We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Winter Fuel

GibbsRule_No3.

Posts: 575 Forumite

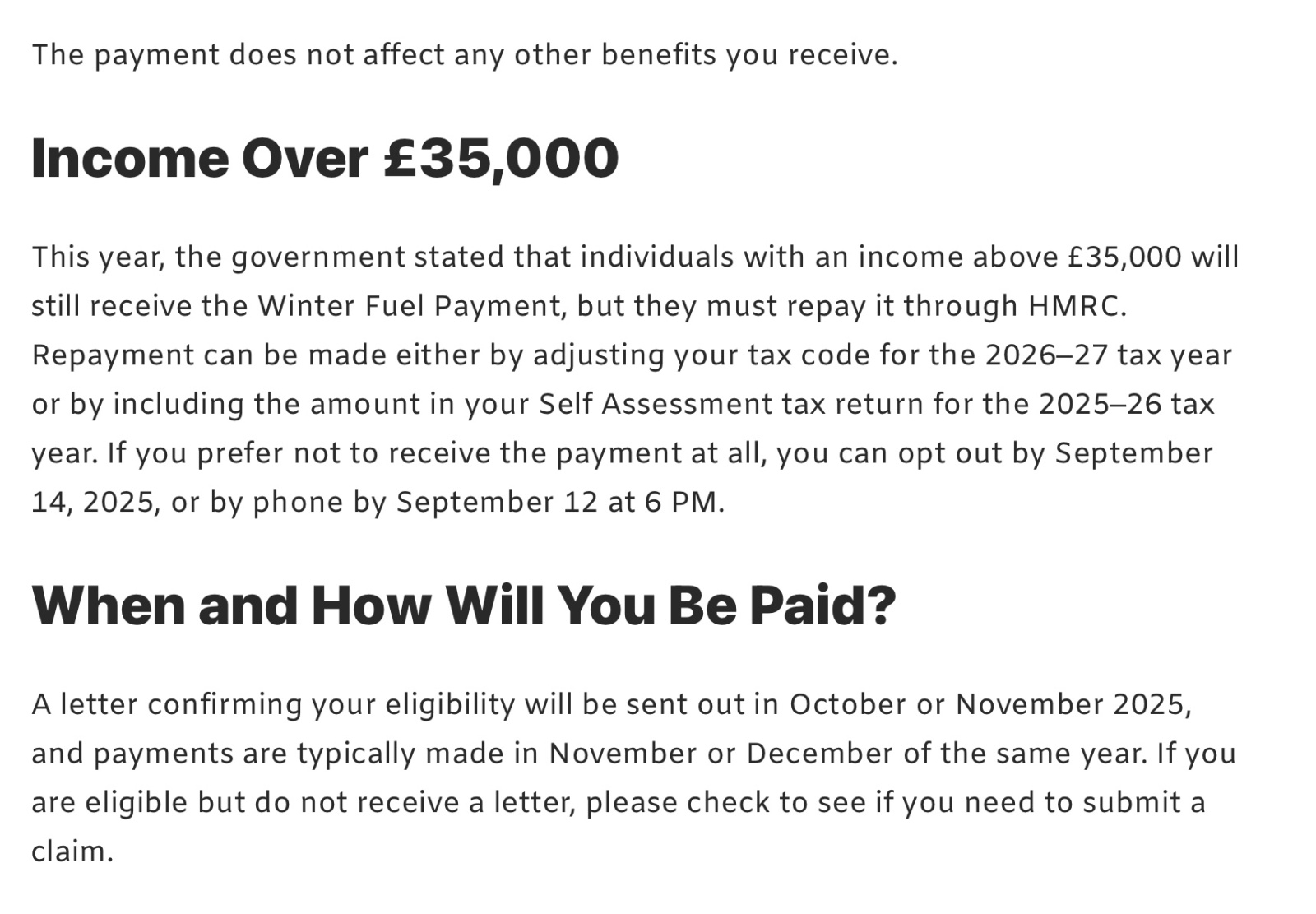

Bearing in mind it is September 7th today, I note that if people want to opt out of the WFP if they are on over £35,000 they need to opt out by 14 September or 12 September, yet people won’t be receiving a letter until October or November. If I had not searched I would not have known, has it been posted everywhere, why were people it could affect not sent letters before the opt out date? I am eligible but also fall within the £35,000 due to continuing work but if I stop early next year then I will fall under £35,000 so expect to be liable for part of the £200 If I opt out and then stop work, it will no doubt muck the Tax system up as it did when I started taking Pensions.

Paddle No 21:wave:

7

Comments

-

Another case of joined up government NOT!4.8kWp 12x400W Longhi 9.6 kWh battery Giv-hy 5.0 Inverter, WSW facing Essex . Aint no sunshine ☀️ Octopus gas fixed dec 24 @ 5.74 tracker again+ Octopus Intelligent Flux leccy

CEC Email energyclub@moneysavingexpert.com1 -

There is an opt out form for online. Ive just filled it in and quite straightforward. They will send confirmation by email.1

-

I’m a Senior Forum Ambassador and I support the Forum Team on the Competition Time, Site Feedback and Marriage, Relationships and Families boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com All views are my own and not the official line of Money Saving Expert.

ARE YOU STRUGGLING DURING THE HOLIDAYS? You may find some ideas on how to cope here:

https://forums.moneysavingexpert.com/discussion/6576551/some-websites-and-helplines-if-youre-struggling-this-christmas0 -

This is my take on it:

Option 1 - Do nothing and I get the money up front and they will slowly take it back (through a tax code adjustment) over the following year; or

Option 2 - Go to the trouble of opting out, then the threshold changes and I go to the trouble of opting back in.

I'll stick with option 1, it's an interest free loan from the government.2 -

I am no doubt doing the same option. I was curious to know though, how many people who might have liked to opt out, knew the cut off date. I can see stories about people complaining that they received the letter telling them they were eligible for WFA but earn £35,000 and it was too late to opt out. I would not have even looked if I hadn’t seen a headline pop up on my iPad about WFA.The_Hawk said:This is my take on it:

Option 1 - Do nothing and I get the money up front and they will slowly take it back (through a tax code adjustment) over the following year; or

Option 2 - Go to the trouble of opting out, then the threshold changes and I go to the trouble of opting back in.

I'll stick with option 1, it's an interest free loan from the government.Paddle No 21:wave:0 -

Wonder what the admin costs will be to reclaim this money, costs that all taxpayers will have to carry.The_Hawk said:This is my take on it:

Option 1 - Do nothing and I get the money up front and they will slowly take it back (through a tax code adjustment) over the following year; or

Option 2 - Go to the trouble of opting out, then the threshold changes and I go to the trouble of opting back in.

I'll stick with option 1, it's an interest free loan from the government.

Afterall if you are on a income over £35k you are not living in penury.Play with the expectation of winning not the fear of failure. S.Clarke0 -

Don't care about the "admin costs" - HMRC are so slow and inefficient I think its much more likely that they will attempt to clawback payments from anyone over the arbitrary £35k whether they have opted out or not.Eldi_Dos said:

Wonder what the admin costs will be to reclaim this money, costs that all taxpayers will have to carry.The_Hawk said:This is my take on it:

Option 1 - Do nothing and I get the money up front and they will slowly take it back (through a tax code adjustment) over the following year; or

Option 2 - Go to the trouble of opting out, then the threshold changes and I go to the trouble of opting back in.

I'll stick with option 1, it's an interest free loan from the government.

Afterall if you are on a income over £35k you are not living in penury.

We are still waiting for them to sort out the overpayment of tax for my wife on interest she never had last year or this. Wrote over 8 weeks ago - still nothing.

! I'll have my £100 upfront thank you !1 -

I don't know where you have read that but everything I've seen shows it's all or nothing.GibbsRule_No3. said:Bearing in mind it is September 7th today, I note that if people want to opt out of the WFP if they are on over £35,000 they need to opt out by 14 September or 12 September, yet people won’t be receiving a letter until October or November. If I had not searched I would not have known, has it been posted everywhere, why were people it could affect not sent letters before the opt out date? I am eligible but also fall within the £35,000 due to continuing work but if I stop early next year then I will fall under £35,000 so expect to be liable for part of the £200 If I opt out and then stop work, it will no doubt muck the Tax system up as it did when I started taking Pensions.

You either pay nothing back or, in your example £200. There is no middle ground.

And if you opt out now you don't even have until the end of the tax year to opt back in, that must be done by the end of March.

https://www.gov.uk/winter-fuel-payment/report-change-circumstances0 -

You have my sympathy on that one, it can be a nuisance sorting that out.brewerdave said:

We are still waiting for them to sort out the overpayment of tax for my wife on interest she never had last year or this. Wrote over 8 weeks ago - still nothing.Eldi_Dos said:

Wonder what the admin costs will be to reclaim this money, costs that all taxpayers will have to carry.The_Hawk said:This is my take on it:

Option 1 - Do nothing and I get the money up front and they will slowly take it back (through a tax code adjustment) over the following year; or

Option 2 - Go to the trouble of opting out, then the threshold changes and I go to the trouble of opting back in.

I'll stick with option 1, it's an interest free loan from the government.

Afterall if you are on a income over £35k you are not living in penury.

If you are able to do it online via a HMRC account it clears a lot quicker than that.

Edit: on your other point I do not see HMRC trying to claim it back if it has never been paid , as it will not be reported to them.Play with the expectation of winning not the fear of failure. S.Clarke0 -

Tax codes are adjusted automatically.

All state pensioners already have a tax code adjustment for state pension rises - sent if necessary to pension scheme provides, employers if still working too.

The opt out scheme is the new admin cost.

Even at £300 max - atcs personal level thats maybe £1pm until tax codes updated - maybe 8-10m after payment if done sa part of p800 type updates that start in Q3 iirc.

But at treasury level say £125 ave for tge c2m pensioners who could opt out who havd lost the tax free - thats another £250 million of govt debt if thry take the cash. A tiny fraction of thr near £3trillion.

So at govt level and gilt rates pushing 5% plus on even short term debt - £1m plus pm extra debt interest.

Hence the opt out.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards