We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Buying shares for the first time.

GE0RDIE

Posts: 23 Forumite

Hi

I have joined a group that offers shares advice (as in which shares to buy and when to sell).

I've followed the advice without actually following through, as a test. If I'd bought and sold as advised, I'd have made about 7% in two months.

I have decided that I can afford to lose £200.

I'd like to buy and sell as advised in the group, starting low and risking a maximum of £200. If I lose the £200 I'll happily accept it as a lesson learned and stick to less risky forms of investment.

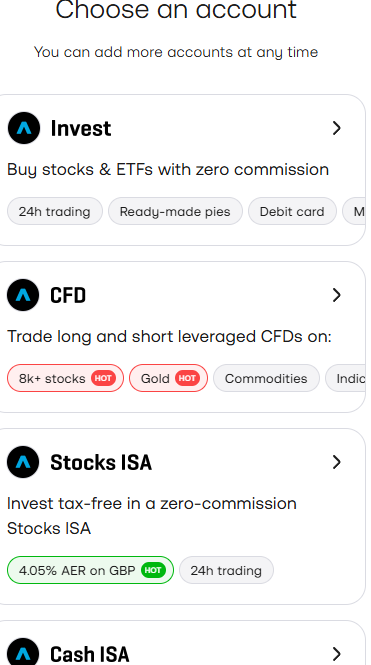

With that in mind, I'm going to open an account at Trading212. I have a choice when opening the account. Should I choose the top one, buy stocks and ETF's? I'll be selling as well as buying.

Any further advice? Has anyone used Trading 212? It appears to offer free buying and selling.

As you can tell, I'm a complete noob, so please no sarcasm.

I have joined a group that offers shares advice (as in which shares to buy and when to sell).

I've followed the advice without actually following through, as a test. If I'd bought and sold as advised, I'd have made about 7% in two months.

I have decided that I can afford to lose £200.

I'd like to buy and sell as advised in the group, starting low and risking a maximum of £200. If I lose the £200 I'll happily accept it as a lesson learned and stick to less risky forms of investment.

With that in mind, I'm going to open an account at Trading212. I have a choice when opening the account. Should I choose the top one, buy stocks and ETF's? I'll be selling as well as buying.

Any further advice? Has anyone used Trading 212? It appears to offer free buying and selling.

As you can tell, I'm a complete noob, so please no sarcasm.

1

Comments

-

Yes - take the top option. You don't want to waste your ISA allowance with a bit of dabbling. CFDs would generally carry more risk so my advice would be to steer clear of these until you understan the details1

-

I'd go with the stocks ISA option unless you're using (or planning to use) your full annual allowance already on cash products - investing outside an ISA wrapper involves more record-keeping for tax purposes, which may not be an issue at the outset but will hopefully become one if continuing the investment journey!3

-

Trading 212 is brilliant. Apart from a few pence of foreign exchange if you e.g. buy shares in $ or euros, trading is free.

Yep that's right - you want the "invest" stocks ISA option (edited, eskbanker is right I think). Make sure you switch it to real cash (initially it might show you £5000 of practice money!).

CFDs are so risky that they are actually banned for retail (individual) investors in the US. They are a form of spread-betting and a good way to lose your shirt.

That's highly unlikely with standard equities or ETFs. Stick to those and you're at very low risk of totally and permanently losing your £200. Losing 10-20% would be a very bad-terrible outcome, which it sounds like you can shrug off. The other side of the coin: if you make 7% every two months, then everyone will be coming to you for tips. The losses and gains will average out over time (the key thing). Making 1% a month would be an excellent return.2 -

Just another tip which (almost) bit me: presumably you haven't used up any of your capital gains (£3K) or dividend tax (£500) allowances this year, or indeed your PSA for savings interest? If by some chance you did, be careful about holding ETFs unwrapped (i.e. outside an ISA) as you would then be liable for tax on them and it is complicated. The amounts would probably be tiny, but in theory you would need to report them to HMRC which could be a pain.

(if the answer is "I don't know", that's fair enough and means you almost certainly haven't!)1 -

Wow great advice. Better than expected. I've gone with the top one, as it's just a bit of dabbling, and I might well use my ISA before the end of the tax year.

Trading 212 does appear to be very good. Obviously a steep learning curve and a lot over my head, but very clever how it gives an instant valuation. I've made 10p already!

Many Thanks.

1 -

My advice, stay clear of what you dont understand, until you learned a lot.

Put that money instead in work pension, you'll get 25% bonus from start.1 -

A bit of low-cost dabbling, as part of a group, can be an effective way of learning rather than doing so solely from reading and researching with no skin in the game. Having said that, there are undoubtedly lower risk ways of investing than dealing in individual shares....Sam_666 said:My advice, stay clear of what you dont understand, until you learned a lot.

But the money will be subject to income tax on the way out again, typically diluting that figure considerably - that's not to say that pension contributions aren't a good idea, but it'll generally be more balanced to set expectations in 6.25% territory rather than 25%.Sam_666 said:Put that money instead in work pension, you'll get 25% bonus from start.4 -

GE0RDIE said:Wow great advice. Better than expected. I've gone with the top one, as it's just a bit of dabbling, and I might well use my ISA before the end of the ...eskbanker was right... starting out with an ISA saves a whole load of hassle with record-keeping.Even if you do find something else to use your ISA allowance on before the end of the tax year, if you are only dabbling with £200 then you'd still have £19,800 of allowance to put into the other thing, and you would be very lucky to benefit more from having that £200 in the other-thing ISA than you would benefit from reduced hassle by using that £200 of allowance to wrap your stocks and shares investing.1

-

eskbanker said:

A bit of low-cost dabbling, as part of a group, can be an effective way of learning rather than doing so solely from reading and researching with no skin in the game. Having said that, there are undoubtedly lower risk ways of investing than dealing in individual shares....Sam_666 said:My advice, stay clear of what you dont understand, until you learned a lot.

But the money will be subject to income tax on the way out again, typically diluting that figure considerably - that's not to say that pension contributions aren't a good idea, but it'll generally be more balanced to set expectations in 6.25% territory rather than 25%.Sam_666 said:Put that money instead in work pension, you'll get 25% bonus from start.

I think that readin and researching should be first step, not by messing with low cost investment.

You're missing point of my suggestion. I wasnt talking about proffit taking but about investment growth.

£100 put in pension become £125 (or more, depending on taxpayer band). That in turn can grow over time to nice levels. Tax efficent ways for taking pesion out will be for discussion in far future, as tax laws will change.1 -

To be clear, I wasn't advocating jumping in without any research, but everyone has to take the first active step at some point, and if OP has determined that they can afford to lose a couple of hundred quid without ramifications then that's no less valid than deferring action for further research.Sam_666 said:

I think that readin and researching should be first step, not by messing with low cost investment.eskbanker said:

A bit of low-cost dabbling, as part of a group, can be an effective way of learning rather than doing so solely from reading and researching with no skin in the game. Having said that, there are undoubtedly lower risk ways of investing than dealing in individual shares....Sam_666 said:My advice, stay clear of what you dont understand, until you learned a lot.

But the money will be subject to income tax on the way out again, typically diluting that figure considerably - that's not to say that pension contributions aren't a good idea, but it'll generally be more balanced to set expectations in 6.25% territory rather than 25%.Sam_666 said:Put that money instead in work pension, you'll get 25% bonus from start.

You're missing point of my suggestion. I wasnt talking about proffit taking but about investment growth.

£100 put in pension become £125 (or more, depending on taxpayer band). That in turn can grow over time to nice levels. Tax efficent ways for taking pesion out will be for discussion in far future, as tax laws will change.

And on the pension point, I wasn't talking about profit-taking either, or investment growth for that matter, neither of which is relevant to the 25% "bonus" you referred to, which shouldn't be seen as a separate issue from withdrawal taxation. It's undoubtedly true that investment should be seen as a long-term activity though, rather than frequent share trading, so if/when aiming for long-term growth then OP would indeed benefit from a different strategy, whether that's within a pension or ISA or GIA, etc.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards