We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Index-Linked Gilts question

Comments

-

Interesting. The market cannot be asleep, so the best explanation is that the balance of institutional over speculative (small 's') buyers is preventing the price of post-2030 ILGs being discounted. For the Treasury that is doubly good news, since not only will they pay lower coupons post-2030 but they can also auction new issue ILGs at a higher price (theoretically 0.9%-1.0% lower) than if the ILG market was efficient.masonic said:zagfles said:

Thanks, interesting analysis. Reminds me of a previous thread where we were discussing the apparent illogical market pricing of gilts. Global or UK bond index - which and why? - Page 2 — MoneySavingExpert Forummasonic said:zagfles said:

I think it's fairly clear just from looking at clean prices that the market is accounting for the lower index linking post 2030. For instance the 2029 and 2036 ILGs have the same 0.125% coupon, the clean price for the 2029 is 98.275 and for 2036 is 85.3, so the annualised capital gain is around 0.5% for 2029 and 1.4% for 2036 above the inflation measure.masonic said:aroominyork said:masonic & GeoffTF (I’m too old to do the ‘@’ thing), are you saying there is an PRI premium that will disappear post-2030? masonic, you say “You can see the market's appraisal of that in the ILG yield curve.”. Can you please post or link to that? The view I was positing is that demand for gilts is not driven essentially by whether they represent value (RPI rather than CPI) but by institutional demand to meet future redemptions. Please educate me!

I would point you to the Bank of England's yield curve graph for implied inflation, and the real yield vs nominal yield data to calculate breakeven inflation across durations.I don't think you'll find much evidence that the market will be compensating investors for the lower rate of index linking post-2030.Whether this is going to happen at some point in the future (i.e further price falls at the long end of the curve) I do not know, but it seems unlikely given it's been known about for quite a long time now.Either way, if you buy a ILG today with a maturity much beyond 2030, you won't be getting as good a deal as you could in the past (low interest rate era excepted).The 2029 ILG has a real YTM of 0.6%, whereas the closest nominal equivalent TG29 a nominal YTM of 3.7%, giving an implied RPI of 3.1%.For the 2036 ILG, it's 1.5%, and T4Q 4.6%, giving 3.1%Going out much further, for T68, it's 2.0% and TR68, 5.2%, giving 3.2%.Historically, the difference between RPI and CPI/CPIH has been ~0.9%, so one should expect an increase in nominal coupon relative to flat gilts and a decrease in breakeven rate. There doesn't seem to be any evidence of that. The market's long term expectation of inflation, beyond 10 years or so, tends to be quite constant, because it cannot predict when high or low inflation periods will fall, and so you'd expect it to be flat if the measure of inflation remained constant, or trend downwards if a new, less generous, measure of inflation were introduced, in proportion to the proportion of time index linking would accrue according to the lower measure.Following the announcement of the uncompensated alignment in late 2020, the immediate reaction of the market was to price inflation slightly higher, which is the opposite of what would have been expected, but perhaps it was muted by pent up demand for inflation hedging, or had been priced in earlier, in the 2010s, but if you look at yield curves from that era, that are shaped quite similarly to those around 2020.I do agree it seems implausible that a change anticipated for years and then confirmed 10 years ahead of implementation would not be priced in, but that is exactly what the data is telling me. Perhaps an explanation for this is that ILG are primarily liability driven investments and their principal liability (RPI linked annuities) will also see the same effect. Pension funds will not lose out if they are receiving less and paying out less due to RPI aligning with CPIH. Though using ILG for other purposes may result in a shortfall.The only conclusion I can reach is that investors will get a lower overall rate of return from these longer duration instruments, without compensation arising from market pricing. They will just have to live with a new, lower, inflation benchmark and live with them being a somewhat less attractive investment than they have been historically. Just as those who have annuitised with RPI-linking will have to do.

If as you say the main users are pension funds etc using them for liability matching and they drown out the effect of speculators and active investment funds looking for opportunities to beat the market then that may make sense, I guess even the vast majority of gilt funds tend to be passive rather than actively managed.

Maybe I was right in the previous thread and there's opportunity here to take advantage of this apparent market inefficiency!There are some interesting views about the market being wrong on this. For example https://www.youtube.com/watch?v=nxj_ToBBTGQ&pp=ygUgaW5kZXggbGlua2VkIGdpbHRzIG5vdCBwcmljZWQgaW4%3DI don't buy that there's going to be some future pricing in event personally, but perhaps there is some shorting money to be made.0

https://www.youtube.com/watch?v=nxj_ToBBTGQ&pp=ygUgaW5kZXggbGlua2VkIGdpbHRzIG5vdCBwcmljZWQgaW4%3DI don't buy that there's going to be some future pricing in event personally, but perhaps there is some shorting money to be made.0 -

It's far too simplistic to assume that the price is correct on the basis of RPI continuing. RPI average over the last 10 years was 4.6%, over the last 20 years was 3.8%, over the last 50 years was 5%, over the last 100 years 4.5%.aroominyork said:

Interesting. The market cannot be asleep, so the best explanation is that the balance of institutional over speculative buyers is preventing the price of post-2030 ILGs being discounted. For the Treasury that is doubly good news, since not only will they pay lower coupons post-2030 but they can also auction new issue ILGs at a higher price (theoretically 0.9%-1.0%) than if the ILG market was efficient.masonic said:zagfles said:

Thanks, interesting analysis. Reminds me of a previous thread where we were discussing the apparent illogical market pricing of gilts. Global or UK bond index - which and why? - Page 2 — MoneySavingExpert Forummasonic said:zagfles said:

I think it's fairly clear just from looking at clean prices that the market is accounting for the lower index linking post 2030. For instance the 2029 and 2036 ILGs have the same 0.125% coupon, the clean price for the 2029 is 98.275 and for 2036 is 85.3, so the annualised capital gain is around 0.5% for 2029 and 1.4% for 2036 above the inflation measure.masonic said:aroominyork said:masonic & GeoffTF (I’m too old to do the ‘@’ thing), are you saying there is an PRI premium that will disappear post-2030? masonic, you say “You can see the market's appraisal of that in the ILG yield curve.”. Can you please post or link to that? The view I was positing is that demand for gilts is not driven essentially by whether they represent value (RPI rather than CPI) but by institutional demand to meet future redemptions. Please educate me!

I would point you to the Bank of England's yield curve graph for implied inflation, and the real yield vs nominal yield data to calculate breakeven inflation across durations.I don't think you'll find much evidence that the market will be compensating investors for the lower rate of index linking post-2030.Whether this is going to happen at some point in the future (i.e further price falls at the long end of the curve) I do not know, but it seems unlikely given it's been known about for quite a long time now.Either way, if you buy a ILG today with a maturity much beyond 2030, you won't be getting as good a deal as you could in the past (low interest rate era excepted).The 2029 ILG has a real YTM of 0.6%, whereas the closest nominal equivalent TG29 a nominal YTM of 3.7%, giving an implied RPI of 3.1%.For the 2036 ILG, it's 1.5%, and T4Q 4.6%, giving 3.1%Going out much further, for T68, it's 2.0% and TR68, 5.2%, giving 3.2%.Historically, the difference between RPI and CPI/CPIH has been ~0.9%, so one should expect an increase in nominal coupon relative to flat gilts and a decrease in breakeven rate. There doesn't seem to be any evidence of that. The market's long term expectation of inflation, beyond 10 years or so, tends to be quite constant, because it cannot predict when high or low inflation periods will fall, and so you'd expect it to be flat if the measure of inflation remained constant, or trend downwards if a new, less generous, measure of inflation were introduced, in proportion to the proportion of time index linking would accrue according to the lower measure.Following the announcement of the uncompensated alignment in late 2020, the immediate reaction of the market was to price inflation slightly higher, which is the opposite of what would have been expected, but perhaps it was muted by pent up demand for inflation hedging, or had been priced in earlier, in the 2010s, but if you look at yield curves from that era, that are shaped quite similarly to those around 2020.I do agree it seems implausible that a change anticipated for years and then confirmed 10 years ahead of implementation would not be priced in, but that is exactly what the data is telling me. Perhaps an explanation for this is that ILG are primarily liability driven investments and their principal liability (RPI linked annuities) will also see the same effect. Pension funds will not lose out if they are receiving less and paying out less due to RPI aligning with CPIH. Though using ILG for other purposes may result in a shortfall.The only conclusion I can reach is that investors will get a lower overall rate of return from these longer duration instruments, without compensation arising from market pricing. They will just have to live with a new, lower, inflation benchmark and live with them being a somewhat less attractive investment than they have been historically. Just as those who have annuitised with RPI-linking will have to do.

If as you say the main users are pension funds etc using them for liability matching and they drown out the effect of speculators and active investment funds looking for opportunities to beat the market then that may make sense, I guess even the vast majority of gilt funds tend to be passive rather than actively managed.

Maybe I was right in the previous thread and there's opportunity here to take advantage of this apparent market inefficiency!There are some interesting views about the market being wrong on this. For examplehttps://www.youtube.com/watch?v=nxj_ToBBTGQ&pp=ygUgaW5kZXggbGlua2VkIGdpbHRzIG5vdCBwcmljZWQgaW4%3DI don't buy that there's going to be some future pricing in event personally, but perhaps there is some shorting money to be made.

Yet the market has apparently priced in an assumed inflation of 3.1%. That's way below RPI historically, and even below RPI minus the 1% or so premium over CPIH. So if anything, long dated gilts look underpriced not overpriced!!1 -

zagfles said:

Or maybe it's the other way round. CPIH average over the last 10 years has been 3.3%, so if the market has priced in 3.1% inflation then maybe it's not long dated gilts that are overpriced but shorter dated ones underpriced! Either that or the market is expecting inflation to be lower than usual over the next 5 years.masonic said:zagfles said:

Thanks, interesting analysis. Reminds me of a previous thread where we were discussing the apparent illogical market pricing of gilts. Global or UK bond index - which and why? - Page 2 — MoneySavingExpert Forummasonic said:zagfles said:

I think it's fairly clear just from looking at clean prices that the market is accounting for the lower index linking post 2030. For instance the 2029 and 2036 ILGs have the same 0.125% coupon, the clean price for the 2029 is 98.275 and for 2036 is 85.3, so the annualised capital gain is around 0.5% for 2029 and 1.4% for 2036 above the inflation measure.masonic said:aroominyork said:masonic & GeoffTF (I’m too old to do the ‘@’ thing), are you saying there is an PRI premium that will disappear post-2030? masonic, you say “You can see the market's appraisal of that in the ILG yield curve.”. Can you please post or link to that? The view I was positing is that demand for gilts is not driven essentially by whether they represent value (RPI rather than CPI) but by institutional demand to meet future redemptions. Please educate me!

I would point you to the Bank of England's yield curve graph for implied inflation, and the real yield vs nominal yield data to calculate breakeven inflation across durations.I don't think you'll find much evidence that the market will be compensating investors for the lower rate of index linking post-2030.Whether this is going to happen at some point in the future (i.e further price falls at the long end of the curve) I do not know, but it seems unlikely given it's been known about for quite a long time now.Either way, if you buy a ILG today with a maturity much beyond 2030, you won't be getting as good a deal as you could in the past (low interest rate era excepted).The 2029 ILG has a real YTM of 0.6%, whereas the closest nominal equivalent TG29 a nominal YTM of 3.7%, giving an implied RPI of 3.1%.For the 2036 ILG, it's 1.5%, and T4Q 4.6%, giving 3.1%Going out much further, for T68, it's 2.0% and TR68, 5.2%, giving 3.2%.Historically, the difference between RPI and CPI/CPIH has been ~0.9%, so one should expect an increase in nominal coupon relative to flat gilts and a decrease in breakeven rate. There doesn't seem to be any evidence of that. The market's long term expectation of inflation, beyond 10 years or so, tends to be quite constant, because it cannot predict when high or low inflation periods will fall, and so you'd expect it to be flat if the measure of inflation remained constant, or trend downwards if a new, less generous, measure of inflation were introduced, in proportion to the proportion of time index linking would accrue according to the lower measure.Following the announcement of the uncompensated alignment in late 2020, the immediate reaction of the market was to price inflation slightly higher, which is the opposite of what would have been expected, but perhaps it was muted by pent up demand for inflation hedging, or had been priced in earlier, in the 2010s, but if you look at yield curves from that era, that are shaped quite similarly to those around 2020.I do agree it seems implausible that a change anticipated for years and then confirmed 10 years ahead of implementation would not be priced in, but that is exactly what the data is telling me. Perhaps an explanation for this is that ILG are primarily liability driven investments and their principal liability (RPI linked annuities) will also see the same effect. Pension funds will not lose out if they are receiving less and paying out less due to RPI aligning with CPIH. Though using ILG for other purposes may result in a shortfall.The only conclusion I can reach is that investors will get a lower overall rate of return from these longer duration instruments, without compensation arising from market pricing. They will just have to live with a new, lower, inflation benchmark and live with them being a somewhat less attractive investment than they have been historically. Just as those who have annuitised with RPI-linking will have to do.

If as you say the main users are pension funds etc using them for liability matching and they drown out the effect of speculators and active investment funds looking for opportunities to beat the market then that may make sense, I guess even the vast majority of gilt funds tend to be passive rather than actively managed.

Maybe I was right in the previous thread and there's opportunity here to take advantage of this apparent market inefficiency!There are some interesting views about the market being wrong on this. For examplehttps://www.youtube.com/watch?v=nxj_ToBBTGQ&pp=ygUgaW5kZXggbGlua2VkIGdpbHRzIG5vdCBwcmljZWQgaW4%3DI don't buy that there's going to be some future pricing in event personally, but perhaps there is some shorting money to be made.If you download the yield curve data series from the BoE, there is no shift at the long end that would correspond to a transition from RPI-based pricing to CPIH-based pricing, and BoE state that they have not changed their methodology to account for it. To go back any further, it is necessary to drop duration to 25 year, which means the data gets noisier.

To go back any further, it is necessary to drop duration to 25 year, which means the data gets noisier. There is clearly a period prior to the GFC where inflation expectations were lower. But this seems too early to link to the replacement of RPI. If anything the trend has been down since 2008. So I'm struggling to see at which point markets could have reacted to the decision and repriced long ILG accordingly. Unless the market simultaneously reacted to this news and decided 40-year inflation would be lower.0

There is clearly a period prior to the GFC where inflation expectations were lower. But this seems too early to link to the replacement of RPI. If anything the trend has been down since 2008. So I'm struggling to see at which point markets could have reacted to the decision and repriced long ILG accordingly. Unless the market simultaneously reacted to this news and decided 40-year inflation would be lower.0 -

RPI replacement has been on the cards for decades, in 2003 they stopped using it for inflation targets, in 2013 the ONS stopped classifying it as a "national statistic", in 2018 the BoE wanted it abandoned, and the 2030 date was actually an extension of RPI's life, the ONS wanted it replaced sooner. Everyone knew it was happening and it probably is happening later than original expectations. So maybe the shift away from RPI was priced in decades ago. As above, your 3.1% calculation of implied inflation is way below historic RPI.masonic said:zagfles said:

Or maybe it's the other way round. CPIH average over the last 10 years has been 3.3%, so if the market has priced in 3.1% inflation then maybe it's not long dated gilts that are overpriced but shorter dated ones underpriced! Either that or the market is expecting inflation to be lower than usual over the next 5 years.masonic said:zagfles said:

Thanks, interesting analysis. Reminds me of a previous thread where we were discussing the apparent illogical market pricing of gilts. Global or UK bond index - which and why? - Page 2 — MoneySavingExpert Forummasonic said:zagfles said:

I think it's fairly clear just from looking at clean prices that the market is accounting for the lower index linking post 2030. For instance the 2029 and 2036 ILGs have the same 0.125% coupon, the clean price for the 2029 is 98.275 and for 2036 is 85.3, so the annualised capital gain is around 0.5% for 2029 and 1.4% for 2036 above the inflation measure.masonic said:aroominyork said:masonic & GeoffTF (I’m too old to do the ‘@’ thing), are you saying there is an PRI premium that will disappear post-2030? masonic, you say “You can see the market's appraisal of that in the ILG yield curve.”. Can you please post or link to that? The view I was positing is that demand for gilts is not driven essentially by whether they represent value (RPI rather than CPI) but by institutional demand to meet future redemptions. Please educate me!

I would point you to the Bank of England's yield curve graph for implied inflation, and the real yield vs nominal yield data to calculate breakeven inflation across durations.I don't think you'll find much evidence that the market will be compensating investors for the lower rate of index linking post-2030.Whether this is going to happen at some point in the future (i.e further price falls at the long end of the curve) I do not know, but it seems unlikely given it's been known about for quite a long time now.Either way, if you buy a ILG today with a maturity much beyond 2030, you won't be getting as good a deal as you could in the past (low interest rate era excepted).The 2029 ILG has a real YTM of 0.6%, whereas the closest nominal equivalent TG29 a nominal YTM of 3.7%, giving an implied RPI of 3.1%.For the 2036 ILG, it's 1.5%, and T4Q 4.6%, giving 3.1%Going out much further, for T68, it's 2.0% and TR68, 5.2%, giving 3.2%.Historically, the difference between RPI and CPI/CPIH has been ~0.9%, so one should expect an increase in nominal coupon relative to flat gilts and a decrease in breakeven rate. There doesn't seem to be any evidence of that. The market's long term expectation of inflation, beyond 10 years or so, tends to be quite constant, because it cannot predict when high or low inflation periods will fall, and so you'd expect it to be flat if the measure of inflation remained constant, or trend downwards if a new, less generous, measure of inflation were introduced, in proportion to the proportion of time index linking would accrue according to the lower measure.Following the announcement of the uncompensated alignment in late 2020, the immediate reaction of the market was to price inflation slightly higher, which is the opposite of what would have been expected, but perhaps it was muted by pent up demand for inflation hedging, or had been priced in earlier, in the 2010s, but if you look at yield curves from that era, that are shaped quite similarly to those around 2020.I do agree it seems implausible that a change anticipated for years and then confirmed 10 years ahead of implementation would not be priced in, but that is exactly what the data is telling me. Perhaps an explanation for this is that ILG are primarily liability driven investments and their principal liability (RPI linked annuities) will also see the same effect. Pension funds will not lose out if they are receiving less and paying out less due to RPI aligning with CPIH. Though using ILG for other purposes may result in a shortfall.The only conclusion I can reach is that investors will get a lower overall rate of return from these longer duration instruments, without compensation arising from market pricing. They will just have to live with a new, lower, inflation benchmark and live with them being a somewhat less attractive investment than they have been historically. Just as those who have annuitised with RPI-linking will have to do.

If as you say the main users are pension funds etc using them for liability matching and they drown out the effect of speculators and active investment funds looking for opportunities to beat the market then that may make sense, I guess even the vast majority of gilt funds tend to be passive rather than actively managed.

Maybe I was right in the previous thread and there's opportunity here to take advantage of this apparent market inefficiency!There are some interesting views about the market being wrong on this. For examplehttps://www.youtube.com/watch?v=nxj_ToBBTGQ&pp=ygUgaW5kZXggbGlua2VkIGdpbHRzIG5vdCBwcmljZWQgaW4%3DI don't buy that there's going to be some future pricing in event personally, but perhaps there is some shorting money to be made.If you download the yield curve data series from the BoE, there is no shift at the long end that would correspond to a transition from RPI-based pricing to CPIH-based pricing, and BoE state that they have not changed their methodology to account for it.To go back any further, it is necessary to drop duration to 25 year, which means the data gets noisier.There is clearly a period prior to the GFC where inflation expectations were lower. But this seems too early to link to the replacement of RPI. If anything the trend has been down since 2008. So I'm struggling to see at which point markets could have reacted to the decision and repriced long ILG accordingly. Unless the market simultaneously reacted to this news and decided 40-year inflation would be lower.0 -

zagfles said:

RPI replacement has been on the cards for decades, in 2003 they stopped using it for inflation targets, in 2013 the ONS stopped classifying it as a "national statistic", in 2018 the BoE wanted it abandoned, and the 2030 date was actually an extension of RPI's life, the ONS wanted it replaced sooner. Everyone knew it was happening and it probably is happening later than original expectations. So maybe the shift away from RPI was priced in decades ago. As above, your 3.1% calculation of implied inflation is way below historic RPI.masonic said:zagfles said:

Or maybe it's the other way round. CPIH average over the last 10 years has been 3.3%, so if the market has priced in 3.1% inflation then maybe it's not long dated gilts that are overpriced but shorter dated ones underpriced! Either that or the market is expecting inflation to be lower than usual over the next 5 years.masonic said:zagfles said:

Thanks, interesting analysis. Reminds me of a previous thread where we were discussing the apparent illogical market pricing of gilts. Global or UK bond index - which and why? - Page 2 — MoneySavingExpert Forummasonic said:zagfles said:

I think it's fairly clear just from looking at clean prices that the market is accounting for the lower index linking post 2030. For instance the 2029 and 2036 ILGs have the same 0.125% coupon, the clean price for the 2029 is 98.275 and for 2036 is 85.3, so the annualised capital gain is around 0.5% for 2029 and 1.4% for 2036 above the inflation measure.masonic said:aroominyork said:masonic & GeoffTF (I’m too old to do the ‘@’ thing), are you saying there is an PRI premium that will disappear post-2030? masonic, you say “You can see the market's appraisal of that in the ILG yield curve.”. Can you please post or link to that? The view I was positing is that demand for gilts is not driven essentially by whether they represent value (RPI rather than CPI) but by institutional demand to meet future redemptions. Please educate me!

I would point you to the Bank of England's yield curve graph for implied inflation, and the real yield vs nominal yield data to calculate breakeven inflation across durations.I don't think you'll find much evidence that the market will be compensating investors for the lower rate of index linking post-2030.Whether this is going to happen at some point in the future (i.e further price falls at the long end of the curve) I do not know, but it seems unlikely given it's been known about for quite a long time now.Either way, if you buy a ILG today with a maturity much beyond 2030, you won't be getting as good a deal as you could in the past (low interest rate era excepted).The 2029 ILG has a real YTM of 0.6%, whereas the closest nominal equivalent TG29 a nominal YTM of 3.7%, giving an implied RPI of 3.1%.For the 2036 ILG, it's 1.5%, and T4Q 4.6%, giving 3.1%Going out much further, for T68, it's 2.0% and TR68, 5.2%, giving 3.2%.Historically, the difference between RPI and CPI/CPIH has been ~0.9%, so one should expect an increase in nominal coupon relative to flat gilts and a decrease in breakeven rate. There doesn't seem to be any evidence of that. The market's long term expectation of inflation, beyond 10 years or so, tends to be quite constant, because it cannot predict when high or low inflation periods will fall, and so you'd expect it to be flat if the measure of inflation remained constant, or trend downwards if a new, less generous, measure of inflation were introduced, in proportion to the proportion of time index linking would accrue according to the lower measure.Following the announcement of the uncompensated alignment in late 2020, the immediate reaction of the market was to price inflation slightly higher, which is the opposite of what would have been expected, but perhaps it was muted by pent up demand for inflation hedging, or had been priced in earlier, in the 2010s, but if you look at yield curves from that era, that are shaped quite similarly to those around 2020.I do agree it seems implausible that a change anticipated for years and then confirmed 10 years ahead of implementation would not be priced in, but that is exactly what the data is telling me. Perhaps an explanation for this is that ILG are primarily liability driven investments and their principal liability (RPI linked annuities) will also see the same effect. Pension funds will not lose out if they are receiving less and paying out less due to RPI aligning with CPIH. Though using ILG for other purposes may result in a shortfall.The only conclusion I can reach is that investors will get a lower overall rate of return from these longer duration instruments, without compensation arising from market pricing. They will just have to live with a new, lower, inflation benchmark and live with them being a somewhat less attractive investment than they have been historically. Just as those who have annuitised with RPI-linking will have to do.

If as you say the main users are pension funds etc using them for liability matching and they drown out the effect of speculators and active investment funds looking for opportunities to beat the market then that may make sense, I guess even the vast majority of gilt funds tend to be passive rather than actively managed.

Maybe I was right in the previous thread and there's opportunity here to take advantage of this apparent market inefficiency!There are some interesting views about the market being wrong on this. For examplehttps://www.youtube.com/watch?v=nxj_ToBBTGQ&pp=ygUgaW5kZXggbGlua2VkIGdpbHRzIG5vdCBwcmljZWQgaW4%3DI don't buy that there's going to be some future pricing in event personally, but perhaps there is some shorting money to be made.If you download the yield curve data series from the BoE, there is no shift at the long end that would correspond to a transition from RPI-based pricing to CPIH-based pricing, and BoE state that they have not changed their methodology to account for it.To go back any further, it is necessary to drop duration to 25 year, which means the data gets noisier.There is clearly a period prior to the GFC where inflation expectations were lower. But this seems too early to link to the replacement of RPI. If anything the trend has been down since 2008. So I'm struggling to see at which point markets could have reacted to the decision and repriced long ILG accordingly. Unless the market simultaneously reacted to this news and decided 40-year inflation would be lower.So maybe that post-2003 period was the repricing, masked by all the other stuff going on, and then crocodile tears in 2020 about not being compensated when it was officially announced?Question then is why during the early 2000s was 25 year RPI inflation implied to be around 2.5% when it is way below historic RPI (not my calculation - just used the BoE's own numbers for this). Seems like long ILGs were a steal back then. Who in 2003 wouldn't have bet RPI from 2003-2028 would average above 2.3%? Whereas now we're being asked to bet CPIH* from 2025-2065 will be above 3.2% (*RPI for the first 5 years, then CPIH for the next 35).0 -

Possibly because they thought things will change after Gordon Brown's big decision to give the BoE interest rate setting powers and a mandate to hit the govt 2% inflation target.masonic said:zagfles said:

RPI replacement has been on the cards for decades, in 2003 they stopped using it for inflation targets, in 2013 the ONS stopped classifying it as a "national statistic", in 2018 the BoE wanted it abandoned, and the 2030 date was actually an extension of RPI's life, the ONS wanted it replaced sooner. Everyone knew it was happening and it probably is happening later than original expectations. So maybe the shift away from RPI was priced in decades ago. As above, your 3.1% calculation of implied inflation is way below historic RPI.masonic said:zagfles said:

Or maybe it's the other way round. CPIH average over the last 10 years has been 3.3%, so if the market has priced in 3.1% inflation then maybe it's not long dated gilts that are overpriced but shorter dated ones underpriced! Either that or the market is expecting inflation to be lower than usual over the next 5 years.masonic said:zagfles said:

Thanks, interesting analysis. Reminds me of a previous thread where we were discussing the apparent illogical market pricing of gilts. Global or UK bond index - which and why? - Page 2 — MoneySavingExpert Forummasonic said:zagfles said:

I think it's fairly clear just from looking at clean prices that the market is accounting for the lower index linking post 2030. For instance the 2029 and 2036 ILGs have the same 0.125% coupon, the clean price for the 2029 is 98.275 and for 2036 is 85.3, so the annualised capital gain is around 0.5% for 2029 and 1.4% for 2036 above the inflation measure.masonic said:aroominyork said:masonic & GeoffTF (I’m too old to do the ‘@’ thing), are you saying there is an PRI premium that will disappear post-2030? masonic, you say “You can see the market's appraisal of that in the ILG yield curve.”. Can you please post or link to that? The view I was positing is that demand for gilts is not driven essentially by whether they represent value (RPI rather than CPI) but by institutional demand to meet future redemptions. Please educate me!

I would point you to the Bank of England's yield curve graph for implied inflation, and the real yield vs nominal yield data to calculate breakeven inflation across durations.I don't think you'll find much evidence that the market will be compensating investors for the lower rate of index linking post-2030.Whether this is going to happen at some point in the future (i.e further price falls at the long end of the curve) I do not know, but it seems unlikely given it's been known about for quite a long time now.Either way, if you buy a ILG today with a maturity much beyond 2030, you won't be getting as good a deal as you could in the past (low interest rate era excepted).The 2029 ILG has a real YTM of 0.6%, whereas the closest nominal equivalent TG29 a nominal YTM of 3.7%, giving an implied RPI of 3.1%.For the 2036 ILG, it's 1.5%, and T4Q 4.6%, giving 3.1%Going out much further, for T68, it's 2.0% and TR68, 5.2%, giving 3.2%.Historically, the difference between RPI and CPI/CPIH has been ~0.9%, so one should expect an increase in nominal coupon relative to flat gilts and a decrease in breakeven rate. There doesn't seem to be any evidence of that. The market's long term expectation of inflation, beyond 10 years or so, tends to be quite constant, because it cannot predict when high or low inflation periods will fall, and so you'd expect it to be flat if the measure of inflation remained constant, or trend downwards if a new, less generous, measure of inflation were introduced, in proportion to the proportion of time index linking would accrue according to the lower measure.Following the announcement of the uncompensated alignment in late 2020, the immediate reaction of the market was to price inflation slightly higher, which is the opposite of what would have been expected, but perhaps it was muted by pent up demand for inflation hedging, or had been priced in earlier, in the 2010s, but if you look at yield curves from that era, that are shaped quite similarly to those around 2020.I do agree it seems implausible that a change anticipated for years and then confirmed 10 years ahead of implementation would not be priced in, but that is exactly what the data is telling me. Perhaps an explanation for this is that ILG are primarily liability driven investments and their principal liability (RPI linked annuities) will also see the same effect. Pension funds will not lose out if they are receiving less and paying out less due to RPI aligning with CPIH. Though using ILG for other purposes may result in a shortfall.The only conclusion I can reach is that investors will get a lower overall rate of return from these longer duration instruments, without compensation arising from market pricing. They will just have to live with a new, lower, inflation benchmark and live with them being a somewhat less attractive investment than they have been historically. Just as those who have annuitised with RPI-linking will have to do.

If as you say the main users are pension funds etc using them for liability matching and they drown out the effect of speculators and active investment funds looking for opportunities to beat the market then that may make sense, I guess even the vast majority of gilt funds tend to be passive rather than actively managed.

Maybe I was right in the previous thread and there's opportunity here to take advantage of this apparent market inefficiency!There are some interesting views about the market being wrong on this. For examplehttps://www.youtube.com/watch?v=nxj_ToBBTGQ&pp=ygUgaW5kZXggbGlua2VkIGdpbHRzIG5vdCBwcmljZWQgaW4%3DI don't buy that there's going to be some future pricing in event personally, but perhaps there is some shorting money to be made.If you download the yield curve data series from the BoE, there is no shift at the long end that would correspond to a transition from RPI-based pricing to CPIH-based pricing, and BoE state that they have not changed their methodology to account for it.To go back any further, it is necessary to drop duration to 25 year, which means the data gets noisier.There is clearly a period prior to the GFC where inflation expectations were lower. But this seems too early to link to the replacement of RPI. If anything the trend has been down since 2008. So I'm struggling to see at which point markets could have reacted to the decision and repriced long ILG accordingly. Unless the market simultaneously reacted to this news and decided 40-year inflation would be lower.So maybe that post-2003 period was the repricing, masked by all the other stuff going on, and then crocodile tears in 2020 about not being compensated when it was officially announced?Question then is why during the early 2000s was 25 year RPI inflation implied to be around 2.5% when it is way below historic RPI (not my calculation - just used the BoE's own numbers for this). Seems like long ILGs were a steal back then. Who in 2003 wouldn't have bet RPI from 2003-2028 would average above 2.3%? Whereas now we're being asked to bet CPIH from 2025-2065 will be above 3.2%.1 -

I wouldn't have thought it, but it does check out. CPI averaged just 1.5% over the decade from 1997, and RPI averaged 2.7%. So perhaps that would set the scene for markets to believe it would continue, as it did in the wake of the GFC, only for a rude awakening recently.zagfles said:

Possibly because they thought things will change after Gordon Brown's big decision to give the BoE interest rate setting powers and a mandate to hit the govt 2% inflation target.masonic said:zagfles said:

RPI replacement has been on the cards for decades, in 2003 they stopped using it for inflation targets, in 2013 the ONS stopped classifying it as a "national statistic", in 2018 the BoE wanted it abandoned, and the 2030 date was actually an extension of RPI's life, the ONS wanted it replaced sooner. Everyone knew it was happening and it probably is happening later than original expectations. So maybe the shift away from RPI was priced in decades ago. As above, your 3.1% calculation of implied inflation is way below historic RPI.masonic said:zagfles said:

Or maybe it's the other way round. CPIH average over the last 10 years has been 3.3%, so if the market has priced in 3.1% inflation then maybe it's not long dated gilts that are overpriced but shorter dated ones underpriced! Either that or the market is expecting inflation to be lower than usual over the next 5 years.masonic said:zagfles said:

Thanks, interesting analysis. Reminds me of a previous thread where we were discussing the apparent illogical market pricing of gilts. Global or UK bond index - which and why? - Page 2 — MoneySavingExpert Forummasonic said:zagfles said:

I think it's fairly clear just from looking at clean prices that the market is accounting for the lower index linking post 2030. For instance the 2029 and 2036 ILGs have the same 0.125% coupon, the clean price for the 2029 is 98.275 and for 2036 is 85.3, so the annualised capital gain is around 0.5% for 2029 and 1.4% for 2036 above the inflation measure.masonic said:aroominyork said:masonic & GeoffTF (I’m too old to do the ‘@’ thing), are you saying there is an PRI premium that will disappear post-2030? masonic, you say “You can see the market's appraisal of that in the ILG yield curve.”. Can you please post or link to that? The view I was positing is that demand for gilts is not driven essentially by whether they represent value (RPI rather than CPI) but by institutional demand to meet future redemptions. Please educate me!

I would point you to the Bank of England's yield curve graph for implied inflation, and the real yield vs nominal yield data to calculate breakeven inflation across durations.I don't think you'll find much evidence that the market will be compensating investors for the lower rate of index linking post-2030.Whether this is going to happen at some point in the future (i.e further price falls at the long end of the curve) I do not know, but it seems unlikely given it's been known about for quite a long time now.Either way, if you buy a ILG today with a maturity much beyond 2030, you won't be getting as good a deal as you could in the past (low interest rate era excepted).The 2029 ILG has a real YTM of 0.6%, whereas the closest nominal equivalent TG29 a nominal YTM of 3.7%, giving an implied RPI of 3.1%.For the 2036 ILG, it's 1.5%, and T4Q 4.6%, giving 3.1%Going out much further, for T68, it's 2.0% and TR68, 5.2%, giving 3.2%.Historically, the difference between RPI and CPI/CPIH has been ~0.9%, so one should expect an increase in nominal coupon relative to flat gilts and a decrease in breakeven rate. There doesn't seem to be any evidence of that. The market's long term expectation of inflation, beyond 10 years or so, tends to be quite constant, because it cannot predict when high or low inflation periods will fall, and so you'd expect it to be flat if the measure of inflation remained constant, or trend downwards if a new, less generous, measure of inflation were introduced, in proportion to the proportion of time index linking would accrue according to the lower measure.Following the announcement of the uncompensated alignment in late 2020, the immediate reaction of the market was to price inflation slightly higher, which is the opposite of what would have been expected, but perhaps it was muted by pent up demand for inflation hedging, or had been priced in earlier, in the 2010s, but if you look at yield curves from that era, that are shaped quite similarly to those around 2020.I do agree it seems implausible that a change anticipated for years and then confirmed 10 years ahead of implementation would not be priced in, but that is exactly what the data is telling me. Perhaps an explanation for this is that ILG are primarily liability driven investments and their principal liability (RPI linked annuities) will also see the same effect. Pension funds will not lose out if they are receiving less and paying out less due to RPI aligning with CPIH. Though using ILG for other purposes may result in a shortfall.The only conclusion I can reach is that investors will get a lower overall rate of return from these longer duration instruments, without compensation arising from market pricing. They will just have to live with a new, lower, inflation benchmark and live with them being a somewhat less attractive investment than they have been historically. Just as those who have annuitised with RPI-linking will have to do.

If as you say the main users are pension funds etc using them for liability matching and they drown out the effect of speculators and active investment funds looking for opportunities to beat the market then that may make sense, I guess even the vast majority of gilt funds tend to be passive rather than actively managed.

Maybe I was right in the previous thread and there's opportunity here to take advantage of this apparent market inefficiency!There are some interesting views about the market being wrong on this. For examplehttps://www.youtube.com/watch?v=nxj_ToBBTGQ&pp=ygUgaW5kZXggbGlua2VkIGdpbHRzIG5vdCBwcmljZWQgaW4%3DI don't buy that there's going to be some future pricing in event personally, but perhaps there is some shorting money to be made.If you download the yield curve data series from the BoE, there is no shift at the long end that would correspond to a transition from RPI-based pricing to CPIH-based pricing, and BoE state that they have not changed their methodology to account for it.To go back any further, it is necessary to drop duration to 25 year, which means the data gets noisier.There is clearly a period prior to the GFC where inflation expectations were lower. But this seems too early to link to the replacement of RPI. If anything the trend has been down since 2008. So I'm struggling to see at which point markets could have reacted to the decision and repriced long ILG accordingly. Unless the market simultaneously reacted to this news and decided 40-year inflation would be lower.So maybe that post-2003 period was the repricing, masked by all the other stuff going on, and then crocodile tears in 2020 about not being compensated when it was officially announced?Question then is why during the early 2000s was 25 year RPI inflation implied to be around 2.5% when it is way below historic RPI (not my calculation - just used the BoE's own numbers for this). Seems like long ILGs were a steal back then. Who in 2003 wouldn't have bet RPI from 2003-2028 would average above 2.3%? Whereas now we're being asked to bet CPIH from 2025-2065 will be above 3.2%.0 -

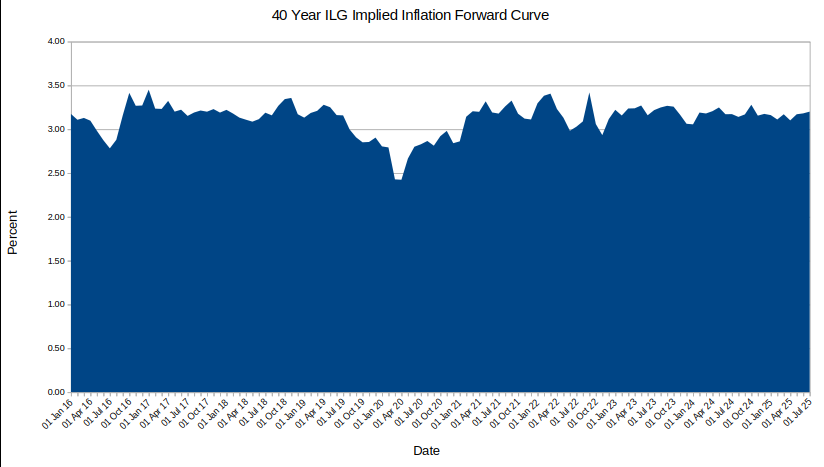

It occurred to me that the theory that the market is pricing in inflation at ~1% lower over the next 5 years or so could be tested by travelling back in time with the BoE dataset. Instead of looking at specific maturities over time, the full duration yield curve at specific dates could be examined. The below plot shows the breakeven inflation rate as it was at the end of Jan 2020 and Jan 2021. The end date for RPI was confirmed in Nov 2020, so the red line should have had plenty of time to price in the uncompensated cliff-edge.

There is a very slight downward slope beyond about 20 years maturity, but nowhere near enough to suggest investors had demanded a higher premium to compensate them for the change. But perhaps that premium was already reflected in the price through earlier anticipation. If that is the case then for the first decade or so the breakeven rate should be about 1% higher. The argument looking at the current yield curve was that the market expected inflation from 2025 to 2030 to average around 1% lower than after 2030. I think it is stretching credibility to suggest this low inflation period ending around 2030 was predicted 9-10 years ahead of time. The alternative explanation is that investors simply haven't driven the price of the longer issues down to command an extra premium to compensate them for the lower uplift after 2030, or to frame it a different way, investors have been getting a free lunch for this decade that will come to an end in 2030.0

There is a very slight downward slope beyond about 20 years maturity, but nowhere near enough to suggest investors had demanded a higher premium to compensate them for the change. But perhaps that premium was already reflected in the price through earlier anticipation. If that is the case then for the first decade or so the breakeven rate should be about 1% higher. The argument looking at the current yield curve was that the market expected inflation from 2025 to 2030 to average around 1% lower than after 2030. I think it is stretching credibility to suggest this low inflation period ending around 2030 was predicted 9-10 years ahead of time. The alternative explanation is that investors simply haven't driven the price of the longer issues down to command an extra premium to compensate them for the lower uplift after 2030, or to frame it a different way, investors have been getting a free lunch for this decade that will come to an end in 2030.0 -

It is pensions raid. People pay the same amount, but get less generous index linking after 2030. Those of us who buy ILGs have to put up with that too. The government benefits from lower payouts. It is easier for them to take money from peoples' pensions than it is to raise their tax bills. Most people will not even know what has happened.0

-

GeoffTF said:It is pensions raid. People pay the same amount, but get less generous index linking after 2030. Those of us who buy ILGs have to put up with that too. The government benefits from lower payouts. It is easier for them to take money from peoples' pensions than it is to raise their tax bills. Most people will not even know what has happened.If the government did not generate revenue from changing the indexing benchmark it would raise it from somewhere else. You have an option whether to buy ILGs - you do not have to 'put up with it', unlike income tax which is pretty much unavoidable.

0

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards