We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Switch pension from Aviva to ii

Comments

-

I would rather wait a day or two extra than risk losing £1000 to £2000 of value. Just today the price change is £1300 lower than yesterday.dunstonh said:

Whilst it can take up to 5 days on admin (it doesn't on the plan you have), Aviva would use the unit price at the next dealing point after the request was received even if they were dealing with it days after.dont_use_vistaprint said:Aviva got the request today , they said it takes 5 days. I’m concerned I’m not in control of the u it sell price/timing so have asked them to pause and I will sell to a cash fund first when the price is next at all time high again.

So, effectively, you have added more uncertainty to the unit price.

If you had left it alone, the funds would be with ii by Thursday or Friday.The greatest prediction of your future is your daily actions.0 -

If you are going to re-invest the money in similar assets in II, you have not lost any value as you will buy the funds in II at a lower price. You will lose value if the price goes up again before you have re-invested, but it should not be a big deal over a decades long timeframe.dont_use_vistaprint said:

I would rather wait a day or two extra than risk losing £1000 to £2000 of value. Just today the price change is £1300 lower than yesterday.dunstonh said:

Whilst it can take up to 5 days on admin (it doesn't on the plan you have), Aviva would use the unit price at the next dealing point after the request was received even if they were dealing with it days after.dont_use_vistaprint said:Aviva got the request today , they said it takes 5 days. I’m concerned I’m not in control of the u it sell price/timing so have asked them to pause and I will sell to a cash fund first when the price is next at all time high again.

So, effectively, you have added more uncertainty to the unit price.

If you had left it alone, the funds would be with ii by Thursday or Friday.

The other thing is to be a bit careful about thinking of things in terms of all time high values - when you propose to sell "at the all time high", markets can just as easily continue to go up to more all time highs in the following days (and usually does as from what I've seen, they tend to come in a bit of a clump before retreating back a bit).

Are you going to wait for the market to drop again when you have the cash in II so that you don't lose money, because this is exactly how many investors end up losing part of their long term returns?3 -

Yeah I understand this, the plan is simple sell when it’s on an all time high, which is most of the time but not always. Hold as cash in ii buy something soonish when on a low. This is not rocket science - investing 101 buy low sell high , why would you do anything different?Pat38493 said:

If you are going to re-invest the money in similar assets in II, you have not lost any value as you will buy the funds in II at a lower price. You will lose value if the price goes up again before you have re-invested, but it should not be a big deal over a decades long timeframe.dont_use_vistaprint said:

I would rather wait a day or two extra than risk losing £1000 to £2000 of value. Just today the price change is £1300 lower than yesterday.dunstonh said:

Whilst it can take up to 5 days on admin (it doesn't on the plan you have), Aviva would use the unit price at the next dealing point after the request was received even if they were dealing with it days after.dont_use_vistaprint said:Aviva got the request today , they said it takes 5 days. I’m concerned I’m not in control of the u it sell price/timing so have asked them to pause and I will sell to a cash fund first when the price is next at all time high again.

So, effectively, you have added more uncertainty to the unit price.

If you had left it alone, the funds would be with ii by Thursday or Friday.

The other thing is to be a bit careful about thinking of things in terms of all time high values - when you propose to sell "at the all time high", markets can just as easily continue to go up to more all time highs in the following days (and usually does as from what I've seen, they tend to come in a bit of a clump before retreating back a bit).

Are you going to wait for the market to drop again when you have the cash in II so that you don't lose money, because this is exactly how many investors end up losing part of their long term returns?

I won’t wait a long time. No, I don’t want to be out of the market. But I also don’t want to be selling my S6 units for a bad price and that’s something I should have full control over. But if it sits in a low volatility cash fund for while it’s not the end of the world if I turned on the auto features of the Aviva platform that is exactly where it would be anyway at my ageThe greatest prediction of your future is your daily actions.0 -

They said this is not the case the information you have gave is not true.Sorry, but it is true. Although what you have said is similar to what I have said, except that you assume a gap is present between Aviva receiving the request and confirming all details are present. The reality is that the gap is usually measured in minutes or hours, with the majority of transfers. Not days.They said they use the 5 o’clock price of the day before the day on which they have determined they have all the information from me they need which is not the price that I want.That is not correct. It would lead to price manipulation if it were. Let's say the markets are falling today. Do you really think you could put your transfer in now to get yesterday's closing price?

If I keyed in a transfer now with one of the efficient platforms, it would be keyed into Origo within 30 minutes and Aviva on ex CGNU plans typically accept it or reject it within an hour. If they reject it, it would not trigger the unit price point. If they accept it, it would trigger the unit price point.

The days of having to wait for postal discharge forms to arrive are long gone with the majority of pensions. Only if there were errors in that information (e.g. wrong name, NI or address etc) would the sale be held up as it would be rejected on Origo and not trigger the unit price point. (or if your transfer has triggered anti-fraud checks - Aviva has a good green list and I would expect it to be on it. If you are using obscure direct investments on ii, then it could hold it up).

However, if you were transferring to an old-fashioned scheme that still relies on discharge forms and non-Origo transfers, then a delay in the full information arriving is possible. ii uses Origo, you dont have that.

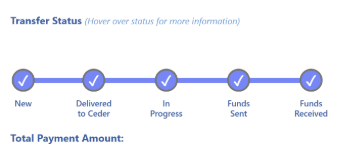

The pic below shows a completed chain on Origo, but it gets accepted/rejected between Delivered to ceder and In progress steps or if something is incomplete or there is an error it won't tick the in progress box. When the 'In Progress' tick appears, that is the point at which the unit price will be determined. And where both providers use Origo, that step is largely automated and can change quickly. But if it sits in a low volatility cash fund for while it’s not the end of the world if I turned on the auto features of the Aviva platform that is exactly where it would be anyway at my ageAre you on the Aviva platform or is it an Aviva Life & Pensions plan? Series 6 is available on both. The Aviva platform is slightly slower than Aviva L&P (ex CGNU). It's staggering how fast Aviva L&P handles transfers nowadays.

But if it sits in a low volatility cash fund for while it’s not the end of the world if I turned on the auto features of the Aviva platform that is exactly where it would be anyway at my ageAre you on the Aviva platform or is it an Aviva Life & Pensions plan? Series 6 is available on both. The Aviva platform is slightly slower than Aviva L&P (ex CGNU). It's staggering how fast Aviva L&P handles transfers nowadays.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

Not sure what you mean by most of the time. According to what I have read, generally stock markets spend more than 90% of their time below the all time high (granted we have had quite a few highs in the last year or so).dont_use_vistaprint said:

Yeah I understand this, the plan is simple sell when it’s on an all time high, which is most of the time but not always. Hold as cash in ii buy something soonish when on a low. This is not rocket science - investing 101 buy low sell high , why would you do anything different?Pat38493 said:

If you are going to re-invest the money in similar assets in II, you have not lost any value as you will buy the funds in II at a lower price. You will lose value if the price goes up again before you have re-invested, but it should not be a big deal over a decades long timeframe.dont_use_vistaprint said:

I would rather wait a day or two extra than risk losing £1000 to £2000 of value. Just today the price change is £1300 lower than yesterday.dunstonh said:

Whilst it can take up to 5 days on admin (it doesn't on the plan you have), Aviva would use the unit price at the next dealing point after the request was received even if they were dealing with it days after.dont_use_vistaprint said:Aviva got the request today , they said it takes 5 days. I’m concerned I’m not in control of the u it sell price/timing so have asked them to pause and I will sell to a cash fund first when the price is next at all time high again.

So, effectively, you have added more uncertainty to the unit price.

If you had left it alone, the funds would be with ii by Thursday or Friday.

The other thing is to be a bit careful about thinking of things in terms of all time high values - when you propose to sell "at the all time high", markets can just as easily continue to go up to more all time highs in the following days (and usually does as from what I've seen, they tend to come in a bit of a clump before retreating back a bit).

Are you going to wait for the market to drop again when you have the cash in II so that you don't lose money, because this is exactly how many investors end up losing part of their long term returns?

I won’t wait a long time. No, I don’t want to be out of the market. But I also don’t want to be selling my S6 units for a bad price and that’s something I should have full control over. But if it sits in a low volatility cash fund for while it’s not the end of the world if I turned on the auto features of the Aviva platform that is exactly where it would be anyway at my age

In fact if you sell at an all time high in Aviva, I’m not sure that this helps you - I wouldn’t be surprised if historically , when you sell at an all time high, the chance is higher that the price will be less if you buy back in a week later.

You might be waiting a while as markets have been falling again today by the way. There is a myth that September and October are bad months for equities which is probably a bit self reinforcing at the start of the month.

Personally I am often tempted to sell at these all time high, but I try to rather look at the gain in my investment over the last year - if it met or exceeded my target, it doesn’t matter if it’s a bit down on the maximum.

0 -

Ignoring the last couple of days, are we not at an all-time high right now? And that is the problem - with the looming debt crisis markets are looking a bit shaky.A little FIRE lights the cigar1

-

Depends what investments you have and the currency - yesterday the S&P 500 lost was down 0.69%. However the dollar strengthened against the pound significantly which cancelled out this loss if your fund is valued in GBP but has a lot of USD shares in it. Vanguard global stock tracker closed slightly below the all time high yesterday in GBP terms. However this is laregly irrelevant if you are transferring, unless you are changing your investment strategy.ali_bear said:Ignoring the last couple of days, are we not at an all-time high right now? And that is the problem - with the looming debt crisis markets are looking a bit shaky.

0 -

Yes because that’s how the fund works. The price changes at 5 o’clock each day so if you put the request in after five you get the following days price - they explained all this to me in great detaildunstonh said:They said this is not the case the information you have gave is not true.Sorry, but it is true. Although what you have said is similar to what I have said, except that you assume a gap is present between Aviva receiving the request and confirming all details are present. The reality is that the gap is usually measured in minutes or hours, with the majority of transfers. Not days.They said they use the 5 o’clock price of the day before the day on which they have determined they have all the information from me they need which is not the price that I want.That is not correct. It would lead to price manipulation if it were. Let's say the markets are falling today. Do you really think you could put your transfer in now to get yesterday's closing price?

If I keyed in a transfer now with one of the efficient platforms, it would be keyed into Origo within 30 minutes and Aviva on ex CGNU plans typically accept it or reject it within an hour. If they reject it, it would not trigger the unit price point. If they accept it, it would trigger the unit price point.

The days of having to wait for postal discharge forms to arrive are long gone with the majority of pensions. Only if there were errors in that information (e.g. wrong name, NI or address etc) would the sale be held up as it would be rejected on Origo and not trigger the unit price point. (or if your transfer has triggered anti-fraud checks - Aviva has a good green list and I would expect it to be on it. If you are using obscure direct investments on ii, then it could hold it up).

However, if you were transferring to an old-fashioned scheme that still relies on discharge forms and non-Origo transfers, then a delay in the full information arriving is possible. ii uses Origo, you dont have that.

The pic below shows a completed chain on Origo, but it gets accepted/rejected between Delivered to ceder and In progress steps or if something is incomplete or there is an error it won't tick the in progress box. When the 'In Progress' tick appears, that is the point at which the unit price will be determined. And where both providers use Origo, that step is largely automated and can change quickly.But if it sits in a low volatility cash fund for while it’s not the end of the world if I turned on the auto features of the Aviva platform that is exactly where it would be anyway at my ageAre you on the Aviva platform or is it an Aviva Life & Pensions plan? Series 6 is available on both. The Aviva platform is slightly slower than Aviva L&P (ex CGNU). It's staggering how fast Aviva L&P handles transfers nowadays.The greatest prediction of your future is your daily actions.0 -

You can avoid paying for trades by setting up a regular investment and then cancel it immediately after the trade has taken place.MetaPhysical said:Something to be aware of when inside II. Trades are normally £3.99. You shouldn't need many to build your portfolio. However, as soon as you want to buy (or sell) 100k or more of something, the trade fee is £40. Be careful of this since I got burnt on three trades that were 150k.

If you want to buy more than 100k, 150k in my example, then split it into two trades - a 90k and a 60k for instance and each will be £3.99.

Your trade would have to be over £one million for it to be worth paying the £40 fee.

Again you don't really need to trade that much, and I'd question anyone if they were regularly trading on what is meant to be their pension fund. Each to their own though.0 -

jaybeetoo said:

You can avoid paying for trades by setting up a regular investment and then cancel it immediately after the trade has taken place.MetaPhysical said:Something to be aware of when inside II. Trades are normally £3.99. You shouldn't need many to build your portfolio. However, as soon as you want to buy (or sell) 100k or more of something, the trade fee is £40. Be careful of this since I got burnt on three trades that were 150k.

If you want to buy more than 100k, 150k in my example, then split it into two trades - a 90k and a 60k for instance and each will be £3.99.

Your trade would have to be over £one million for it to be worth paying the £40 fee.

Again you don't really need to trade that much, and I'd question anyone if they were regularly trading on what is meant to be their pension fund. Each to their own though.How would you do that in the example above where you wanna buy 150K worth of a single fund ? Have you tested it works with these kinds of figuresThe greatest prediction of your future is your daily actions.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604.1K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards