We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Mortgage Complaint - Private recording, can I share transcript and/or audio with the FOS?

Comments

-

Last week I posed a new client.kingstreet said:

Yes. I expected you to say Nationwide.plays said:

Lender was Nationwide. They're going to help me as I am a vulnerable customer with a chronic illness.kingstreet said:27Tec is a sourcing system. It can be linked to a CRM like 360 so data is pulled through to feed the source.

Back to the substantive issue. As many lenders require a full application to be submitted before a rate can be reserved, which lender was involved here?

The rate can be reserved at the product reservation stage without the need to submit the FMA, hence why the broker is trying every sly little trick in the book to fabricate a series of events for which the FOS has not fact-checked.

Once a DIP has been done, a product can be reserved with a full application not immediately submitted; but a product fee would have to be paid, if add to loan wasn't chosen. There is then a three month period in which an application can be submitted but the offer must be issued within that period to preserve the reserved rate.

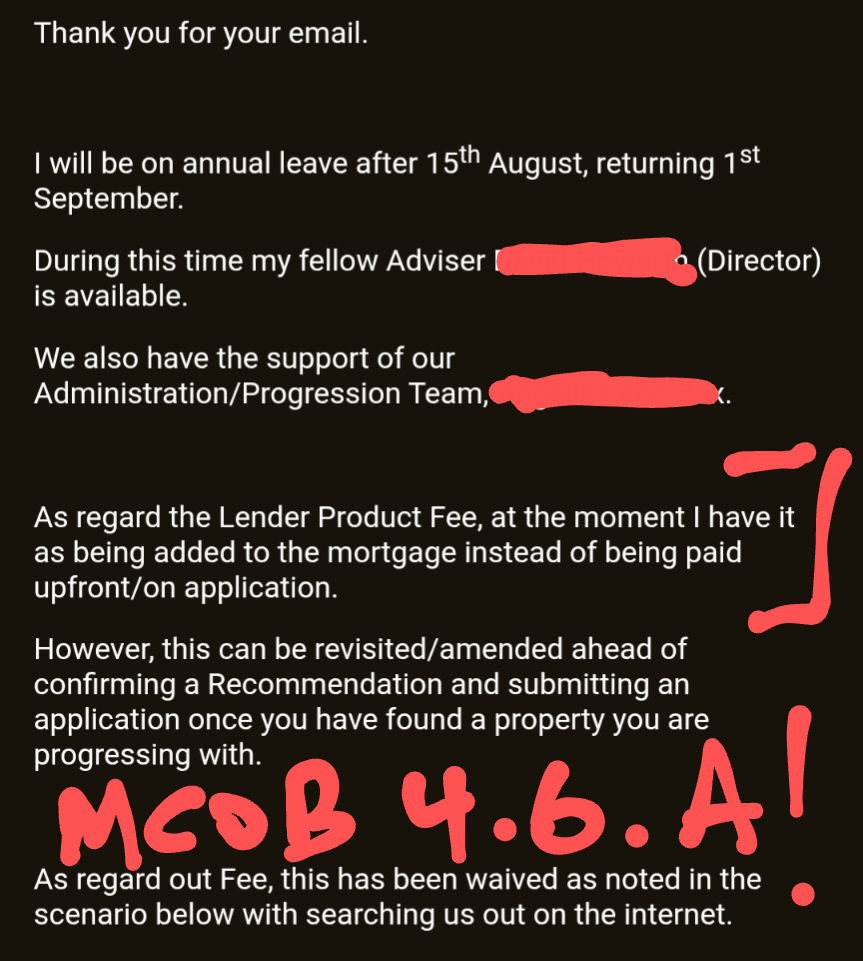

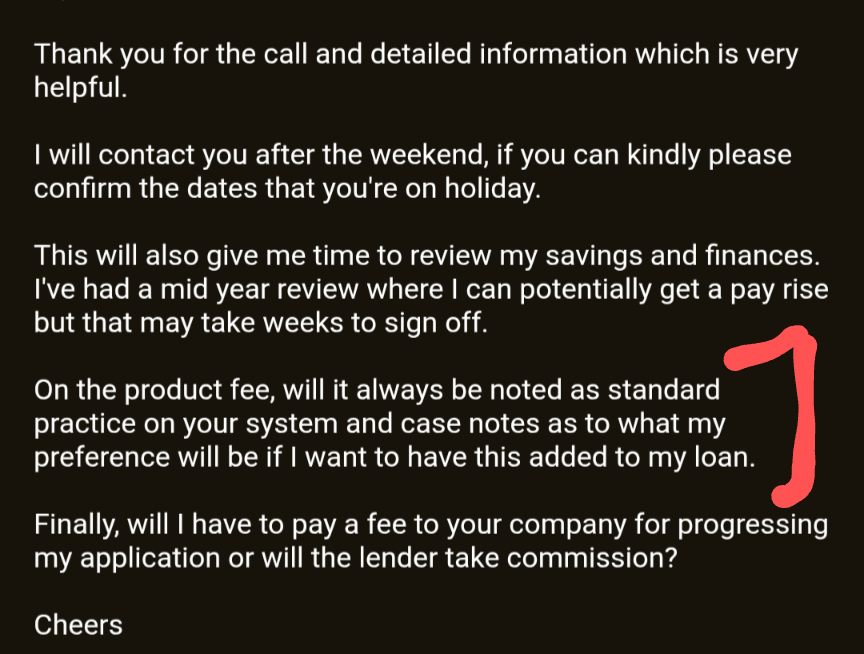

I carefully worded my responses and I have evidence they add the product fee without customer acknowledgement nor consent, thereby breaking MCOB rules unless I have misinterpreted it. I am more knowledgeable on FCA guidelines based on my 13 years within asset finance"A firm must not undertake any action that commits a customer to an application for a regulated mortgage contract where a fee or charge of any kind (receivable either by the firm or another party) is to be added to the sum advanced under the regulated mortgage contract, unless the customer has made a positive choice to add the fee or charge to the sum advanced"

This was the main basis of their argument in my case claiming I consented at the DIP stage

Well as I said I don't trust the FOS but

0

0 -

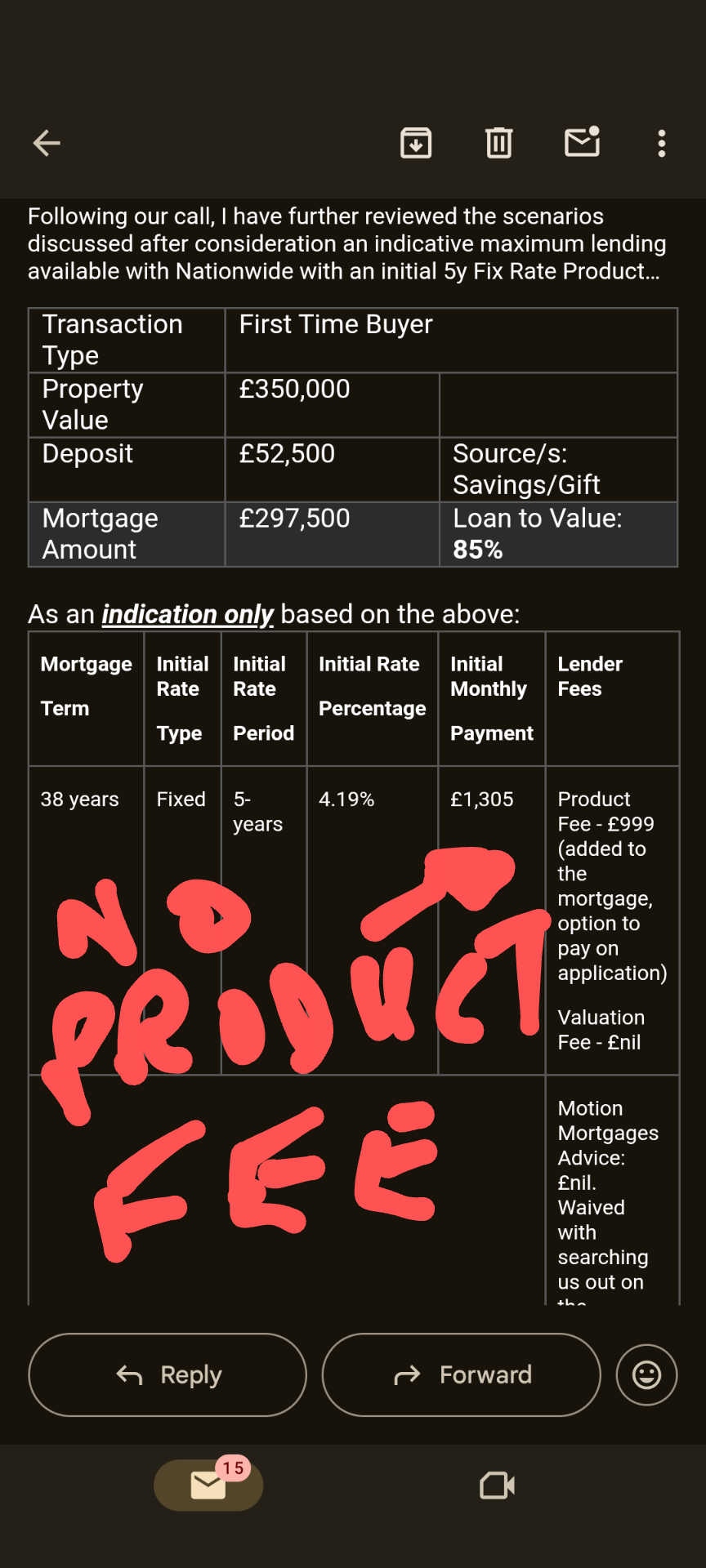

IIRC it was April 2014 when automatically adding a fee to the loan was outlawed. Here's how we deal with that for new clients today. This was at the point we're preparing the application;-

"Please find attached final illustrations for two year and five year fixed rates showing rates, fees and monthly mortgage costs. Products with lender arrangement fees have been illustrated as these offered best value for money.

If you would like to add the product fee to the loan, please let us know and we will produce and forward an updated illustration. Interest will be charged on the fee so it is best repaid sooner rather than later once you’ve moved."I am a mortgage broker. You should note that this site doesn't check my status as a Mortgage Adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice. Please do not send PMs asking for one-to-one-advice, or representation.0 -

They have not committed you to paying the fee. Under the first paragraph you highlighted, it says they can revisit it.

Im not defending the firm here btw. I am just sitting on the fence rather. But if they are trying to get away with a mistake, I am amazed they are taking it so far. It would have been easier to just agree to cover the difference rather than putting half the story in a spreadsheet etc.I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0 -

The main group is an AR of the broker I dealt with.ACG said:They have not committed you to paying the fee. Under the first paragraph you highlighted, it says they can revisit it.

Im not defending the firm here btw. I am just sitting on the fence rather. But if they are trying to get away with a mistake, I am amazed they are taking it so far. It would have been easier to just agree to cover the difference rather than putting half the story in a spreadsheet etc.

So if we're talking about the main group who is the AR, their last accounts on Companies house for 2023 read £3,825,034 in profit. As a minimum lost out on £2,400 for the 5 year fixed period, and £1,100 for interest (assumption of same rate) for the whole term for the product fee.

I also found an old email where another estate agents I liaised with actually carried out an affordability check via my brokerage for an offer on a house I didn't proceed with in the end, based on a £100k deposit, so if they claim they were worried I couldn't afford £999 to pay up front then they'll have a lot of explaining to do.

This affordability check has not been provided to me and i've informed the main group overseeing this i will take this as another breach of data protection laws if they fail to provide it.

0 -

I think you may have it wrong.

You normally have the company at the top - which is directly authorised. (this is who would/should have been dealing with the complaint originally).

You might then sub companies who are the ARs.

Its the AR who would be liable for the this money (if they are in the wrong) rather than the main company.

The only way £100k is relevant is if the deposit was £99k and the fee £1k... If the deposit was £100k and the fee £1k then you are £1k short. Also, if that was a while ago, they may not retain it. I speak to people and if no advice was provided, after a period of time I delete their files.

I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0 -

So the KFI was emailed to me after the point of them submitting the FMA, however, it was an 11 page document which I could only access on my phone in small print and during working hours and I couldn't send it to my work laptop due to data security issues and not only because of problems accessing my personal account but sending non-related work files to my work address which would have prompted an internal IT response.kingstreet said:IIRC it was April 2014 when automatically adding a fee to the loan was outlawed. Here's how we deal with that for new clients today. This was at the point we're preparing the application;-

"Please find attached final illustrations for two year and five year fixed rates showing rates, fees and monthly mortgage costs. Products with lender arrangement fees have been illustrated as these offered best value for money.

If you would like to add the product fee to the loan, please let us know and we will produce and forward an updated illustration. Interest will be charged on the fee so it is best repaid sooner rather than later once you’ve moved."

They're claiming because I said nothing then I must have agreed to the product fee being added but I have written evidence from my lender and funnily enough from the FOS of my vulnerabilities when dealing with me and my inability to read long financial documents due to severe fatigue and concentration issues and I'll have a GP Letter to back-up these in writing as my chronic illness affected me since 2017.

Also, my financials were discussed on the day of the rate change, once the 5pm deadline to secure the rate was missed. At no point did he mention the product Fee and by stating that the mortgage amount was £250,000, his follow-up email without specifying a breakdown did amount to a mortgage amount of £250,999.

From: BrokerSent: 10 February 2022 17:00To: MeSubject: RE: Mortgage applicationHi ******,Thanks for this.Is that *Estate Agents in Town*?And what *Solicitor* branch is it?I am assuming you are aiming to use £250,000 mortgage and £65,000 deposit?

------------------

From: MeSent: 10 February 2022 17:05To: BrokerSubject: RE: Mortgage applicationHi *****,Providing if you feel Nationwide rates are fine despite the increase then £250k mortgage with £65k deposit. Happy to discuss if you feel there are better rates available.

......

----------------From: BrokerSent: 10 February 2022 17:40To: MeSubject: RE: Mortgage applicationHi ******,The rate increases would be quite punitive, the rates are going up to 1.94% however there is now difference between the 75% and 80 LTV Rates so wouldn’t be any point increasing the deposit to beat the threshold.We might be able to press ahead with your existing rate that we dipped at if we maintain the same LTV ratio. This would mean a deposit of £78,750.Is this something you could make work or would you prefer to use a lower deposit?The monthly payments on the £65,000 deposit would be approx. £823.20. If we can keep your existing rate but used a £78,750 deposit, this would be approx. £736.57 per month. Over the 5 year fixed rate this is a sizeable difference of almost £5,197.80, but you have to remember, some of this saving will be purely because you are borrowing less money to begin with.In terms of alternatives, no one can match that lending even at 75% LTV. Santander come close at 75% LTV with £230,500 and they do have a better rate than the new Nationwide rate, but if we are going to the 75% anyway we may as well try to proceed on the Nationwide DIP we already have.I hope that makes sense.0 -

So if we're talking about the main group who is the AR, their last accounts on Companies house for 2023 read £3,825,034 in profit. As a minimum lost out on £2,400 for the 5 year fixed period, and £1,100 for interest (assumption of same rate) for the whole term for the product fee.You cannot tell the company position from companies house. I only had a £90 profit on my trading company. The profit was transferred to the holding company.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

oh well FOS didn't uphold my case despite finding clear lies from the Broker regarding that product fee not being refundable and apparently my vulnerabilities clearly noted with NHS and the FOS themselves i had difficulty reading financial documents...the same ombudsman who led a conference about Consumer Duty and Vulnerable customers, saying I would have no problem reading financial documents

Guess it didn't help I mocked his abilities as well")

Decision is so long winded, funnnily enough he took my advice to cut down the responses after having 11 pages before. link available for a week and he ignored the clear contradictions made of the product fee not being refundable ...nice

https://www.filemail.com/d/oeezoqtjfiqdlau

Small claims court might the path for me. On the ICO complaint, that was made two weeks ago

0 -

Vulnerabilities noted with the NHS is of not help to your argument. Neither is it with the FOS as that would have only happened after the event.

I still think there is more to this. I cant get past the fact that I think it is unlikely a firm would like to the FOS for £2,400. They also have a network who are monitoring everything. If they were caught out to be lying, they could be stuck off.

Also you mention you are vulnerable, I also find it hard to believe the FOS would not be taking that seriously.

I am not saying you are wrong, but something does not feel right about your version of everything. The complain alone would cost them £500, it would also need disclosing to the FCA and insurers down the line. So for £2,400 you would think they would just pay you off to get rid of you - unless they genuinely believe their version is watertight.

Consider that if you go down the small claims route, it will start costing you money and there will be more paperwork. Im not saying dont do it. But it starts to come with a little more risk.I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0 -

ulcerative colitis since 2017

removal of the bowel last year

yeah something doesn't feel right 0

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards