We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Branch savings advice please

Comments

-

With the Halifax, NatWest & Barclays how likely are they to have access to a branch in the futurepookey said:Hi everyone,

Family friends have come into money and are asking for advice on savings accounts. They are elderly so don't do online banking so are looking for branch based accounts.

They currently bank with YBS, Halifax, Barclays , Nationwide and natwest.

The amount they have in savings is around £75k each.

I've had a very quick look and seen that YBS have a fixed branch based ISA around 4% and Rainy day saver around 4% too. This would account for 30k each.

Can anyone recommend what to do with the other 30k please? I would prefer to keep it simple and not open too many different accounts so it's easy for them to keep track if possible. They don't really need access to the money so it can be fixed.

Any advice would be much appreciated.

0 -

I expect branch still exist in major City?35har1old said:

With the Halifax, NatWest & Barclays how likely are they to have access to a branch in the futurepookey said:Hi everyone,

Family friends have come into money and are asking for advice on savings accounts. They are elderly so don't do online banking so are looking for branch based accounts.

They currently bank with YBS, Halifax, Barclays , Nationwide and natwest.

The amount they have in savings is around £75k each.

I've had a very quick look and seen that YBS have a fixed branch based ISA around 4% and Rainy day saver around 4% too. This would account for 30k each.

Can anyone recommend what to do with the other 30k please? I would prefer to keep it simple and not open too many different accounts so it's easy for them to keep track if possible. They don't really need access to the money so it can be fixed.

Any advice would be much appreciated.

Pensioner has free bus pass and time, so don't too worry about it...1 -

Thank you, the bond is the same rate at YBS so I'll help them to set it up there as going to help them open a couple of other accounts there tooxylophone said:If they don't need access, how about a fixed rate (branch) bond with Nationwide?

https://www.nationwide.co.uk/savings/fixed-rate-savings-accounts/1 -

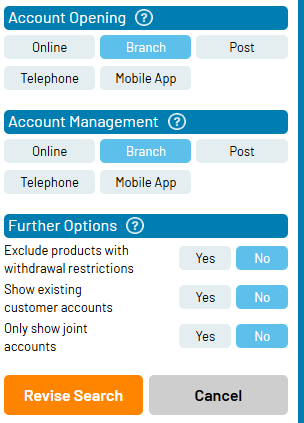

This is great, thank youBridlington1 said:It's worth noting you can also filter accounts on moneyfacts to show only accounts that can be opened and managed in branch.

To do this, go to moneyfacts, then full search and change the account opening and account mamagement sections to branch. Then click ``revise search".

Also make sure to sort the accounts by rate: 1

1 -

Thank you, YBS has a fixed rate bond at 4% which isn't too bad. I'll try to find out what the procedures are.lr1277 said:I would suggest building up cash ISA's. My reasons are as follows:When both my parents were alive, my dad had a occupational and state pension. My mum is still alive and had a state pension. Mum never paid tax as she never earned enough.After dad died, both his occupational pension and state pension transferred to mum. Some of his savings account also transferred to mum. The only accounts that didn't transfer were his cash ISA's. Suddenly she was paying tax on her increased income. This coincided with the rise in interest rates after many years of low rates. This led to a situation where HRMC kept sending out different tax codes to her occupational pension provider, each one meaning her net pension income was reduced. Mum was upset that each tax coding notice led to a decrease in her net pension. Once we realised what was going on, we moved as much of her savings as possible into cash ISA's and will continue to do in each new tax year, whilst funds are not in ISA's.Positives with a cash ISA: Less tax to payNegatives: I am under the impression non-ISA savings accounts have higher rates of interest than cash ISA accounts. You (or they) may not want to think about this, but once one person in the couple dies, getting the ISA money to the living spouse maybe more difficult and may involve probate or letters of administration. But if it is a branch based account and they are both known at the branch, who knows what the procedures are?But this all depends on finding a branch based cash ISA that pays an acceptable rate of interest.0 -

They live in London so it shouldn't be too difficult35har1old said:

With the Halifax, NatWest & Barclays how likely are they to have access to a branch in the futurepookey said:Hi everyone,

Family friends have come into money and are asking for advice on savings accounts. They are elderly so don't do online banking so are looking for branch based accounts.

They currently bank with YBS, Halifax, Barclays , Nationwide and natwest.

The amount they have in savings is around £75k each.

I've had a very quick look and seen that YBS have a fixed branch based ISA around 4% and Rainy day saver around 4% too. This would account for 30k each.

Can anyone recommend what to do with the other 30k please? I would prefer to keep it simple and not open too many different accounts so it's easy for them to keep track if possible. They don't really need access to the money so it can be fixed.

Any advice would be much appreciated.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards