We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Interest calculations check

Yorkie1

Posts: 12,475 Forumite

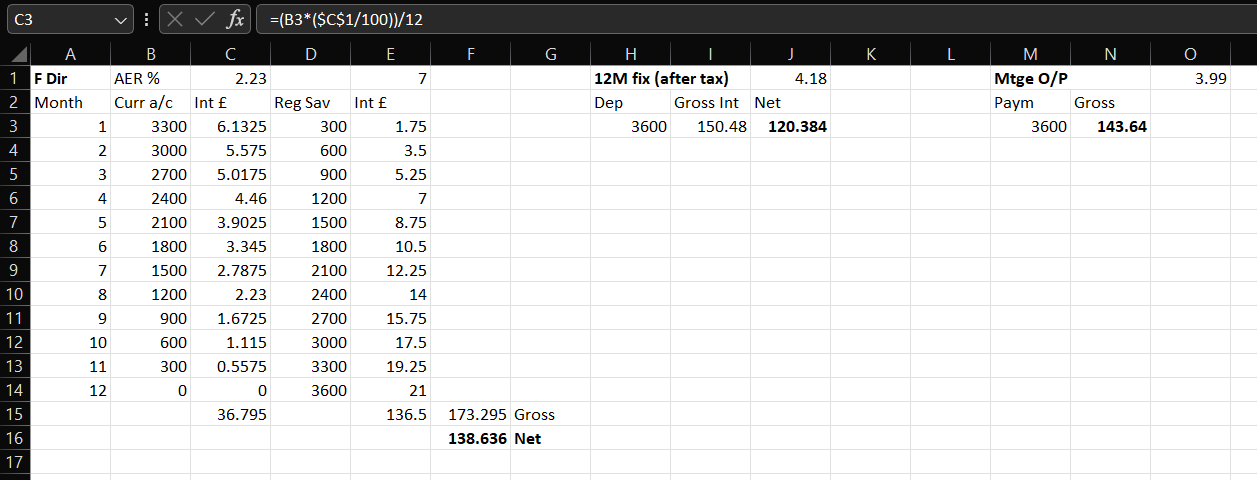

Someone recently suggested that I should work out whether it would be better value to spend a given amount of money on a 12 month regular saver, a 12 month fixed account, or paying that amount off the mortgage. Sample interest rates and values used.

For Reg Saver - funds start completely in the current account at month zero at 2.23%; then move at £300 per month at the start of months 1-12 to the reg saver at 7%.

Calculate each month's interest for each account by multiplying by the relevant % and dividing by 12.

All added up at the end to get the overall interest for the year, paid gross, which must then be multiplied by 0.8 to account for basic rate tax.

12M saver - whole value of funds multiplied by 4.18% to get the year's interest.

That is then multiplied by 0.8 again to get to net of tax.

Mortgage rate - multiply the whole value of funds by the interest rate of 3.99% to compare figures.

Stays at gross rate for comparison purposes.

Screenshot below (the calculation in the formula tool bar is for cell C3: the interest for the balance in the current account for that month):

On these figures, I get more interest from the overall reg saver than the 12M fix, but it's marginally better value still to pay the amount off the mortgage. Am I in the right ball park, please? I know interest is calculated daily but that's a step too far for my spreadsheet and me!

Thanks a lot for any comments.

For Reg Saver - funds start completely in the current account at month zero at 2.23%; then move at £300 per month at the start of months 1-12 to the reg saver at 7%.

Calculate each month's interest for each account by multiplying by the relevant % and dividing by 12.

All added up at the end to get the overall interest for the year, paid gross, which must then be multiplied by 0.8 to account for basic rate tax.

12M saver - whole value of funds multiplied by 4.18% to get the year's interest.

That is then multiplied by 0.8 again to get to net of tax.

Mortgage rate - multiply the whole value of funds by the interest rate of 3.99% to compare figures.

Stays at gross rate for comparison purposes.

Screenshot below (the calculation in the formula tool bar is for cell C3: the interest for the balance in the current account for that month):

On these figures, I get more interest from the overall reg saver than the 12M fix, but it's marginally better value still to pay the amount off the mortgage. Am I in the right ball park, please? I know interest is calculated daily but that's a step too far for my spreadsheet and me!

Thanks a lot for any comments.

0

Comments

-

I think the calculations are right, though it you were prepared to move money manually each month, you might do better with other reg savers - eg

Principality BS 7.5% up to £200/mth for 6 mths - put all you can in this

plus Monmouthshire BS up to £500/mth for 12 mths - fill this to £2000 in 4 mths, then £400 for 1 mth, £0 the next mth, then £500 again (when the Principality one matures) until the £3600 has been put in

Keep the cash which is not yet in a reg saver in Cahoot Sunny Day Saver at 5%

By my reckoning, that gets you £171.33 after 20% tax. Whether the £28 is worth the extra hassle would be up to you. If you use the 2.23%-bearing current account rather than Cahoot, I think it's £155.64.1 -

I think you’re overcomplicating things - but calculation is likely correct (I didn’t check)

can you not get a better temporary interest account than 2.23%?Let’s say you found one at 3%Then approximately your annual interest rate on the monthly saver would be

0.5 x (3 + 7) = 5%

vs 4.18% 12m fixed saver

vs 3.99 (4%) mortgage.vs 4.61% (your monthly saver 7% and 2.23%Only multiply the savers above by .8 (or .6) if you’re sure you’re earning more than 500 (or £1000) in interest in the FY

If you have a lower earning spouse put savings in their accounts.

if you want to factor in daily compounded interest then don’t forget you can get almost 13 payments into a 12m saver if you open account at right time of month.2 -

You beat me to it. Unless you've got more savings in non-ISA accounts elsewhere, it's likely you won't be paying tax on the interest.On-the-coast said:Only multiply the savers above by .8 (or .6) if you’re sure you’re earning more than 500 (or £1000) in interest in the FY

If you have a lower earning spouse put savings in their accounts.

Also if the gains are only marginal, forget about any calculations and think instead about whether paying off your mortgage is important to you in the long term. I would personally go down that route rather than eke out a little more interest in the regular saver, because I can't be sure what will happen in future years - health issues, job changes etc. might affect my mortgage payments. Or for the same reasons you might want to keep the money in savings in case you need it. It's up to you.2 -

Yorkie1 said:...

12M saver - whole value of funds multiplied by 4.18% to get the year's interest.

That is then multiplied by 0.8 again to get to net of tax.

Mortgage rate - multiply the whole value of funds by the interest rate of 3.99% to compare figures.

Stays at gross rate for comparison purposes.4.18%*0.8= 3.34% - this is obviously less than 3.99% and you don't need any Excel to compare these twoFor a regular saver (R%) combined with an easy access saver (E%) the exact formula is(R*6.5 + E*5.5)/12*0.8All this was assuming that you do pay 20% tax on your savings interest.

2 -

Many thanks everyone for your comments.

At present I expect to be lucky enough this year to have more than £1K in taxable savings interest, and am a basic rate taxpayer.

You're right about being able to get more interest on the easy access part of it. It's about deciding where to draw the level of juggling and complexity, as you say.

The aim is to pay off the mortgage in the next year or so. I had just got so used to focusing on the higher regular savings interest rates that diverting funds at the end of, or instead of, regular savers (rather than recycling the funds into the next year's saver from the matured easy access account).0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards