We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Has UC removed my NI credits a year into my pension?

Comments

-

I’m pleased to report that DWP did send a letter - generic but correct.

Coincidentally, same delivery brought an HMRC tax code notice for this year (starting 6/4/25) which includes my new, reduced pension in the calculation.£12570 (PA) less £10578 (pension) = £1992 tax-free (code199L). Straightforward enough, but now I wonder what might have a hidden knock-on effect on something else.

In the DWP letter that began all this (only a few days ago), headed - A change in your entitlement, it began

“The amount of your state pension has changed. You are entitled to a state pension of £180.23pw, starting on xJan ‘24”.

“From 8 April ‘25, the amount will be £203.37pw”. Those, presumably, are the figures they’d rather have had at the start; whereas I now have letters and notices with the original ‘24/‘25 tax years and revised figures, but with Sept.’25 printing/posting dates on.

DWP explained this time that they’d set the pension level correctly, in accordance with my NI record they recently received from HMRC. And that it was backdated 20 months right to my birthday. HMRC evidently “found something“ that’s altered things, but they haven’t asked for the return of the £1850, nor have they given any explanation of what’s behind all this.

As I’ve explained, I was receiving a four-weekly amount that was only pennies away from the full SP amount, and I probably put it down to leap-days or something.This is one original notice from 19 April 2024, and there’s also an Award notice & Statement of details from 18 April 2024 confirming the figures. Both of those are from DWP and they’ll simply say that they calculated payments from whatever NI figures HMRC gave them. My NI record shows that certain years had voluntary contributions made, years that no longer have enough statutory credits to qualify toward the state pension. Those VC’s have now been left redundant and it’s evident which years have had credits removed.Even if I make voluntary contributions to the last 3 available years, I’ll still not make it back to where I was. And that is the central point of my complaint - I lost the opportunity to retrieve my position, and I’m none the wiser on what brought it about. The long-term ramifications to me (+partner) are significant. Even if they provide a rational/legal reason for the changes, it’s been handled very poorly.

My NI record shows that certain years had voluntary contributions made, years that no longer have enough statutory credits to qualify toward the state pension. Those VC’s have now been left redundant and it’s evident which years have had credits removed.Even if I make voluntary contributions to the last 3 available years, I’ll still not make it back to where I was. And that is the central point of my complaint - I lost the opportunity to retrieve my position, and I’m none the wiser on what brought it about. The long-term ramifications to me (+partner) are significant. Even if they provide a rational/legal reason for the changes, it’s been handled very poorly.

I can’t help feeling a little daunted at the prospect of challenging HMRC but, in the absence of anything further, I think I’ll have to, more or less on the grounds that I’ve touched on.0 -

Well, it’s got to be done; I’m sending a complaint to the appropriate dept at HMRC.

I’ve tried to keep it concise because I have a tendency to waffle.

If anyone has any comment on the tone or substance, I’d appreciate suggestions.I am contacting you to express my dismay over the handling of a recent alteration to my National Insurance account, which has had a significant knock-on effect to my state pension.

I qualified for SP at my 66th birthday, Jan 24; I took an interest in the standing of my NI contribution record and, informed by the SP forecast, I took the necessary steps to ensure that I would receive the full state pension.

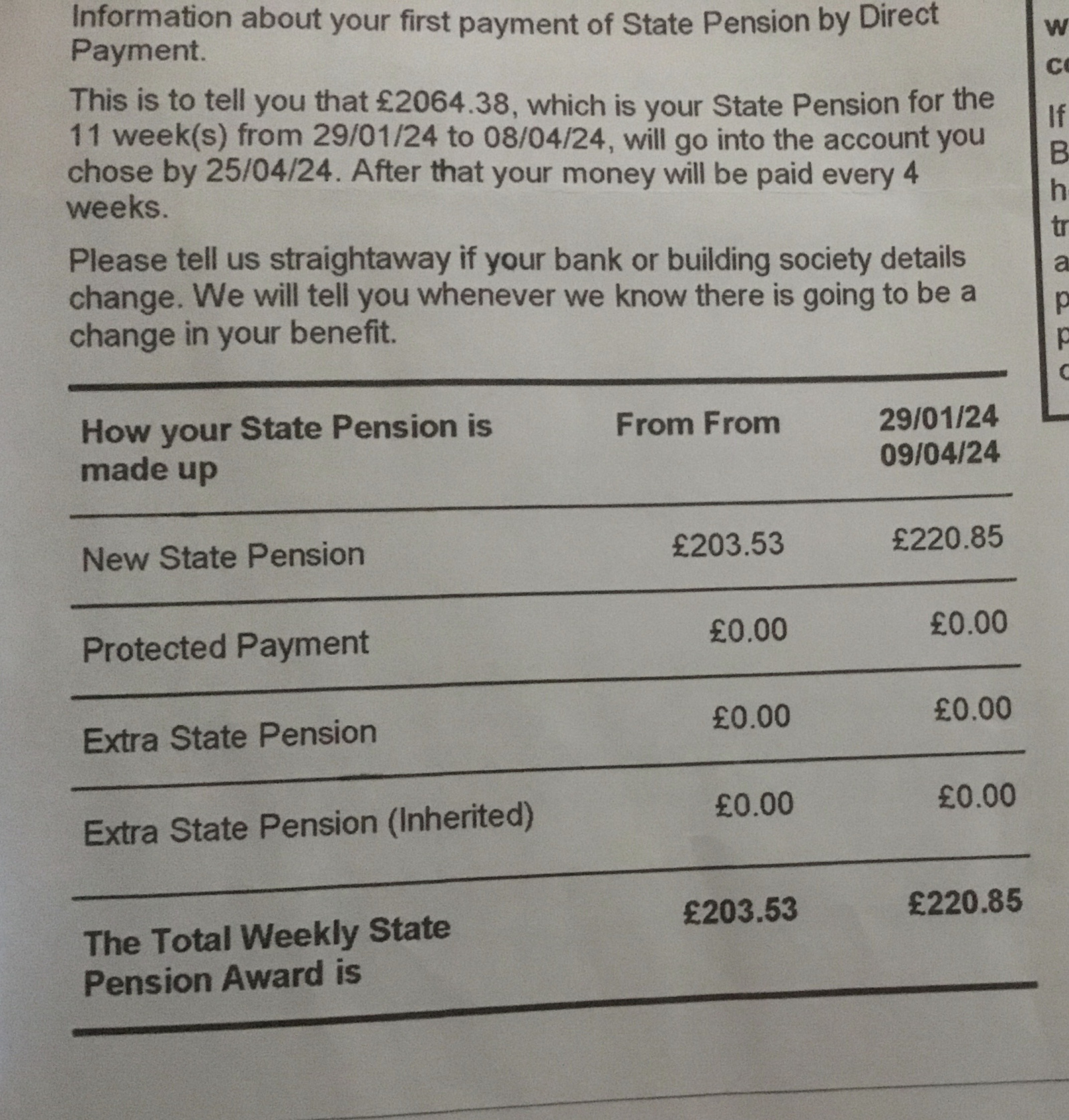

This was successful and was confirmed in at least two DWP letters – Award notice & Statement of details (18/4/24) and another letter (19/4/24 letter Ref.BR2198(NSP)).

The amount awarded was within pennies of the full pension rate, and I accepted that it was, in effect, the full rate. I received this rate from April 2024 until now, including the 25/26 uplift.

Correspondence from DWP, dated 12/9/25, told me that HMRC had recently “reconciled my records” and provided revised NI figures. The result of this was that my state pension was to be reduced significantly and, furthermore, I have lost the opportunity to restore the position.

The only explanation I received, from DWP, was that HMRC had “removed several credits from my record”. This had the effect of reducing a handful of years to below the qualifying contribution threshold.

18 months ago, my contribution record qualified me; an Award notice confirmed it; and I began receiving my pension. This letter has arrived, out of the blue, and no one has been able to explain what’s behind it. The HMRC call handler confirmed that one particular year had had credits removed but offered no further explanation.

It is evident, in my record, where credits have been removed, as those years contain left-over voluntary contributions, paid to make up a qualifying year. A total of four years were lost from my record – I can possibly make up three of them, for £840 – the other year is now outside the time limit. There’s no possibility of my being able to achieve the full pension rate again.

Whatever the issue is, there is no need to take as long as it did. Had I received correspondence about what was happening, before April 2025, I’d have been able to do something about it.

My complaint is this – whatever the reason for removal of credits, it’s distressing to learn, this far into my retirement, that my pension will drop by 9% but I can buy back some of it.

I consider that, given the existing difficulties and constraints of retirement planning, this has treated me unfairly, in that I can no longer get back to the full pension level, that I’ve been paid for 18 months; and the potential stress of this news should have been predicted, coming so late in the day.

I request that HMRC restore my position, preferably with the full pension, but at least with the option to pay VC’s sufficient to achieve that.

All I want is to be no worse off than previously, with one thing less to worry about.

Yours faithfully,

National Insurance and employer complaints

Write to HMRC if your complaint is about National Insurance or employers.

NIC and EO Complaints

HM Revenue and Customs

BX9 1AAHow to complain by post

You do not need to include a street name, city name or PO box when writing to these addresses.

Write ‘Complaint’ on the front of the letter and include your reference number if it is shown in any letters you have from HMRC.

Tell us if you need extra support with your complaint because of a health condition or your personal circumstances.

0 -

I hesitate to suggest this as it will make the letter longer but I think you need to spell out in more detail the steps you took to pay voluntary NICs. So I would change this bit

"I took an interest in the standing of my NI contribution record and, informed by the SP forecast, I took the necessary steps to ensure that I would receive the full state pension."

to say something like

"In [insert year or put On date] I paid £[insert amount] of voluntary NICs in order to boost my state pension to as near to the full amount as possible." [Say whether you did this online or after speaking to someone at DWP/HMRC - something like "I checked my NIC record at the time online and relied on the accuracy of that record when topping up years (insert which tax years) shown as partially full. Or I spoke with DWP to ascertain how much I needed to pay and for which years. That conversation was based on my NI record being accurate.]" I would specify which years you topped up and how much was paid for each one (assuming you still have that information). Maybe do a schedule showing the credits as they were when doing the topping up how much you paid in voluntary NICs and what the new figures are for credits. I think you need to be precise about this rather than talking about "a handful of years".

I am sure you can polish that but the point you want to be making is that you (and perhaps the person at DWP who helped with the voluntary NICs) were relying on the records being accurate when you paid the voluntary NICs.

You also want to be making the point that you did the topping up before the April 2025 deadline and so they should allow you now to top up years that are now closed - identify the year and link that with your point about not being able to fill all the gaps you need to fill now that April 2025 has passed (which of course you would have been able to do if they had reconciled their figures sooner or got the figures right in the first place).

You have two lines of attack and you have blended them together in a way which may be very clever.

I might have split them in two along these lines

"Could you please explain why the NI credits showing on my record have been removed. And

1 If their removal is incorrect could you please credit them back so that I have full years or

2 If their removal is correct can you please allow me to top up years [a b c and d - the incomplete years including the one which is not now available] and confirm that this top up will have effect as if made back in [year you did the top up] so that my state pension is restored to its proper amount."

But your version might work better.

2 -

Thanks @DRS1, I think we’re on the same wavelength. I didn’t want to be cod-legalistic with it but it needs tightening up slightly. What’s been bugging me is that there is probably a perfectly reasonable explanation for the removal of credits, which seem to number 48weeks or thereabouts. What’s not reasonable is the delay in applying their removal and a lack of details.

When my pension forecast was generated, I presume the figures were correct at the time and that something only came to light later on, possibly very recently. Best guess is that it was in connection with UC credits.

I’ll re-jig the letter, but there’s only so many ways I can insist that I did it all by the book, and relied on figures expressly calculated for my pension.

To be honest, I believed that there would be respondents who would be familiar with NI weeks being credited and who could shed some light.

Whatever’s gone on, it remains the case that I’m feeling hard done by after 18 months; my income has dropped; I’ve lost the opportunity to make it up; I’ve lost money on Voluntary Contributions now redundant; and it has caused some anxiety (otherwise known as leaving me rather !!!!!!-off). These are the points I need to bear in mind.

I shall update my letter and see what happens.0 -

It may be me, but I didn't see anywhere in there that specifically asked for the reasons the credits were removed for each year they were taken from. This may help you down the line as I can't see this being resolved with one letter each from you and HMRC.........Gettin' There, Wherever There is......

I have a dodgy "i" key, so ignore spelling errors due to "i" issues, ...I blame Apple 0

0 -

To be honest, I believed that there would be respondents who would be familiar with NI weeks being credited and who could shed some light.

The trouble is no-one has any information on which to go so any suggestions would just be speculation.

You believe it is down to a removal of credits linked to UC but to know that you would need to know what your record said for each year before it was reconciled and what it says afterwards - ie to know what has disappeared. You may be able to see the current position if you look at your NIC record online but unless you took screenshots back when you were topping up you probably don't remember what it said back then. But perhaps you just haven't mentioned it on here.1 -

You mention self employment. I thought it might be useful to see how self employment NIC credits and voluntary contributions appear on my NIC record (though you probably know this already)

1 -

Quite so, @DRS1, I got quite familiar with my NI record last year. For instance, ‘19/‘20 currently shows Voluntary 30 weeks, NI credits 4 wks. That’s clearly one that I topped up to make a full year. 18 weeks NI credits have been removed, that would make it up to 52 weeks; that’s confirmed because 18x£17.75 (class3) makes £319.50, which I’m invited to pay to make up the full year. By seeing how short I was of the full pension, knowing that they were using the class3 rate, and counting the missing weeks from any that contained VC’s, it became clear that 48 weeks’ credits had gone, in total.

22/23 is showing 52 weeks NI credit to make the full year. If they’d taken most of that year, they’d have had the 48 weeks that they wanted removed, for the loss of only one full year. It suggests that the credits have been removed from specific years rather than just a grab of 48 credits. I’m not sure how that year generated 52 credit weeks, but it’s the only year I had like that, and I was working throughout.

The one that’s now out of reach, 18/19, shows VC’s of 13 weeks and credits of 14 weeks. All the years showing Voluntary Contributions are clearly ones that I had made up to full years and those VC’s are now doing nothing. It would be nice if I could shift my impotent/out of time VC’s to pay toward the years I can still complete.

@GunJack, I’ve updated my draft letter, as per @DRS1’s suggestion, to include specifically the question at the heart of all this - why was it done?

This is what I’m going with:I am contacting you to express my dismay over the handling of a recent alteration to my National Insurance account, which has had a significant knock-on effect to my state pension.

I qualified for SP at my 66th birthday, 29 Jan 24; in Jan & Feb 2024 I paid £2068.80 of voluntary NICs in order to boost my state pension to, as near as possible, the full amount. I checked online my NIC record and State Pension forecast and relied on the accuracy of those records when topping up years showing as partially full.

This was successful and was confirmed in at least two DWP letters – Award notice & Statement of details (18/4/24) and another letter (19/4/24 letter Ref.BR2198(NSP)). Since then, I have received weekly equivalents of £203.53 in 24/25 and £229.89 in 25/26, which are the amounts awarded.

Correspondence from DWP, dated 12/9/25, told me that HMRC had recently “reconciled my records” and provided revised NI figures. The result of this was that my state pension was summarily reduced by a significant amount.

The only explanation I received, from DWP, was that HMRC had “removed several credits from my record”. The upshot is that I now have 31 full, qualifying years of NI contributions in place of the 35 at the start of my pension. The removal of credits has eliminated four of my qualifying years and my pension entitlement has dropped commensurate with that.

At the time I paid the Voluntary Contributions, I was able to reach back beyond the usual six-year limit to find useful partial years. This opportunity has now closed, such that one of my “lost” years (18/19) has now fallen outside the cut-off. Had I been told about this significant change before April 2025, I’d have had the chance to make up all four of my lost years. It is evident where credits have been removed, as those years contain left-over voluntary contributions, paid to make up a qualifying year. A total of four years were lost from my record – I can possibly make up three of them, for £840 – the other year is now outside the time limit. There’s no possibility of my being able to achieve the full pension rate again.

18 months ago, my contribution record qualified me; an Award notice confirmed it; and I began receiving my pension. This letter has arrived, out of the blue, and no one has been able to explain what has happened. The HMRC call handler confirmed seeing that one particular year (20/21) had had credits entered and later removed but offered no further explanation.

My complaint is this – whatever the reason for removal of credits, it’s distressing to learn, this far into my retirement, that my pension will drop by 9%, albeit I can buy back some of it, for the second time.

I consider that this late adjustment to my contribution record has treated me unfairly, in that I can no longer get back to the full pension level, that I’ve been paid for 18 months; and the potential stress of this news should have been predicted, dealing as it does with retirement planning, which is more onerous for some than others.

Could you please explain why the NI credits that had been showing on my record have been removed; and,

If their removal is incorrect, would you please credit them back so that I have full qualifying years, or

If their removal is correct, can you please allow me to top up sufficient years, including 18/19 and confirm that this top up will have effect as if made in 2024, so that my state pension is restored to its proper amount. It would be reasonable to allow my idle Voluntary Contributions – 13 weeks’ worth in 18/19 - to be put towards this, as that was the intention when I paid them.All I want is to be no worse off than previously, and that HMRC allow me to restore my previous position.

Yours faithfully,

I can’t keep tweaking it, and I don’t think I’ve left any glaring errors or repetition.0 -

Don't worry, I am not going to suggest any tweaks.

The fact that the missing credits were NI credits rather than self employed credits suggests you were right that the issue is somehow connected to benefits rather than say some issue with self employed contributions (which can give rise to issues as mentioned by others on here).

Let's see what HMRC say. Good luck.1 -

To date, HMRC have said nothing…I thought I’d wait and find out if the payment had decreased this month which, of course, it has. Down to 814, which equates to about 12% or £1400-ish pa.

They must’ve received my letter 3 weeks ago and I’d hoped for at least an acknowledgement by now. My fault for sending it merely first-class (my town’s PO is the end of a mini-market counter, that occasionally is staffed). This time, it’s going to be signed for.

Of course, there might be something in the mail today - I’ll wait until then before re-sending the complaint (with covering note).

At worst, I have until March to make up the (available) years, which will add back £144 per month, for £840. That will pay for itself after 6months and I’ll be down £35-odd per month, going forward.When I receive some form of response to the complaint, I’ll have a better idea of how to feel about paying voluntary contributions for a second time. I look forward to having something concrete to report in due course…

On a closely-related point, my partner (9 years younger) has zero full years showing in her NI record but her pension summary indicates a current weekly expectation of £116 on her “to-date” NI record, £175 if contributing until 2033, and £201 if she makes up shortfalls from last 5 years.

How does one build up any pension entitlement with a record of zero “full” years. Until last year, she received an increment on our UC claim under Limited capacity to work and she claims PIP, related to that. There was another amount for me as I was (and remain) part-time carer. She was not expected to look for work but there’s no indication that her NI record was safeguarded or topped-up during that time. 6 years are missing entirely from her record, including 22/23 when nothing was different from 21/22 or 23/24.

This suggests that even minimal NI credits are aggregated and count toward one’s pension. If that were the case, my accumulated “partial” years would have counted toward my pension. I know I had some confusion about reaching 35 full years and it seems that, purely by chance, achieving that number got me to within pennies of the full pension.

Can someone please explain if I’ve a fundamental misunderstanding about this, ie. how does she qualify for well over half the full pension with no full years recorded?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards