We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage Complaint - Private recording, can I share transcript and/or audio with the FOS?

Comments

-

On what basis?MWT said:plays said:So, anyway, am I legally allowed to share the recording with the FOS as a private individual or only the transcript, why I believe I can do?Very generally, you cannot share an undisclosed recording with a 3rd party, without the consent of the other party on the call.Same goes for the transcript...

Certainly in civil court you can and the judge will make their own decision on what weight is placed on it if the counter party object on the basis of it being recording without explicit consent.

It's never been an issue I've come across with the FOS as we've always recorded calls and routinely submitted them to the FOS when the allegations relate to a conversation on the phone. Normally it would be in the format of a transcript rather than audio file but thats more in sympathy for the person at the FOS as its much easier to search in a text file for keywords if you are looking for one key detail rather than having to listen to a long call to just hear if commission was or wasnt mentioned or whatever the point is around.0 -

Yeah. You have to make clear exactly what is required and by when. It's a useful option to have though, especially in a rising rate period.Sarsibob1 said:I guess the risk is though that if the broker reserves the rate in say May, client finds in say July then the broker has to get a mortgage offer out within the remainder of the 90 days timescale which could only be 4 weeks or so. At the point of aip the client doesn't have a house - the time taken to find one is a bit of a 'how long is a piece of string' situation. If say there is a short timescale then if that isn't managed (as at the time of rate increases lenders are busy, queries on underwriting or need an employers reference or no valuers etc) the client could then be in a worse position than if they had just reserved the rate at the point of application - in this case it was still around 2% fixed for 5 years. - this was in 2022 when rates started going up sharply. Had the client not got his mortgage offer within 90 days from aip then that would have probably been a bigger complaint as suddenly the rates available are 3% plus

TBH we can usually get from application to offer in less than two weeks.I am a mortgage broker. You should note that this site doesn't check my status as a Mortgage Adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice. Please do not send PMs asking for one-to-one-advice, or representation.0 -

Update.

Letter of intent to take it to small claims court.

Interesting response 😁

For the record, we reject your claim for £4,996 in its entirety. As such, if you do wish to take this matter to the County Court, we would defend our position on the following grounds:

1. Incorrect Legal Entity and Lack of Liability

The mortgage advice and application in question occurred in February 2022. The following points are important to note:

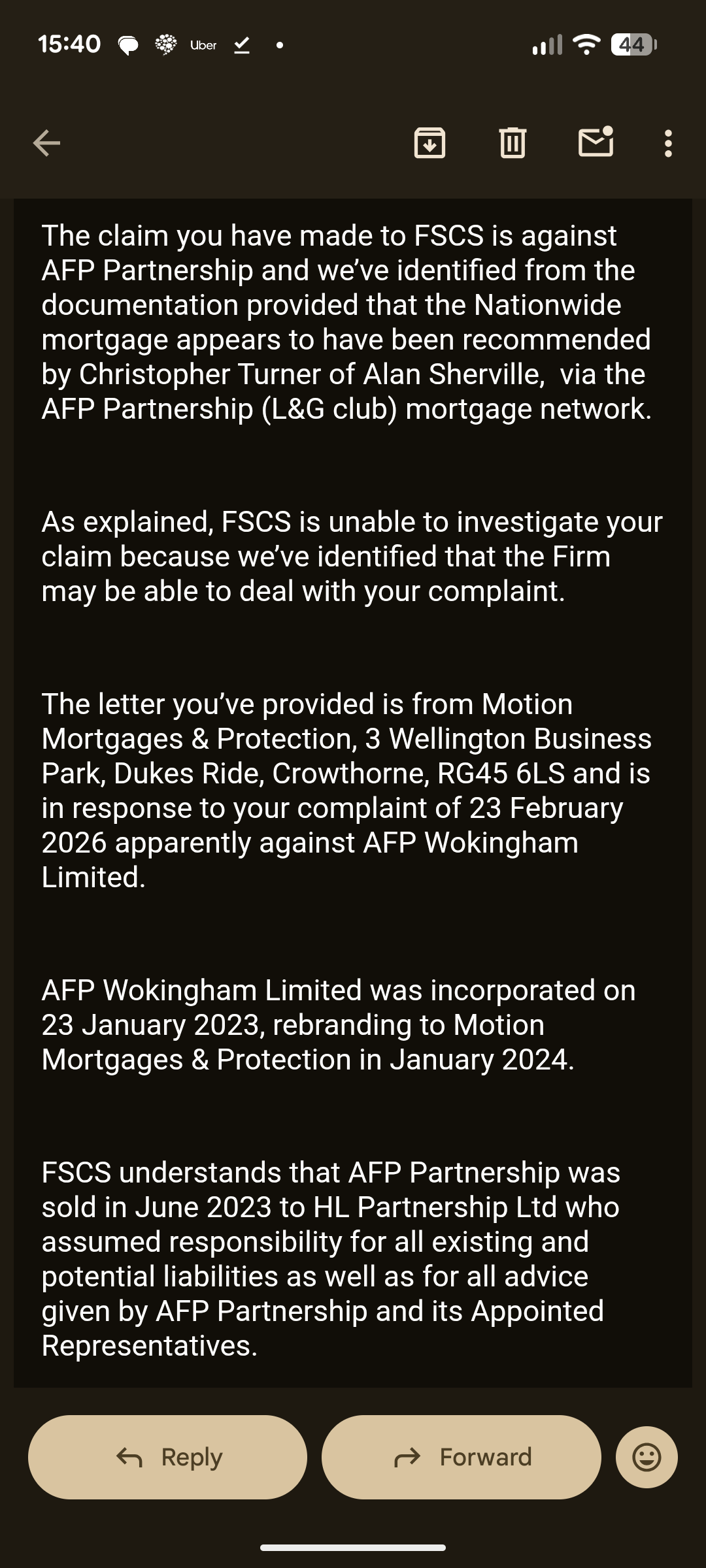

At the time of the advice, AFP Wokingham Ltd did not exist. The company was incorporated after your mortgage was arranged.

The business you dealt with was owned and operated by A*** S****, acting as a sole trader, under the AFP Mortgage Network.

AFP Wokingham Limited took over the client bank and goodwill of the previous sole trader business. No novation or transfer of liabilities occurred.

AFP Wokingham Limited does not own the previous sole trader business and has not assumed any historic liabilities for transactions arranged before the company began trading.

Neither myself D***H****, nor AFP Wokingham Limited provided the advice or had any part in the management of your case.

On that basis, AFP Wokingham Limited is not the correct legal entity in respect of the advice provided in

February 2022. However, if you still believe that AFP Wokingham Limited is responsible, I would encourage you to show evidence of a contractual relationship between yourself and AFP Wokingham Limited.

2. Independent Reviews

The substantive elements of your claim, specifically the 1.59% vs 1.94% interest rates, have been examined by our network, HL Partnership Limited (HLP), and the Financial Ombudsman Service (FOS).

…

- Response to Data Protection Allegations

You allege that data has been "withheld" or "doctored" in violation of Section 173 of the Data Protection

Act. We provide the following clarifications:

Verified Disclosure: All data held by this firm has been provided to you. This disclosure was also

facilitated and verified by HLP, which forwarded the records to you on our behalf.

Forensic Evidence: We have provided the Excel document which you have challenged the

authenticity of. The metadata and version history demonstrate that the records supplied have

not been altered or deleted.

Information Commissioner: You have already made these allegations to the Information

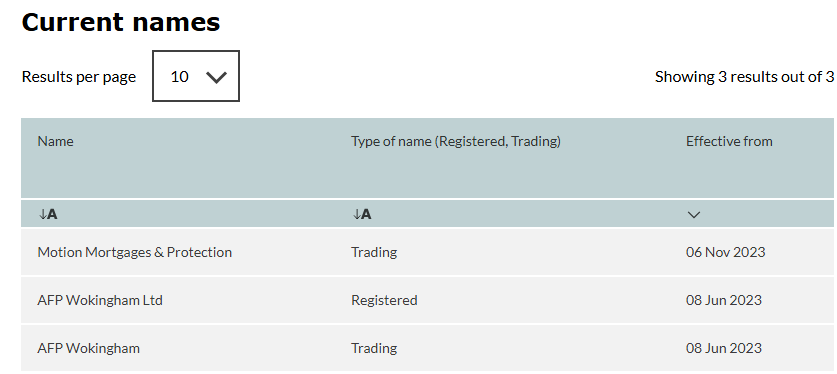

Below is a linkage of trading names

AFP Wokingham in 2022 which worked on my mortgage, part of AFP Group Ltd I believe

Looks like AFP Wokingham became part of AFP Wokingham Ltd in 2023

This then became part of HL Partnership Ltd in June 2023 perhaps

AFP Wokingham rebranded as Motion Mortgages & Protection later on

Anyway A**** S**** is still connected as a director, so is DH now trying to say he is the responsible and liable party? Some colleague that is!

I also find it quite amusing that he has admitted he had no involvement on my case and the only two people who worked on my case left two-three years beforehand yet compelled to give evidence and a version of events to the FOS despite having no phone recordings or alleged case notes and claimed I actioned certain things 😁

Does the below apply?

Under the Financial Services Act 2012 and subsequent Financial Conduct Authority (FCA) rules, a successor firm—such as a mortgage broker that takes over the business, assets, or client base of a predecessor—can be held liable for mis-selling or negligence committed by the predecessor firm.

Financial Conduct Authority | FCA

Financial Conduct Authority | FCA

+2

The FCA strengthened rules to assist the Financial Services Compensation Scheme (FSCS) in handling claims where the original firm has gone out of business, ensuring that successor firms cannot easily evade liability for prior negligent advice or actions.

Financial Conduct Authority | FCA

Financial Conduct Authority | FCA

Key Aspects of Successor Liability for Mortgage Brokers:

Definition of Successor Firm: The FCA generally considers a firm a "successor" if it assumes the liabilities or takes over the business of a predecessor, especially if it continues to operate in the same market, such as mortgage mediation.

Liability Transfer: If a mortgage broker acquired the client list, business name, or key personnel of another broker that mis-sold mortgages (e.g., in the 2004–2009 interest-only era), the new firm may inherit the responsibility to handle complaints and pay redress.

FCA Rule Changes (Post-2012): Changes made by the FCA, including those following CP15/40 (finalised in PS16/14), clarified how compensation rules apply to successor firms to ensure consumers can still receive compensation for negligent advice.

Complaints Handling: If a mortgage broker has gone out of business, complaints can often be directed to the successor firm or the FSCS 0

0 - Response to Data Protection Allegations

-

Effective from June 2023…

I received a complaint in 2017 I think. It was for a Limited company with the same name as mine. However the complaint was from a transaction in 2012. They closed the business in 2013 or 14 I think. I registered the limited company name in 2016. In my case, I had nothing to do with the previous owners in any regards, we are from opposite ends of the country. But the principle is the same, your complaint is with a business that no longer exists not this new one.

However, if the old business was a sole trader, you can take the owner of the business to court. A limited company is its own legal entity. A sole trader is just a trading name of that person. So even if the company has closed down, the person would still be fair game I believe. This is one of the benefits of going limited for a business.

They are correct I believe in that if you go after the limited company, and that company never even existed at the time, your case will be thrown out as it would have been physically impossible for a company that did not exist to make a mistake.

Type in the name of the business on your mortgage offer into the FCA register. If it is/was a sole trader then you would need to take the person to court. You might also be able to include the network in the claim if there was one but I am not sure on that. You potentially need legal advice.

Dont get fixated on trying to take it to court at any cost, you have made a mistake here and they could have just turned up to court and watch you waste your money and embarrass yourself by ignoring your letters.

But just to be clear, I still believe that you are throwing good money/energy after bad.

I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.1 -

AFP Wokingham is actually the old name, FCA shows a clear linkage between Motion Mortgages & Protection

It originally fell under a different Ltd company at the time, AFP Partnership Ltd - which I believe HL Partnership Ltd took over the network of firms beneath

Their own website even states at the top :

"Hello, if you're looking for AFP Wokingham, you've come to the right place. In January 2024, we rebranded the business to MOTION Mortgages & Protection. It's a new name but the same great service so don't hesitate to get in touch."

So the company appears to be the same. It's not a limited company, it's the company which is part of the wider AFP Wokingham Ltd which also falls under the Principal firm HLP Ltd for which I am not intending to sue, it's the individual firm which isn't on Companies House and is still active. So there is no intent by me to sue any Limited Company.

If I won my FOS case, would they have then said they would not pay up? I have another open case with the FOS regarding an income protection complaint with the same firm. So I've asked the FOS who is the liable party on that one

Anyway small claims court fee is over £200 so I'll have a judge review because I will call a witness summons to the director for what I perceive to be misleading statements which can be given to the FOS without legal consequences, but in a civil arena I'm willing to see if he'll put himself in contempt of court regarding the internal complaint notes - for which the FOS eventually provided to me so I can prove these were withheld by the firm which breaches the Data Protection Act after they denied having any

Alternatively i'll get confirmation if to take it to the FSCS and that'll still give me time for the 6 year time limit for small claims court

0 -

Look at Debenhams, Comet or Woolworths.

All of those business names still trade. But none of those original businesses exist.

This is the same principle.

The new business has used, maybe even bought the name but not the liability.

I imagine your claim would be against AFP partnership ltd and possibly also HL Partnership ltd (HLP). If AFP partnership limited (the one that did your mortgage in 2022) no longer exists, then you probably only have HLP to go after. But this is all getting a little messy and complex so I think you are best taking legal advice.

I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0 -

AFP Wokingham is actually the old name, FCA shows a clear linkage between Motion Mortgages & Protection

That doesn't mean they are responsible.

I took on an adviser who used to have his own business. His client bank was novated to mine and we set up a trading style similar to his old name (basically minus the Ltd) and I have no liability whatsoever for anything that he did under his old limited company. The FCA register would show him as being linked to a similar name but that is all.

Under the Financial Services Act 2012 and subsequent Financial Conduct Authority (FCA) rules, a successor firm—such as a mortgage broker that takes over the business, assets, or client base of a predecessor—can be held liable for mis-selling or negligence committed by the predecessor firm.

I suspect you have used AI with the +2 indicating sources, but it's giving an incorrect interpretation. Try a different AI model (ideally not a free one, as they frequently hallucinate).

The Financial Services Act 2012 mainly created new regulatory and enforcement structures (FCA, PRA, Part 7 offences etc.); it does not contain a general rule that a “successor firm” automatically becomes liable in civil law for the predecessor’s mis‑selling. In other words, the Act itself is not the source of a blanket principle that a purchasing mortgage broker is liable for all historic negligence of the seller.

Under the post‑FS Act 2012 regulatory regime and FCA rules and guidance, a firm that acquires another firm’s business, assets or client bank may, depending on the terms of the transaction and any undertakings to the FCA, assume liability for some or all of the predecessor firm’s mis‑selling or negligence; additionally, the FCA can expect the acquiring firm to deal appropriately with any historic detriment affecting the customers it has taken on.

If the new firm bought the shares in an authorised firm, they normally inherit that company with all its historic liabilities, including redress, as a matter of company and contract law rather than any special FCA rule. By contrast, they only bought the client bank (the list of clients and associated income), there is no automatic rule that they take on the seller’s past advice liabilities; the position is more open and depends on the contractual allocation of responsibilities and any regulatory undertakings. i.e. if the FCA states that the new company is effectively phoenixing from the old without any valid reason for doing so, then they can insist that the new company takes on the liabilities of the old as a condition of their FCA permissions.

Sole traders and partnerships carry lifetime liability. Limited companies carry limited liability (hence limited)

It originally fell under a different Ltd company at the time, AFP Partnership Ltd - which I believe HL Partnership Ltd took over the network of firms beneath

You have to take the legal entity that is responsible to court.

Companies house clearly shows an incorporation date of 23/01/2023 and the FCA register shows start date of 08/06/2023. It also shows HL partnership as a connected firm but only from 08/06/2023.

In most cases, the network takes on liabliity for its member firms and in this case, the legal letter response confirms that HL Partnership reviewed the complaint.

AFP Wokingham is actually the old name, FCA shows a clear linkage between Motion Mortgages & Protection

It originally fell under a different Ltd company at the time, AFP Partnership Ltd - which I believe HL Partnership Ltd took over the network of firms beneath

I can see that AFP Wokingham had several trading styles, including Motion but all are effective after the date in question.

It also shows that the Principal firm is HL Partnership Ltd but again, from 2023.

AFP Wokingham is actually the old name,

AFP Wokingham was only effective until 19/09/2016. Going by the FCA register, I haven't found any AFP Wokingham references after that date. (apart from the limited company set up later, but that is not the same as AFP Wokingham). There seems to be a gap between 2016 and 2023.

However, the FCA register is notorious for being hard to track history and can lead to gaps and a risk of incorrect assumptions.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

right confirmation from the FSCS that HL Partnership Ltd are liable, for assuming all responsibility and advice given at the time. Court fee £280 or so? Worth it if it proceeds to court stage if they don't wish to settle

Also, L&G confirmed to me that in writing that the commission payment from the Income Protection product (separate to the mortgage) was paid to the master agency account of HL Partnership so clearly there is a linkage if they're taking commission from contracts in 2022. I have actually requested the CRM pages from L&G - failed to spot that in previous correspondence but doesn't disguise the fact they're refusing to give their internal CRM notes and workflow but also HLP admitted something which contracts MM&P's pre-action response.

I'll have them and Motion Mortgages & Protection as both defendants. They used the liability excuse not to answer any of the direct complaints I had noted to the ICO - who I know won't consider this as new evidence to investigate - but I can ask them direct questions in court as to their claims about my data not being accessible in regards to case notes and workflow 🙂

0

0 -

If AFP partnership limited (the one that did your mortgage in 2022) no longer exists, then you probably only have HLP to go after. But this is all getting a little messy and complex so I think you are best taking legal advice.

This is what I said 2 weeks ago.

HLP are a bigger firm (a network) that allow smaller firms to trade in financial services. If a complaint comes in to one of the smaller firms within the network it would be the network (HLP in this case) who deal with it.

Going off past posts, it looks like HLP have already rejected your complaint as have the FOS.

Your last option now is to go to small claims against HLP. I dont see them settling outside of court. If they thought they were in the wrong, they would have settled before allowing you to go to the ombudsman as it costs them £500 for the FOS to look into it.

They seem very adamant that they are not in the wrong.

I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0 -

Yes, but thankfully I have direct correspondence from Nationwide contradicting their claims regarding the product fee being non-refundable - which they claimed as to why they didn't apply it along with false claims I didn't want to pay it up front which would have secured the lower rate in question. I initially had my complaint upheld by the initial case handler but the ombudsman overturned it without any facts or basis, that I apparently always wanted to add the product fee to the loan balance despite there being no mortgage notes on the forms I checked after the DSAR nor emails confirming or instructing this under MCOB rules, and clearly I was able to pay it up front

- sizeable savings on the bank statement

- the advisor himself asked if I wanted to increase the deposit size by£12.5k so evidently I could afford the £999 up front

- This seems to have gone above the ombudsman head who I'm fairly certain copied/pasted what HLP sent without fact checking considering that it clearly stated on the KFI itself that the product fee was refundable and provided emails from Nationwide detailing it more

No calls, no emails etc, even evidence I was clearly worried about the rate change on the day it was applied and wanting to secure the lower rate

I don't know why they seem so adamant and seem to be giving conflicting statements on liability

(Image removed by Forum Team)

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards