We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

maximising savings interest

Son_Of_Meerkat

Posts: 11 Forumite

I may be way off and admittedly i am not great with numbers...but..

there are several accounts out there that pay between 5% - 7%, on between 200-300 per month.

say first direct as an example, £300 per month. £3600 per year - £152 interest.

is it theoretically better to say have x amount, in a easy access saver or any such account and have all amounts of between £200-300 go to their respective bank savings account, per month.

as in say 6-8 different banks.

versus

locking it all away at say 4/5% for a year

For abit of context before anyone says it, yes that is of course not in an ISA. I am very fortunate in that I max out an isa every year, what i am trying to do is maximise what i get that i cannot put into an isa for that year, like several bonds/fixed term accounts etc i have

is it better to diversify and have lots of small amounts going to lots of higher interest savings accounts, which ultimately = more interest in the long run

apologies if this makes no sense, but its a question/idea i cant quite crunch the numbers on

there are several accounts out there that pay between 5% - 7%, on between 200-300 per month.

say first direct as an example, £300 per month. £3600 per year - £152 interest.

is it theoretically better to say have x amount, in a easy access saver or any such account and have all amounts of between £200-300 go to their respective bank savings account, per month.

as in say 6-8 different banks.

versus

locking it all away at say 4/5% for a year

For abit of context before anyone says it, yes that is of course not in an ISA. I am very fortunate in that I max out an isa every year, what i am trying to do is maximise what i get that i cannot put into an isa for that year, like several bonds/fixed term accounts etc i have

is it better to diversify and have lots of small amounts going to lots of higher interest savings accounts, which ultimately = more interest in the long run

apologies if this makes no sense, but its a question/idea i cant quite crunch the numbers on

0

Comments

-

Not sure how you are getting your figures. You are aware with regular saver (RS) accounts, the full interest is only applicable to half the total amount? This is on the basis that you build up the savings balance over the year. So until you get to the 6 month point you have less than half the amount saved. After the 6 month point you have more than half the amount saved. So after 12 months, interest is applied to half the amount saved. I suspect this is not a good explanation but sorry can't do better.By my calculation, say you save £300 per month at 5%.So at the half way point you would have saved £1800.Giving you £1800 X 5% = £90 interest for the whole year.Edited to add: a better explanation might be, by the end of the year you will have £3600 in the account. But until that point you don't have the full £3600 in the savings account. If you had the full £3600 in the account for the whole year at 5%, you would get £180 interest. But as you are building up to £3600, the interest is only applicable to the amount in the account at that time.So for the 1st month, interest would be applied to £300. (5% of £300 divided by 12 for the one month it has been in the account).In the 2nd month, the interest would be applied to £600. (5% of £600 divided by 12. You then add this interest to the interest from the 1st month to keep a running total.In the 3rd mont, the interest would be applied to £900. (5% of £900 divided by 12. You then add to the first 2 months to keep a running total.I think this explanation is right and hope it helps.1

-

For maximum interest, go with the best interest rate. So, regular saver accounts offering 6-7% will give you the best return. The only limitations being 1) some of them don't allow withdrawals until the end of the term (usually a year) and 2) there's a limit to how much money you can put in each month (usually £200-300).Son_Of_Meerkat said:I may be way off and admittedly i am not great with numbers...but..

there are several accounts out there that pay between 5% - 7%, on between 200-300 per month.

say first direct as an example, £300 per month. £3600 per year - £152 interest.

is it theoretically better to say have x amount, in a easy access saver or any such account and have all amounts of between £200-300 go to their respective bank savings account, per month.

as in say 6-8 different banks.

versus

locking it all away at say 4/5% for a year

For abit of context before anyone says it, yes that is of course not in an ISA. I am very fortunate in that I max out an isa every year, what i am trying to do is maximise what i get that i cannot put into an isa for that year, like several bonds/fixed term accounts etc i have

is it better to diversify and have lots of small amounts going to lots of higher interest savings accounts, which ultimately = more interest in the long run

apologies if this makes no sense, but its a question/idea i cant quite crunch the numbers on

There's nothing to stop you from opening several regular savers with different banks to maximise the total amount you can put away each month.

Depending on your circumstances, you way want to stagger your regular savers throughout the year so that they don't all mature at the same time. And find an easy access savings account with a good rate to keep any excess money while it's waiting to be put into the regular savers, so it's earning interest all year round. If you get the Santander Edge saver at 6% then it's a better rate than most regular savers but you can only save up to £4000. And there are other options for around 5%.0 -

I can see what you mean 😉Son_Of_Meerkat said:I may be way off and admittedly i am not great with numbers...but..

there are several accounts out there that pay between 5% - 7%, on between 200-300 per month.

say first direct as an example, £300 per month. £3600 per year - £152 interest.

is it theoretically better to say have x amount, in a easy access saver or any such account and have all amounts of between £200-300 go to their respective bank savings account, per month.

as in say 6-8 different banks.

versus

locking it all away at say 4/5% for a year

For abit of context before anyone says it, yes that is of course not in an ISA. I am very fortunate in that I max out an isa every year, what i am trying to do is maximise what i get that i cannot put into an isa for that year, like several bonds/fixed term accounts etc i have

is it better to diversify and have lots of small amounts going to lots of higher interest savings accounts, which ultimately = more interest in the long run

apologies if this makes no sense, but its a question/idea i cant quite crunch the numbers on

Where are you getting £152 from 🤔

Timing of the payments into the account is a factor but I can't see how you get much more than ~£135 from the first direct regular saver paying 7%.

Assuming you don't mind doing the (not particularly onerous) legwork moving money or setting up standing orders etc then why wouldn't you go for the highest interest rate?

Five accounts each paying 6-7% on say £200 is surely better than one with £1,000 in paying 5%?

0 -

Oh no. This is a new way of communicating misleading information about Regular Saver accounts 😤You are aware with regular saver (RS) accounts, the full interest is only applicable to half the total amount?

It would be far more helpful to refer people to the MSE Regular Saver calculator so they can work out themselves how much they can earn.

https://www.moneysavingexpert.com/savings/savings-calculator/

7 -

Interest is calculated daily, based on the amount of of money in the account at the end of a day and the interest rate of the account.a better explanation might be, by the end of the year you will have £3600 in the account. But until that point you don't have the full £3600 in the savings account. If you had the full £3600 in the account for the whole year at 5%, you would get £180 interest. But as you are building up to £3600, the interest is only applicable to the amount in the account at that time.So for the 1st month, interest would be applied to £300. (5% of £300 divided by 12 for the one month it has been in the account).In the 2nd month, the interest would be applied to £600. (5% of £600 divided by 12. You then add this interest to the interest from the 1st month to keep a running total.In the 3rd mont, the interest would be applied to £900. (5% of £900 divided by 12. You then add to the first 2 months to keep a running total.I think this explanation is right and hope it helps.

Accrued interest is credited to the account either monthly or annually, depending on the available / chosen frequency. For most Regular Savers, the only time interest will be added is at time of maturity, which is usually annually. Most Regular Savers will not show the accrued interest until it gets credited.0 -

Read this article

https://www.moneysavingexpert.com/savings/best-regular-savings-accounts/

And use the drip feeding calculator that it links to, to do your calculations.

Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.3 -

Just a thought, if ISAs are all full and there's a fair amount of money going in this year, 6 account at £200 per month and this isn't a new trend and/or will continue, depending on other income, tax on savings might become an issue. So it becomes time to look at nett amounts, then run the comparator against premium bonds and gilts0

-

Ooh that calculator is interesting!kimwp said:Read this article

https://www.moneysavingexpert.com/savings/best-regular-savings-accounts/

And use the drip feeding calculator that it links to, to do your calculations.0 -

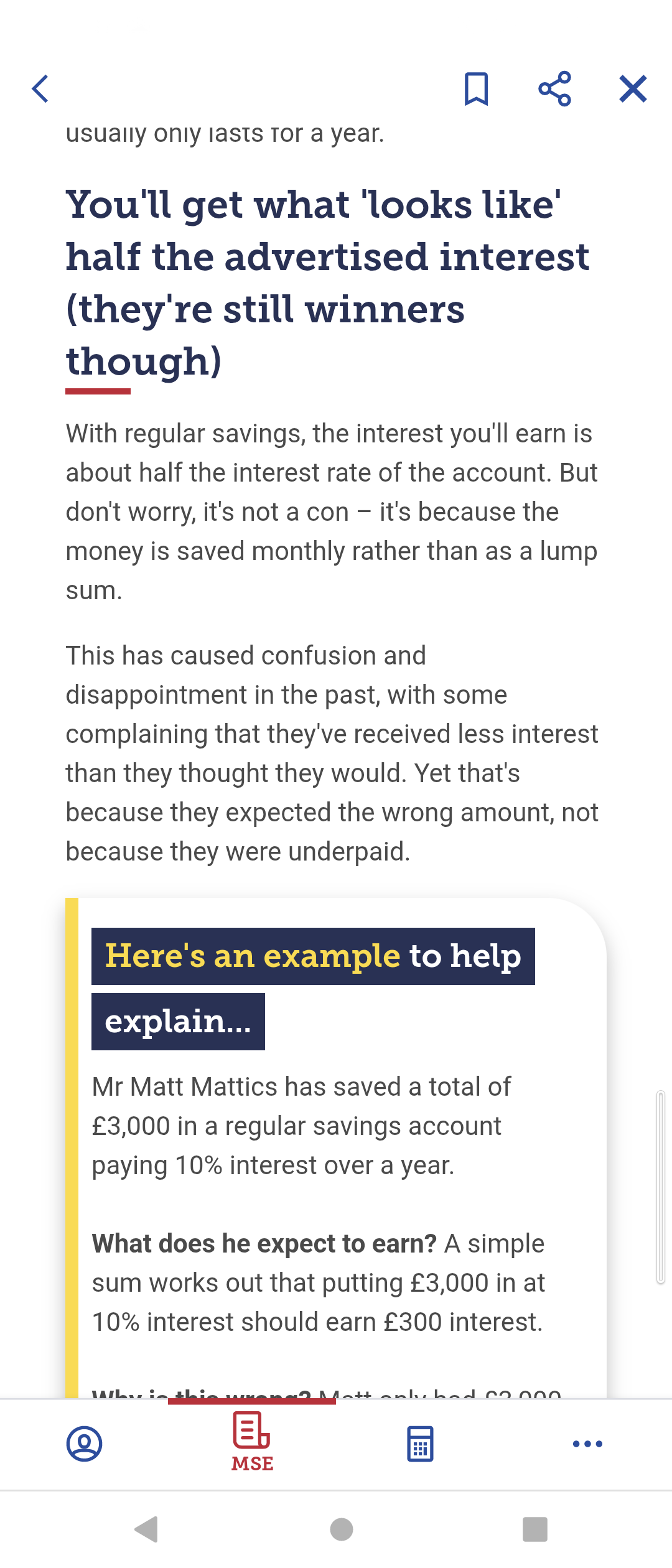

That article still describes it wrong, though, by saying the interest you'll earn is about half the interest rate of the accountYorkie1 said:

Ooh that calculator is interesting!kimwp said:Read this article

https://www.moneysavingexpert.com/savings/best-regular-savings-accounts/

And use the drip feeding calculator that it links to, to do your calculations.

I consider myself to be a male feminist. Is that allowed?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.7K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards