We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Has UC removed my NI credits a year into my pension?

Comments

-

No point sending signed for as it won't be, just a waste of money. Letters are often taking many months to actually be opened and scanned into the system, it is the worst possible way to communicate with HMRC.As a post 2016 retiree with no full years recorded she should have no entitlement, there are various ways a full year could be achieved with no inference of how it got there but to get any pension you need full years. Part years do not aggregate to make full years. A weird one !0

-

People who know more than me will be along shortly but are you sure she has no full years? Have you gone back all the way to her 16th birthday? You get full years for just being at school so she should have some back then.0

-

That’s what I imagined would be the case…no full years, no pension. And this is where my confusion begins - the value of “full years”. Everyone tells me not to bother with the actual number of years involved in my pension calculation, even though counting years got me to within a whisker of the full pension; and now we have a NI record that shows no full years but qualifies for a pension.

My own NI record took me back to to schooldays, 1975; hers begins in 1989 (age 22) but she was variously at college, on YTS, temp jobs, travelling from 16yo. From ‘89 onwards, she has NI credits varying between 20&35 weeks for a few years, as well as 10 missing years, plus ages 16-22. 1998-2002 isn’t showing but I met her in that time, while she was temping with my employer. 2004-2007 is also missing.

1 -

Maybe you could post some screenshots so we know what you mean by "missing".0

-

OK, hands up. Mea culpa etc.

Of course, for my other half’s NI record, I was looking at “gaps in my record and the costs of filling them”, NOT the full record. The missing ones were the full years and go right back to 1982. She has 19 full years at present.No wonder you had a raised eyebrow. Sorry for wasting your time with a stinky red herring.1 -

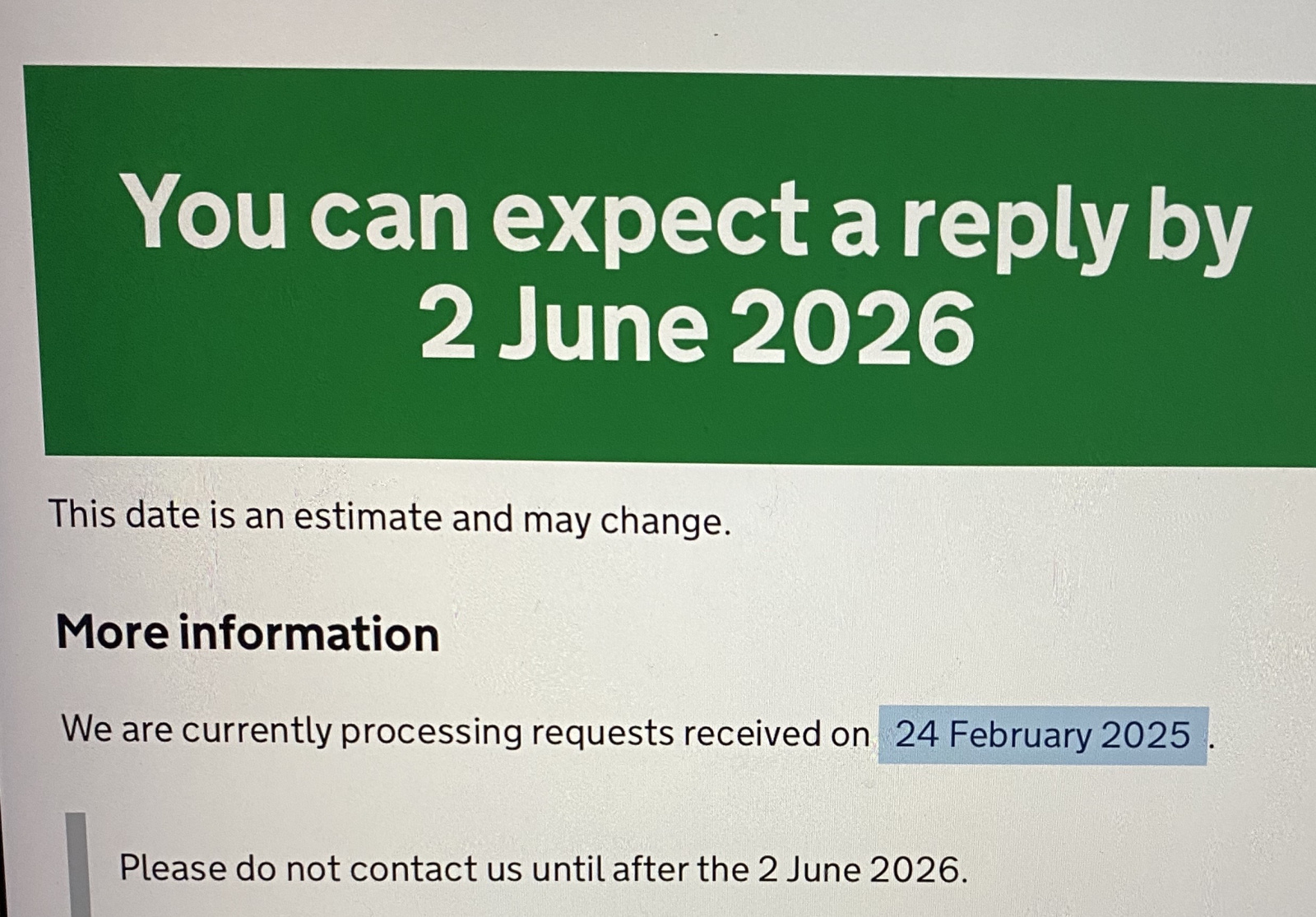

I’d be grateful if someone can suggest the best way to lodge my complaint, if a letter is likely to take ages to process. Is there any value in approaching a third party - CAB, MP?I don’t want to end up having to pay for the available years before time runs out, simply because HMRC’s complaints dept. can’t cope.0

-

The problem of course is who is responsible for the change in the record as there are 2 distinct organisations involved, DWP which covers many individual departments responsible for benefit credits and HMRC both the keeper of the records and responsible for employment credits.It could be worth contacting your MP's office, or maybe former pensions minister Steve Webb who writes in This Is Money or one of the other newspapers.And this is where my confusion begins - the value of “full years”. Everyone tells me not to bother with the actual number of years involved in my pension calculation,

The complication is that there is a distinct split in the pension pre and post 2016. A pre 2016 year can be worth £6.58 or £5.88 depending on personal circumstances. If the latter then there could be additional pension on top, if the former then there is the possibility of a contracted out deduction reducing the total amount due. This means that pre 2016 the number of years is not really relevant and the calculation in £s at April 2016 is the only thing that matters and someone who has 29 years could have a greater amount than someone with 40 years.

1 -

Oh dear, I see what you mean, and there was me thinking that three weeks was enough for some sort of acknowledgment !!!!!!…

By which time, I’ll have lost the opportunity to buy back one of the available years, so I might as well pay (again) for the three I can retrieve and accept that I’ll never get back to the full rate.0

By which time, I’ll have lost the opportunity to buy back one of the available years, so I might as well pay (again) for the three I can retrieve and accept that I’ll never get back to the full rate.0 -

This has been proper banging head against wall stuff.

In light of the advertised delays, I rang HMRC again and had a series of young people playing a dead bat and sending me to the self-assessment team, then the NI team; the only consistent point made was that it was a DWP matter. And we know what they say.

The final one I spoke to couldn’t see any removed credits or notes to explain any alteration, but could see the years with voluntary contributions remaining.

Ultimately, they had no explanation and claimed not to have come across this before. They all “completely understood my situation” and the suggestion was that I wait until my letter is opened and a case-worker can look at it. Understandably, I was a little miffed at waiting until summer but was unable to glean any useful alternative route. The call-handlers are merely there to field simple questions and guide callers along preferred pathways; there’s absolutely no point in losing your rag with them.I can’t believe that, amongst all the people I’ve spoken to at both Departments, or whoever I’m put on hold for while they “just check with someone”, no-one says they recognised the action of removing credits and reducing entitlements.HMRC has no useful information accessible to the call-handlers; DWP (who sent all the original letters and calculations, as well as the recent updated ones) knock it back to HMRC, who give them the figures to use for calculating each pension.If the snail-mail route is log-jammed, every other possible route likely is similar. I keep tweaking my complaint letter, but the original will have to do - I was even wondering about an FOI request, just to learn a bit more.

I accept that they’re swamped with calls and have generic call-handlers and a massive mail backlog but it’s taking the pee from my vantage point -

They won’t claim back the overpayment, so it’s not as though I did anything wrong

They made an error with my original award, despite my following and relying on their figures

It took 18 months to implement the reduction, meaning that it’s too late for me to climb back to full pension; I’m currently £1300pa down from full rate and another £840 voluntary payment will restore £900-ish of that.

No-one in either Department can offer any explanation for what’s happened

It feels like a slam-dunk !!!!!!-up but it’s probably a routine minor adjustment, implemented belatedly and without notes on the system.1 -

I thought it couldn’t but it’s become ever more baffling…

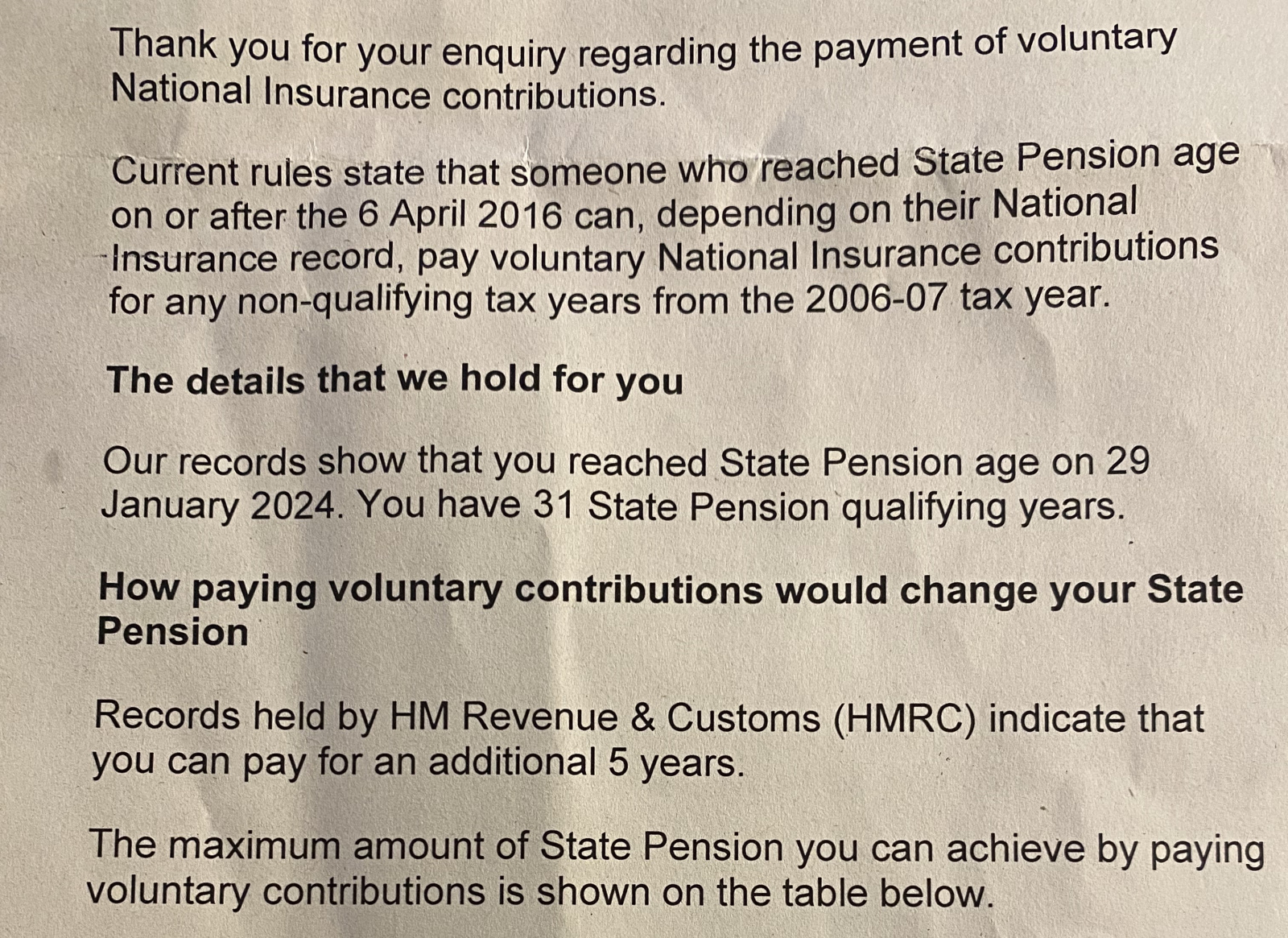

Today, received a letter from DWP that really confused me; all I could think was - well, sounds promising, at least.

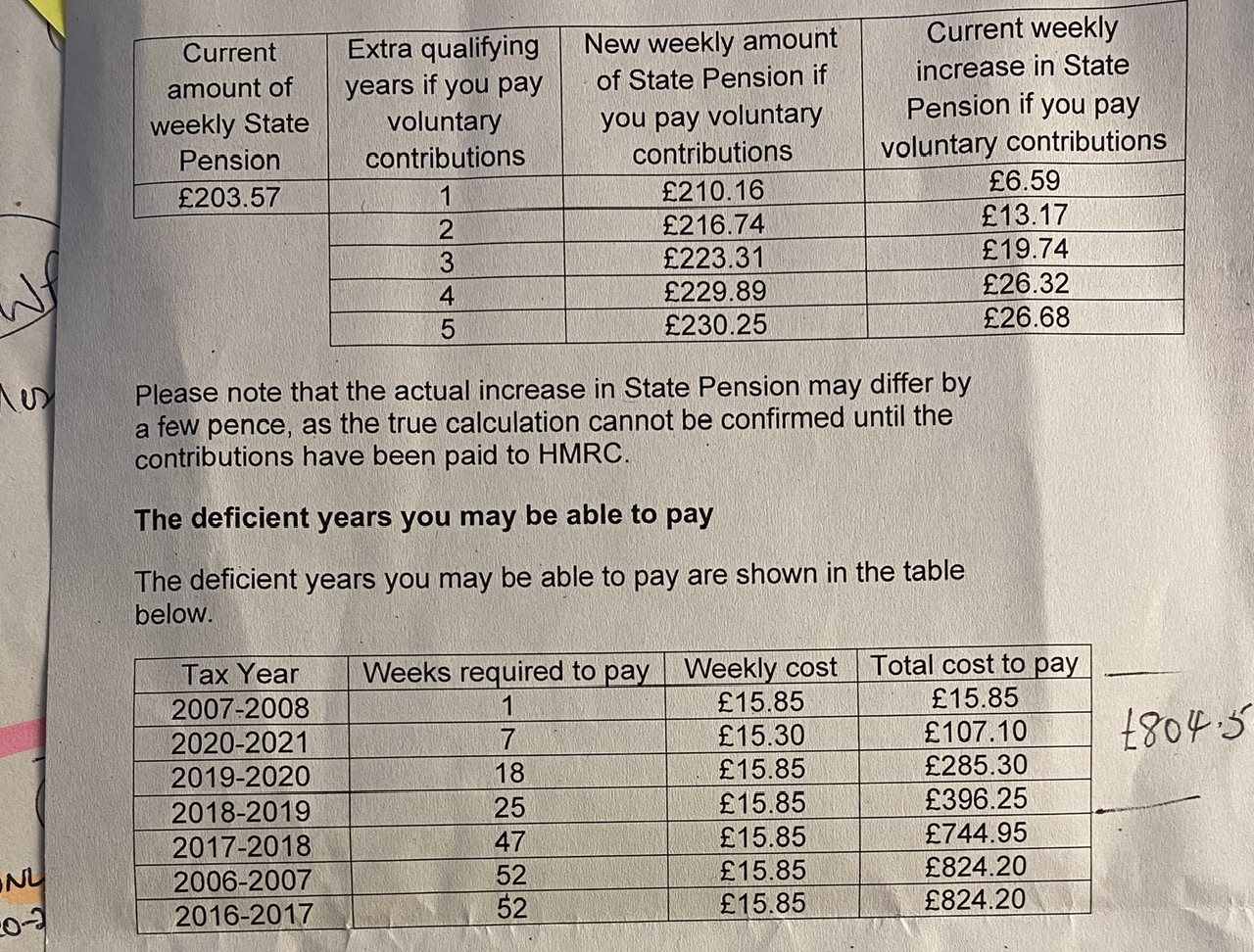

It went on to demonstrate not only which years were available but which would be cheapest to fill. According to their figures, I could make up 5 years to reach the full SP rate for £1549.45. However, since I’d been content for 18 months receiving a few pence less than full rate, it would be a no-brainer to save £744 and make up only 4 years, and forgo the extra 36p every week. Note how far back they’re going. What happened to 6 years? And what does “depending on their National Insurance record..” mean?

Note how far back they’re going. What happened to 6 years? And what does “depending on their National Insurance record..” mean?

My online NI record hasn’t been altered, so there are disparities between that and this list.

Call DWP - tentatively suggested that NI removals might be connected with other benefits I had, possibly UC…couldn’t make much headway and we presumed that the letter was an automatic response to updated figures from HMRC. DWP’s letter was full of ifs & maybe’s so it was off to HMRC to see if I was eligible.

HMRC - it turns out that my letter of complaint was opened pretty promptly, about 10 days ago!

This call-handler was much more on the ball than previously, and was able to tell me that two teams had read my letter and the matter had been raised to a Tier1 issue. The CH took the trouble to read it while on with me and confirmed what I was told previously - that they could see that credits had been removed but had no explanation why.

As to why DWP were triggered to send their letter, we couldn’t find out. There seems to be some left hand/right hand ignorance between the two departments. The adviser confirmed that it was odd for there to be no explanatory note on my account but reassured me that things should be moving with haste now.

Let’s hope that Tier1 means something!2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards