We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Small pots to maximise use of 0% tax band

MallyGirl

Posts: 7,546 Senior Ambassador

Hi

I've been pretty successful in getting most of my redundancy (taxable bit) into my pension via salary sacrifice whilst meeting NLW requirements. As a result I have only earned £9,760 taxable this year and my employer has contributed £45,623 to my pension.

Since I have the time to do the admin I think I can contribute to a new SIPP (with HL for small pot ease) and get it back out as small pots this year and next. I have no intention to earn again but I don't want to trigger MPAA yet as that shuts a door before I need to. I won't be taking any pension this year other than the small pot. OH is not retiring yet.

AIUI I can contribute £7,808 to a SIPP which will be grossed up to match my £9,760 taxable income. I can then take a small pot of £3,226 which will have a taxable element of £2,420 to keep me under £12,180 (with a tax code of 1218L) and not cost me any tax. I will also get a rebate of tax already paid at some point and maybe also a new tax code due to the partial year of taxable benefits. Next year I can put in £2,880 which will be grossed up to £3,600 as I will have no earned income.

9,760+3,600 = 13,360.

13,360-3,226 = 10,134

I've been pretty successful in getting most of my redundancy (taxable bit) into my pension via salary sacrifice whilst meeting NLW requirements. As a result I have only earned £9,760 taxable this year and my employer has contributed £45,623 to my pension.

Since I have the time to do the admin I think I can contribute to a new SIPP (with HL for small pot ease) and get it back out as small pots this year and next. I have no intention to earn again but I don't want to trigger MPAA yet as that shuts a door before I need to. I won't be taking any pension this year other than the small pot. OH is not retiring yet.

AIUI I can contribute £7,808 to a SIPP which will be grossed up to match my £9,760 taxable income. I can then take a small pot of £3,226 which will have a taxable element of £2,420 to keep me under £12,180 (with a tax code of 1218L) and not cost me any tax. I will also get a rebate of tax already paid at some point and maybe also a new tax code due to the partial year of taxable benefits. Next year I can put in £2,880 which will be grossed up to £3,600 as I will have no earned income.

9,760+3,600 = 13,360.

13,360-3,226 = 10,134

That leaves me with £10,134 (plus any growth) to take as a second small pot next year with a little bit left over. The taxable element will be under the 0% boundary so again no tax to pay.

Have I understood the rules right?

Thanks in advance.

Have I understood the rules right?

Thanks in advance.

I’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.

0

Comments

-

Some quick observations.

Small pots are a technical term and have to be below £10k, Taking £3226 in the first year is OK but taking £10134 the following year will breach that limit and trigger the Money Purchase Annual Allowance.

Redundancy isn't necessarily forever. If you're ever likely to gain a wage again in the decades to come having breached the small pot rules will limit how much you can add to a pension in the future.

With a bit of jiggling you could delay the first pot until the 2nd year and split the £13360 to stay below the £10k max. You can take up to 3 small pots at any time.0 -

Yes - I wouldn't take more than £10K from pot 2 leaving a little bit for a 3rd pot. I don't want to trigger MPAA just in caseI’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.0 -

Please double check but my understanding is when taking a small pot the pension has to be collected in full and closed. You can't just leave a bit behind. As there's a max amount removable by small pots it makes sense to maximise the amount you extract to nearer £30k if poss. Does you provider allow splitting like this?MallyGirl said:Yes - I wouldn't take more than £10K from pot 2 leaving a little bit for a 3rd pot. I don't want to trigger MPAA just in case

I understood about not triggering MPAA jic, had similar thoughts myself.0 -

Hargreaves will create a separate £10k pot specifically for this fiddle, oops, requirement. 🤣🤣🤣kempiejon said:

Please double check but my understanding is when taking a small pot the pension has to be collected in full and closed. You can't just leave a bit behind. As there's a max amount removable by small pots it makes sense to maximise the amount you extract to nearer £30k if poss. Does you provider allow splitting like this?MallyGirl said:Yes - I wouldn't take more than £10K from pot 2 leaving a little bit for a 3rd pot. I don't want to trigger MPAA just in case

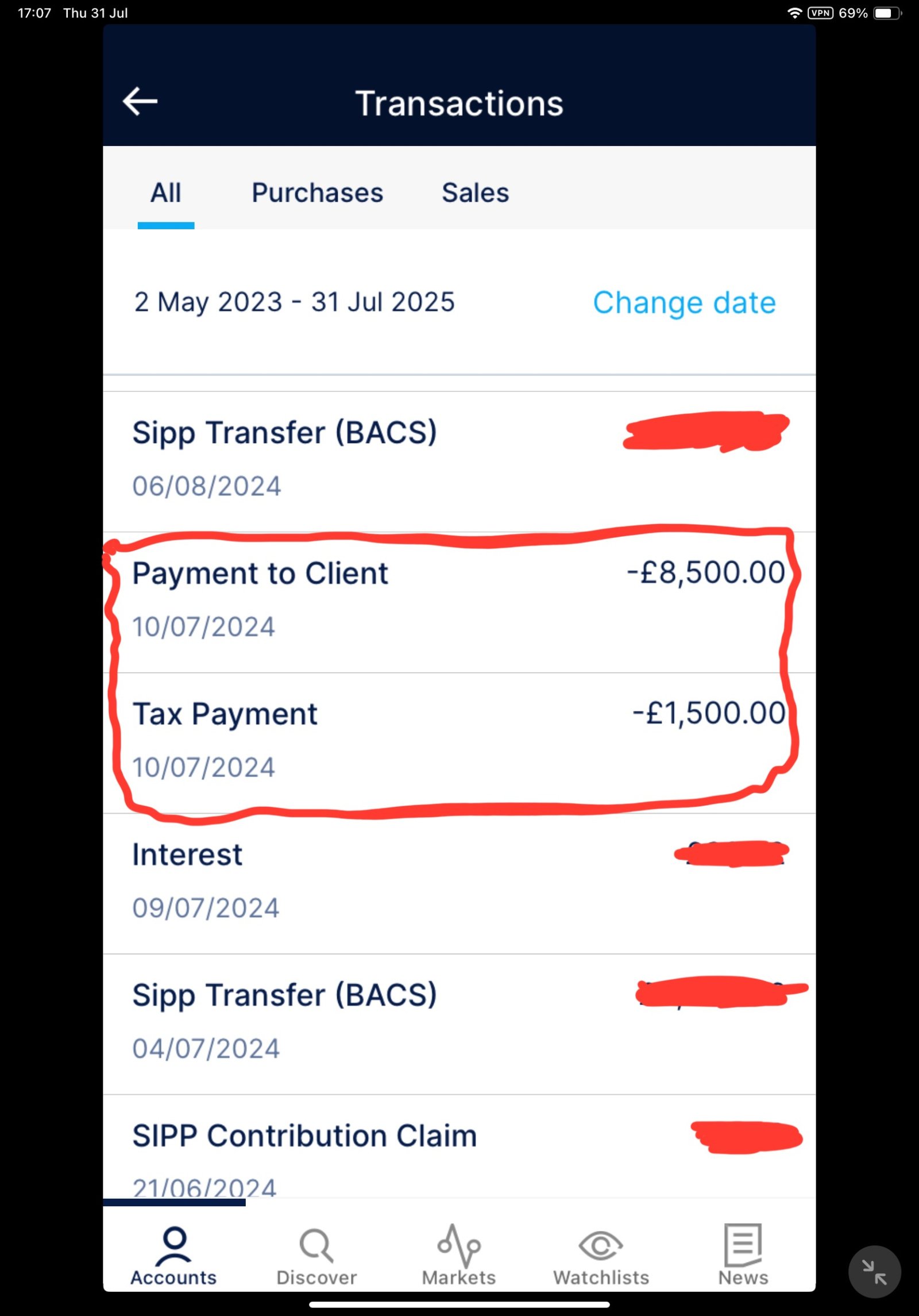

I understood about not triggering MPAA jic, had similar thoughts myself. £2,500 tax free

£2,500 tax free

£7,500 taxable at BR regardless of tax code (corrected by HMRC code adjustment if wrong) so £1,500 tax.1 -

That is correct.kempiejon said:

Please double check but my understanding is when taking a small pot the pension has to be collected in full and closed. You can't just leave a bit behind. As there's a max amount removable by small pots it makes sense to maximise the amount you extract to nearer £30k if poss. Does you provider allow splitting like this?MallyGirl said:Yes - I wouldn't take more than £10K from pot 2 leaving a little bit for a 3rd pot. I don't want to trigger MPAA just in case

I understood about not triggering MPAA jic, had similar thoughts myself.

When making a withdrawal under The Small Pots Rule, you have to take everything in the pension pot, and that pension is then closed. You also have to inform the provider specifically that is what you want to do, and fill in a form ( in my experience) and not just make an online 'normal' withdrawal .

The advantage is of course that you do not trigger MPAA, and there is zero contribution to the tax free lump sum allowance limit.

AFAIK , only HL will split a bigger pot into small pots ( as mentioned as a kind of fiddle).

Some other providers offer single Small Pot Withdrawals, but not all do.1 -

...in total from personal pension arrangements, plus an unlimited number from true 'occupational' pension schemes. In practice very few people are likely to have more than one 'small pot' resulting from short term membership of an occupational scheme, so this post is added for accuracy/completeness (and shouldn't raise false hopes!).kempiejon said:You can take up to 3 small pots at any time.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards