We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

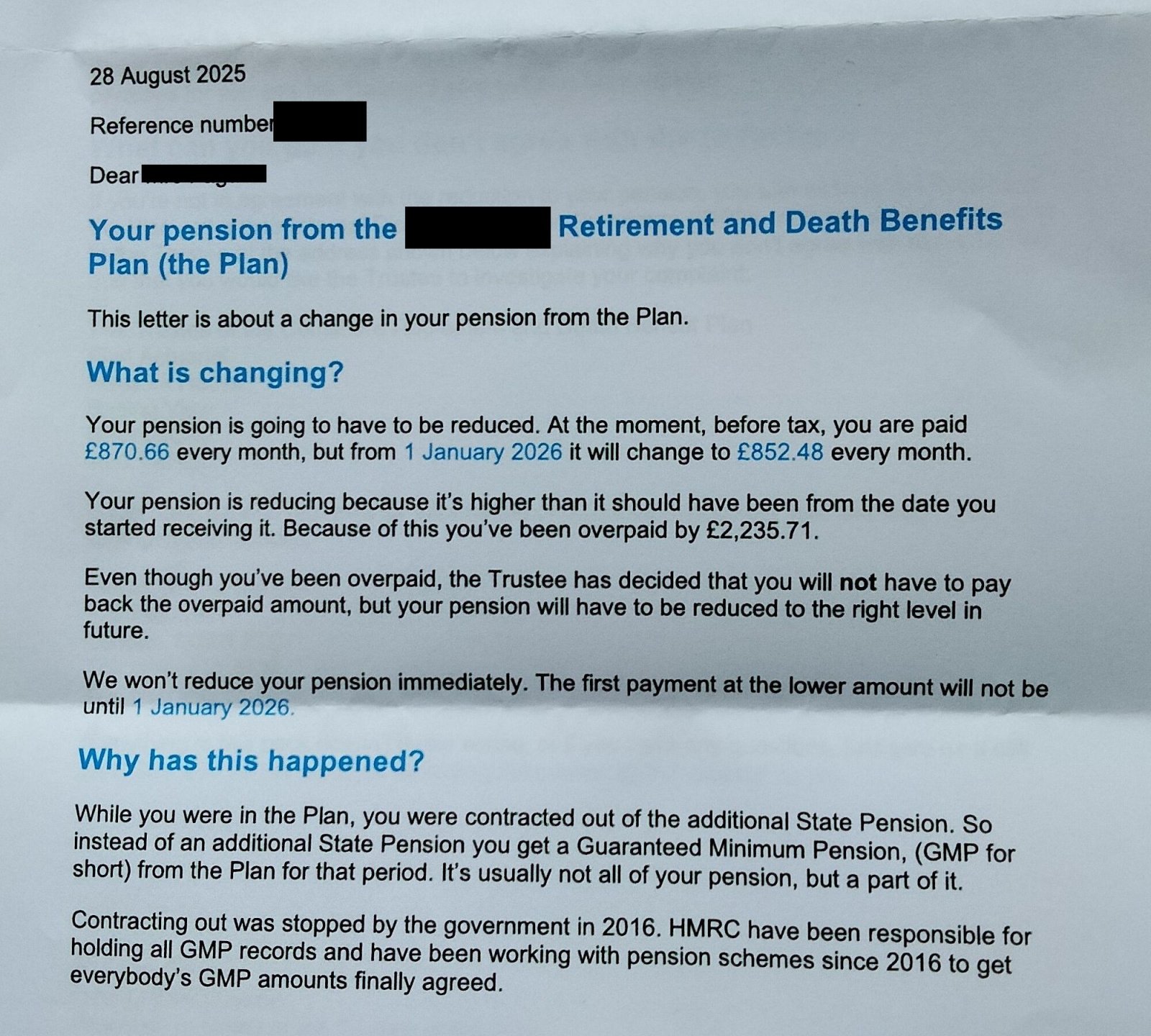

Pension reduced because of GMP recalculation.

My wife is 73. She has just received the below letter from one of her pension providers. It relates to a pension that she started taking in July 2014 at age 62.

If I have understood and calculated this correctly, her before tax pension will reduce by £18.18 per month or £218.16 per year. As she pays 20% tax this is effectively a loss of about £174 per year. We are very comfortable financially so fortunately this is not a worry to us.

I presume that she should just take this on the chin and be grateful that she has profited from the £2,235 overpayment, worth about £1,788 after tax, over the past decade or so. Plus she will get the £18.18 (less tax) overpayment for another four months.

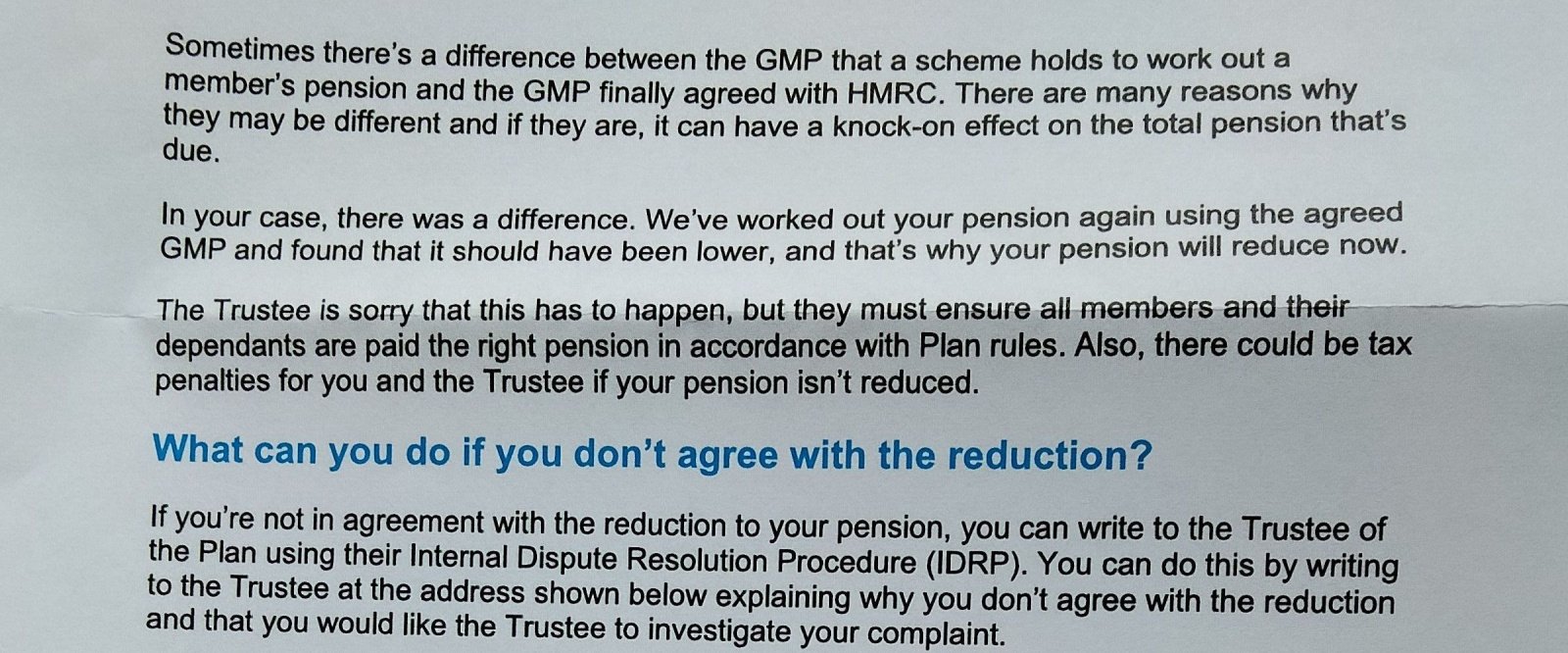

We have no clue how to check whether the letter is factually correct and that the sums add up but presumably a professional pension provider usually get these matters correct.

As she was contracted out of the additional State Pension and received a GMP instead, could this recalculation of the GMP mean that her State Pension should now be increased appropriately?

I haven't named the Pension Provider but I can do that if it makes a difference.

Comments and any useful advice would be welcome.

Thanks.

He said to the salesman, “My wife would like to talk to you about the Volkswagen Golf in the showroom window.”

Salesman said, “We haven't got a Volkswagen Golf in the showroom window.”

The man replied, “You have now mate".

Comments

-

Your starting point would probably to ask to see their sums.

If they overstated the GMP then maybe they understated the excess over GMP? So maybe the overpayment is more to do with increases on the GMP element vs increases on the excess?1 -

Your wife's state pension commenced before 6/4/16?

Does the private pension include pre and post 88 GMP?

What is the COD shown on her state pension letter?

Presumably it should have been lower if it had been correctly calculated?1 -

Always makes me laugh when they only give you the final figures , a bit of a summary, and then are like "here's how to complain if you dont agree" where's the middle ground of just asking questions ? . It would be VERY easy to be more specific in these letters and e.g. explain that its because post 88 GMP increases at a higher rate than the excess and they've been adjusted or whatever

1 -

This is due to an error in the GMP calculation, nothing to do with equalisation as you would just keep the higher (existing benefit) with that calculation.

Two silver linings are they don’t want the past overpayments back and the drop is likely to be less than one year’s worth of pension increases so after the next increase the pension should be higher than the current pension (admittedly in nominal terms).1 -

Thanks everyone for your comments.

I will look up the COD and GMP figures and post again later.A man walked into a car showroom.

He said to the salesman, “My wife would like to talk to you about the Volkswagen Golf in the showroom window.”

Salesman said, “We haven't got a Volkswagen Golf in the showroom window.”

The man replied, “You have now mate".1 -

Here is her most recent DWP letter dated 8 Feb 2025.

A man walked into a car showroom.

He said to the salesman, “My wife would like to talk to you about the Volkswagen Golf in the showroom window.”

Salesman said, “We haven't got a Volkswagen Golf in the showroom window.”

The man replied, “You have now mate".0 -

For 95% of people they only care about the bottom line, they broadly trust people have calculated it right and wouldnt understand what they were looking at were the calculations shown.PensionsStuff said:Always makes me laugh when they only give you the final figures , a bit of a summary, and then are like "here's how to complain if you dont agree" where's the middle ground of just asking questions ? . It would be VERY easy to be more specific in these letters and e.g. explain that its because post 88 GMP increases at a higher rate than the excess and they've been adjusted or whatever

They are likely obliged to include the dispute process in a similar way to insurers being obliged to tell you about the financial ombudsman.

The issue with talking about calling to ask questions is that people do, often they dont have any actual questions but they feel they are obligated to do so. Calls require staff to answer them and that costs money and many would rather their pension funds were used to pay pensioners not pay for staff. When we had to do a mass mailing to 400,000 annuity customers it cost about £350k in additional call centre staff to be able to deal with the surge in calls that were anticipated.2 -

I notice that her COD is greater than her pre 97 ASP - this indicates that at some stage she was a deferred member of a pension scheme where the GMP revalued in deferment at fixed rather than full rate.

Was the scheme from which she receives this pension the only one with a GMP?

Is there pre and post 88 GMP?

Does the COD figure now require a downwards adjustment?

See https://forums.moneysavingexpert.com/discussion/comment/60448917/#Comment_60448917

re the SERPS scheme.1 -

And how much of that £350k in additional call centre costs could have been saved by some of (or a better version of) a FAQ or similar being provided that answers the most common questions and provides specific details?MyRealNameToo said:

For 95% of people they only care about the bottom line, they broadly trust people have calculated it right and wouldnt understand what they were looking at were the calculations shown.PensionsStuff said:Always makes me laugh when they only give you the final figures , a bit of a summary, and then are like "here's how to complain if you dont agree" where's the middle ground of just asking questions ? . It would be VERY easy to be more specific in these letters and e.g. explain that its because post 88 GMP increases at a higher rate than the excess and they've been adjusted or whatever

They are likely obliged to include the dispute process in a similar way to insurers being obliged to tell you about the financial ombudsman.

The issue with talking about calling to ask questions is that people do, often they dont have any actual questions but they feel they are obligated to do so. Calls require staff to answer them and that costs money and many would rather their pension funds were used to pay pensioners not pay for staff. When we had to do a mass mailing to 400,000 annuity customers it cost about £350k in additional call centre staff to be able to deal with the surge in calls that were anticipated.

0 -

PensionsStuff said:Always makes me laugh when they only give you the final figures , a bit of a summary, and then are like "here's how to complain if you dont agree" where's the middle ground of just asking questions ? . It would be VERY easy to be more specific in these letters and e.g. explain that its because post 88 GMP increases at a higher rate than the excess and they've been adjusted or whateverI think you're over-estimating how easy this would be. The key issue is that there isn't just one potential cause - maybe for one member the problem is that the Scheme put too high a Post88 GMP into payment from GMP age, and GMP increases at a higher rate than excess, but for another member the particular section of the Scheme means that excess increases at a higher rate. Meanwhile for a third member the problem isn't just that the wrong excess / GMP split happened at GMP age, but also in their original retirement calculations. A fourth member had both issues affecting their pension in opposite directions, whilst another member had a transfer-in that didn't get the correct deferred GMP revaluation rate.In theory you could try to output some automated explanation based on what is going on in the underlying models, but a) it would often end up fairly incomprehensible to anyone who didn't already have a good understanding of pensions and b) I wouldn't be comfortable it was working reliably without quite a lot of checking (which is expensive, and money the Trustees are paying to advisors rather than members), and this is one of those cases where an incorrect explanation is likely to be worse than no explanation.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards