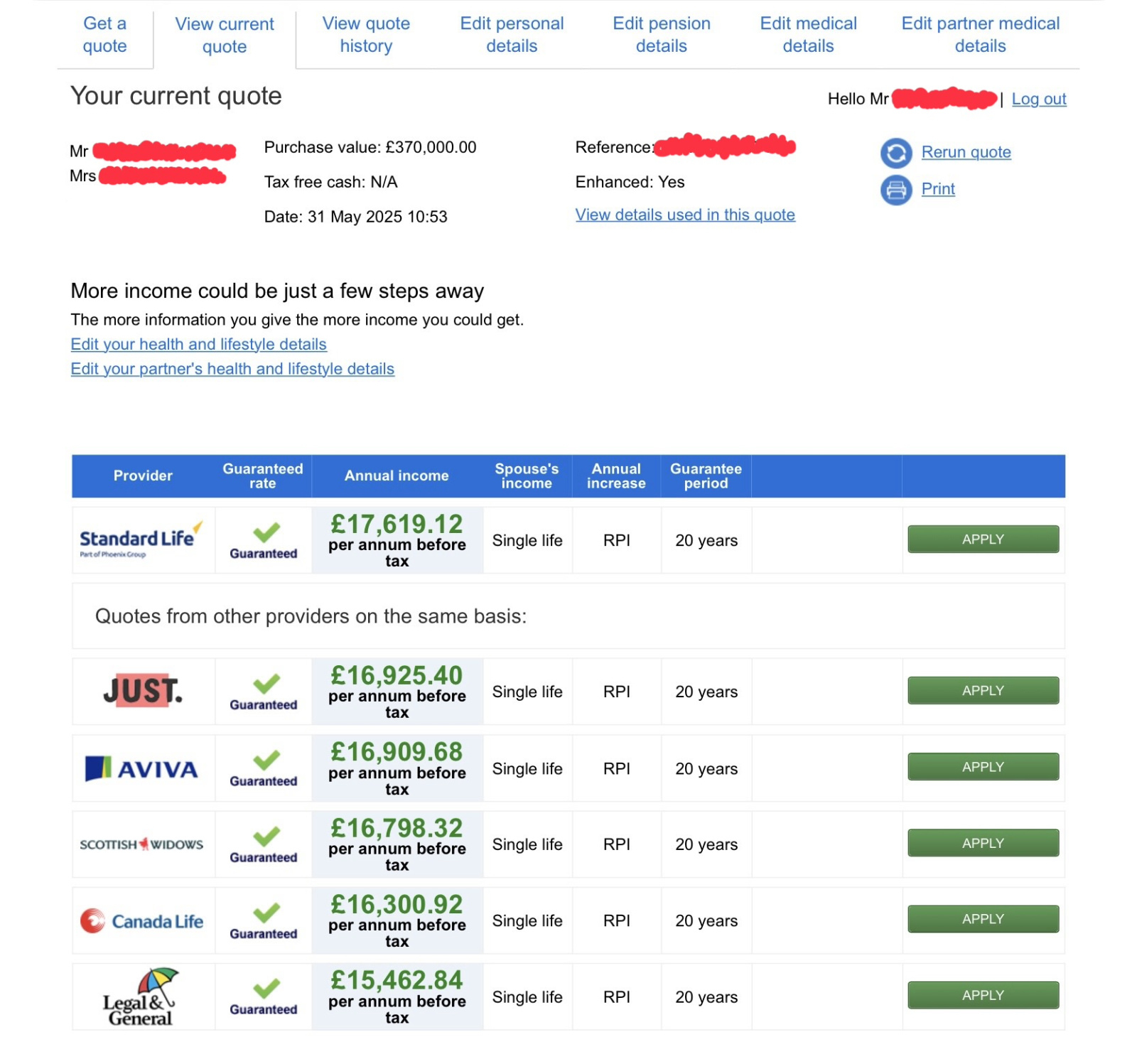

The day after I ran the Just quote on 30 May, their rates dropped by 12% the next day with Standard Life being the best quote by 5% (but still 10% less than the previous day’s quote by Just).

Hargreaves Lansdown got me the May 30 quote from Just. In fact I got £100 a year more than that quote for some reason. As I already had a Just annuity, perhaps they rebated a monthly policy fee of about £8 from this new annuity?

I went for single life with a 20 year guarantee having previously had a joint life for my last annuity.

I am 61 years old.

30 May quotes 31 May quotes

31 May quotes 0

0 -

Thanks for that insight, very interesting.dunstonh said:

There are three quote levels. Snapshot on a given date using remuneration assumptions (moneyhelper). Online quote engines (3 main ones available to IFAs and other distribution arms) and manual underwritten quotes.grn99 said:Have confirmed his morning direct with SLAC that they won't deal with new customer direct, only to an IFA. SW did of course talk to me and the numbers were actually better than the HL or Money Helper quotes (which I don't profess to understand).

Manual quotes often come in best for those with more significant health conditions, as it's passed to a doctor to look at rather than the computer. Typically, you need an IFA to go down that route as it's a manual process and the website quote services tend to stick to what you input and what the online quote says.

There is actually a fourth method, which only applies to a couple of providers who offer quotes based on current gilt yields in real time and a sales team with the ability to lock in a rate higher than their online rate, if the live rate is better than the official rate.

This is part of the reason the "best quote" is often incorrect, as it relies on snapshot data and assumptions about commercial terms.

SW tend to have low uplifts on many health conditions quote better on clean health. So, this often sees them come in higher up the pricing table when health is less of an issue but lower down when health is an issue.

Indeed, I did a quote last week, and SW were second from the bottom. They gave no uplift. SL was best last week by some way but a refresh now shows SL and Just were the top two, with just a few pounds in it on the computer quote, but SL was better with a manual underwriting quote (which the refresh still didnt beat). Based on that refresh, I am just waiting for Just to come back to see if they will beat the manual underwritten quote from SL.0 -

All providers were higher with the health details (some by over 10%) except for Just where health details made no difference whatsoever in the annuity quotes on both occasions.On the quotes we see as IFAs, it gives us the level of uplift from their standard price.

When you start getting to 20+ years guaranteed period, the level of uplift will start to drop away. Some being small. Some being non-existent. It depends on what they think your life expectency is based on the medical conditions.Maybe a coincidence, but medical details seem to have no impact on the rates offered by Just.They do. That one I mentioned previously had a 2.02% uplift by Just. (with two providers being no uplift and the best having a 3.72% uplift, despite being third in pricing).

It can all be down to timing and demand. Somtimes, when a provider shoves its base annuity rate higher, it will lower the uplift for medical conditions. Other times it will lower its base annuity rate but increase the uplift. Sometimes, they will increase the base annuity rate but still leave medical uplifts applying to a lower base rate where you get the higher of the uplifted rate or the upper annuity rate.The day after I ran the Just quote on 30 May, their rates dropped by 12% the next day with Standard Life being the best quote by 5% (but still 10% less than the previous day’s quote by Just).May 2025 was a bit of a !!!!!! with Just. Although it wasn't their fault, it was the markets. Gilt yields were volatile, and Just's daily pricing and real-time pricing reflected the volatility. The others were smoothing it out but Just were following the volatility. If you got your timing right, you did very well out of it.

I remember doing a quote on a Friday and redoing it on the application on Monday to see if there was any improvement, and it had dropped away by around 10%. It was one of the largest swings I have ever seen. Thankfully, the Friday price was guaranteed and we used that one (which is normal with quotes and not specific to any distribution channel unless you are only obtaining quick quotes).

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

I've been exploring annuities using the Hargreaves Lansdown annuity quotation tool. On transferring around £150,000 from my SIPP into an annuity it would see HL be paid a £4,800 commission. Ouch! If I go down the annuity route I'll certainly be looking for a cost-effective way to purchase it. £4,800!!!! What?!?!?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards