We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Transfer Advice Complaint - Do I have a leg to stand on here?

Comments

-

Glad to see we're still on speaking terms. 8-)dunstonh said:Can I ask you if someone was advised to arbitrarily liquidate their ISA Stock&Shares invesments and then buy them back over a period of weeks or months whether that person would have something to complain about? What is the difference ?a) why would they sell them to buy back identical investments?

b) If they cannot buy identical investments, then yes, it is normal to liquidate the holdings to allow a cash transfer.

You are still ignoring the dates and the fact you probably haven't made a loss.

Lets help you with that:

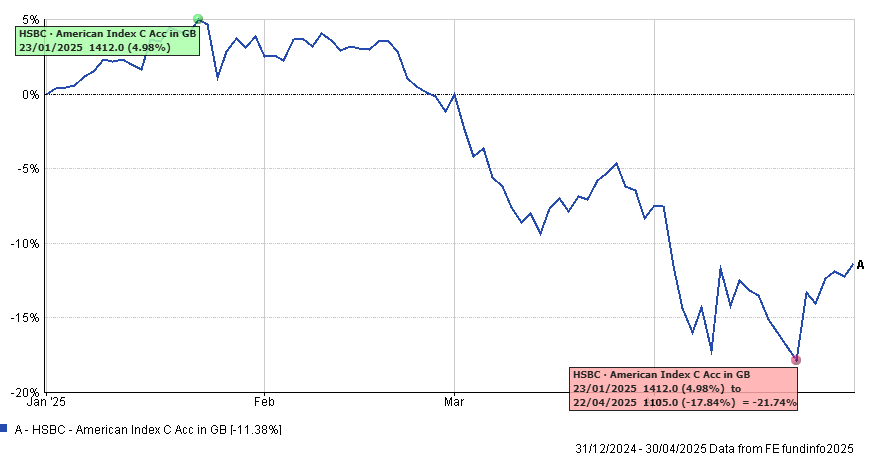

The chart shows a US equity fund that effectively tracks the S&P500. It peaked 23rd January. So, between then and the end 31st March, it was already down 12.68%.

You say you sold out in early April and didn't reinvest to weeks later. So, below shows selling out on 4th April and the loss that continued whilst you were out of the market to rejoin "weeks later".

From peak on 23rd Jan to trough on 22nd April, the loss was 21.74% and you were out of the market for around 7% of that loss.

You are fixated on Trumps liberation day of 2nd April but you can see that the majority of the winter/spring drop had already happened by Liberation day.

Give us the sale date on the existing pension and the purchase date on the new one and I will use those dates.

Sale April 4 (I've just checked) and purchase I'm still not fully in.

I got control on the other side (the new platform) on April 30. I had some trouble getting through their telephone queueing system (I didn't know it would be phone only) but eventually managed to call every day for the subsequent 2 weeks dripping in 200K. Over the subsequent months I've put the rest except 150K still in a cash fund.

My transfer value was 540K (possibly irrelevant), the value just before transfer was 520K. The amount transferred was 463K (inclusive of your colleagues' "modest" fee).

You ask why would anyone sell and then buy identical (or close to identical) investments? I think they wouldn't. But my question to you is what is the risk of doing that? And if there is a risk shouldn't I have been told about it as that is what the mechanics of the transfer involved? You will say "no" of course or that it doesn't matter and you might be right. I don't know.

0 -

You do keep banging the same old drum and resolutely refusing to take on board the crucial point: you were going to go ahead whatever anyone said. You wanted to transfer and you weren't going to listen to any of the arguments against doing so.

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!4 -

Sale April 4 (I've just checked) and purchase I'm still not fully in.I got control on the other side (the new platform) on April 30. I had some trouble getting through their telephone queueing system (I didn't know it would be phone only) but eventually managed to call every day for the subsequent 2 weeks dripping in 200K. Over the subsequent months I've put the rest except 150K still in a cash fund.Ok, so lets look at what happened from January to 4th April with US equity. -14.35%. So, the bulk of the loss had occurred before transfer.And what happened between 5th April and 30th April: +3.47%

So, in the scheme of things, the difference was small in respect of US equities. The decision to phase back in was a bad one in hindsight. Personally, I don't phase as statistically you are more likely to end up in a worse position. If you cannot handle the volatility of a risk profile, then phasing doesn't change that. It just delays the inevitable when the next negative period comes along.You ask why would anyone sell and then buy identical (or close to identical) investments? I think they wouldn't. But my question to you is what is the risk of doing that? And if there is a risk shouldn't I have been told about it as that is what the mechanics of the transfer involved? You will say "no" of course or that it doesn't matter and you might be right. I don't know.You are right, they wouldn't sell and buy identical. They would use inspecie transfers. But you cannot do that if the assets you hold are not available to the new pension (or ISA etc). A platform to platform transfer can use in-specie with most funds. An insured pension/fund doesn't have in-specie available.

It would be worth your revisiting the recommendation report and checking the risk warnings. The report writing software I use automatically adds a risk warning about being out of the market for a period while a transfer takes place.

Here it is:- The underlying investments may not be invested for a short time while the switch is taking place. During this time, you will not benefit from any increase in their value, but neither will you be disadvantaged if their value falls.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.6 -

I will have a thorough read through again but I'm pretty sure I would have remembered such a warning.dunstonh said:Sale April 4 (I've just checked) and purchase I'm still not fully in.I got control on the other side (the new platform) on April 30. I had some trouble getting through their telephone queueing system (I didn't know it would be phone only) but eventually managed to call every day for the subsequent 2 weeks dripping in 200K. Over the subsequent months I've put the rest except 150K still in a cash fund.Ok, so lets look at what happened from January to 4th April with US equity. -14.35%. So, the bulk of the loss had occurred before transfer.And what happened between 5th April and 30th April: +3.47%

So, in the scheme of things, the difference was small in respect of US equities. The decision to phase back in was a bad one in hindsight. Personally, I don't phase as statistically you are more likely to end up in a worse position. If you cannot handle the volatility of a risk profile, then phasing doesn't change that. It just delays the inevitable when the next negative period comes along.You ask why would anyone sell and then buy identical (or close to identical) investments? I think they wouldn't. But my question to you is what is the risk of doing that? And if there is a risk shouldn't I have been told about it as that is what the mechanics of the transfer involved? You will say "no" of course or that it doesn't matter and you might be right. I don't know.You are right, they wouldn't sell and buy identical. They would use inspecie transfers. But you cannot do that if the assets you hold are not available to the new pension (or ISA etc). A platform to platform transfer can use in-specie with most funds. An insured pension/fund doesn't have in-specie available.

It would be worth your revisiting the recommendation report and checking the risk warnings. The report writing software I use automatically adds a risk warning about being out of the market for a period while a transfer takes place.

Here it is:- The underlying investments may not be invested for a short time while the switch is taking place. During this time, you will not benefit from any increase in their value, but neither will you be disadvantaged if their value falls.

Looking at the s&p, on April 4 it was 5074 and by April 30 it was 5569. I make that a 9.7% rise.

Do you think the yes/no result of the Advice is relevant ?

0 -

While dunstonh has provided charts for a S&P500 tracker, that might not correctly reflect your DC funds' movements.In your previous thread you stated:The DC pension is invested in certain public funds whose values are known and change daily (when the markets are open).Do you remember (or have a record of) exactly which funds these were? It might be that they moved differently back in the early months of 2025?N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.0 -

I think the popular phrase the kids use is FAFO and you are in the FO phase………2

-

Well that's me told thenMyRealNameToo said:

Hu? You've been here more than 20 minutes havent you?artyboy said:Might as well close this thread now, as I suspect MSE doesn't condone blatant greedy ambulance chasing activities like what the OP appears to be proposing.

This whole site was founded on arguing your way out on loopholes and technicalities.

Seriously though, you go over to the property board and start a thread on loopholes and technicalities to avoid care home fees by giving your house away to your kids... that's the sort of ballpark we are in here.0 -

You're right! I'll do the maths tomorrow but looks more like a 5% growth rather than 9.7.QrizB said:While dunstonh has provided charts for a S&P500 tracker, that might not correctly reflect your DC funds' movements.In your previous thread you stated:The DC pension is invested in certain public funds whose values are known and change daily (when the markets are open).Do you remember (or have a record of) exactly which funds these were? It might be that they moved differently back in the early months of 2025?0 -

Does that warning not underplay potential losses that could occur if transferring when markets are very volatile?dunstonh said:

It would be worth your revisiting the recommendation report and checking the risk warnings. The report writing software I use automatically adds a risk warning about being out of the market for a period while a transfer takes place.

Here it is:- The underlying investments may not be invested for a short time while the switch is taking place. During this time, you will not benefit from any increase in their value, but neither will you be disadvantaged if their value falls.

0 -

Looking at the s&p, on April 4 it was 5074 and by April 30 it was 5569. I make that a 9.7% rise.But you are a UK investor. The US dollar fell against the Sterling, so UK investors haven't seen that rise. Only those that are currency hedged (and most dont).

During that period of 5th April to 30th April, all equities were up across the usual countries/regions in a portfolio except emerging markets. Bonds & gilts were slightly down or flat. Cash would be positive but the amount would be based on the interest rate of your cash account.Does that warning not underplay potential losses that could occur if transferring when markets are very volatile?The risk of adding many qualifying statements to risk warnings is that people stop reading them, as they are too long and unwieldy. A statement of fact that is short and simple to understand is best.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards