We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Last minute indecision about taking defined benefits pension

Comments

-

I will add a “thanks for the thank you” - there are a lot of helpful folk on this forum who post considered replies, some very wise people: mine are but an opinion, but it is nice to feel they have perhaps helped someone, & even nicer to have that noted!Carefulspender1 said:@dunstonh @p00hsticks @Marcon @Sarahspangles @molerat @[Deleted User] @cfw1994 I just want to say thank you to everyone who has replied here - I was having a real wobble about my decision and you have all set my mind at ease that I have already made the right decision. So thank you to all of you for taking time out of your day to answer my questions

Enjoy your retirement 😎👍Plan for tomorrow, enjoy today!3 -

I think you made the right decision. I have a DB pension and the monthly cheque that doesn't depend on the stock market is very welcome. You need a well researched asset allocation and the commitment to manage your money carefully if you are going to do drawdown and that can be very difficult when markets are volatile.And so we beat on, boats against the current, borne back ceaselessly into the past.2

-

We’ve read this so many times and glad the OP got value from the replies.

I understand the mindset though. If you are working with figures of £160 a month vs £65k (if they were up to date) it takes a leap to get your head around it. Especially depending on your personal circumstances, which is probably the most important factor. Once you establish you can’t (easily) get your hands on anything other than the £160 a month it makes things easier.1 -

Thank you for your comment Cobbler tone- yes it was looking at the amounts and thinking "why did I not take the money on a transfer" that made me have this wobble at the last minute. I have to say having slept on it I feel even more certain that I made the right decision, and that's down to the responses of the kind people on here. 😊Cobbler_tone said:We’ve read this so many times and glad the OP got value from the replies.

I understand the mindset though. If you are working with figures of £160 a month vs £65k (if they were up to date) it takes a leap to get your head around it. Especially depending on your personal circumstances, which is probably the most important factor. Once you establish you can’t (easily) get your hands on anything other than the £160 a month it makes things easier.2 -

Thanks Bostonerimus1, that's so true - I feel more comfortable at the idea of not having the stress of managing investments.Bostonerimus1 said:I think you made the right decision. I have a DB pension and the monthly cheque that doesn't depend on the stock market is very welcome. You need a well researched asset allocation and the commitment to manage your money carefully if you are going to do drawdown and that can be very difficult when markets are volatile.0 -

This is so true. I am grateful that my DB pension will arrive monthly for the rest of my life and is also fully indexed linked. That plus my state pension and a small annuity means I can enjoy my retirement without being unduly worried about how to manage financially.Carefulspender1 said:

Thanks Bostonerimus1, that's so true - I feel more comfortable at the idea of not having the stress of managing investments.Bostonerimus1 said:I think you made the right decision. I have a DB pension and the monthly cheque that doesn't depend on the stock market is very welcome. You need a well researched asset allocation and the commitment to manage your money carefully if you are going to do drawdown and that can be very difficult when markets are volatile.1 -

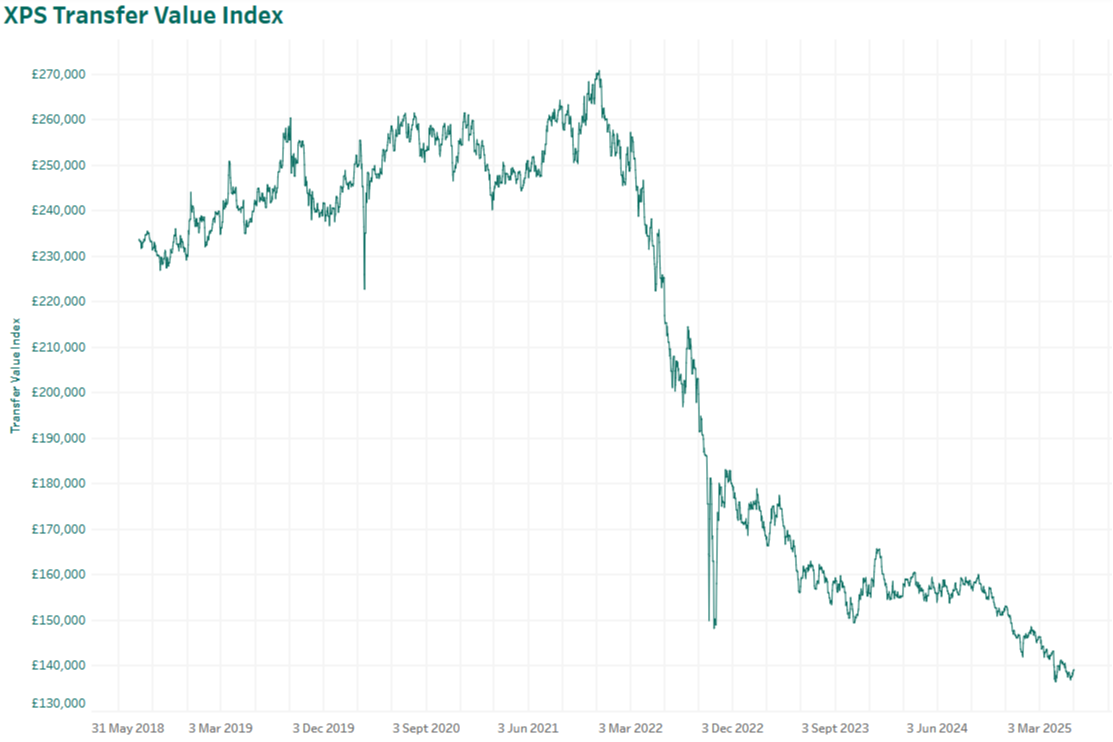

CETV are at multi year lows at the moment.

1 -

The above graph should further ease the mind of the OP. A sensible decision was made.1

-

Sarahspangles said:Remember you can pay £2,880 into a personal pension/SIPP even if you have no income and receive a tax relief top up of £720. It’s a way of boosting return on savings. If you draw it down in a year you’re not receiving enough income to use your personal allowance, you can draw it tax free.Excellent thread. I have been undecided about taking my DB for a year, but think Im going down the same route asap.I thought you werent supposed to pay any money you get from a pension, back into another pension fund to get another tax-free top-up ?0

-

Not pension recycling if under £7500Mr_Benn said:Sarahspangles said:Remember you can pay £2,880 into a personal pension/SIPP even if you have no income and receive a tax relief top up of £720. It’s a way of boosting return on savings. If you draw it down in a year you’re not receiving enough income to use your personal allowance, you can draw it tax free.Excellent thread. I have been undecided about taking my DB for a year, but think Im going down the same route asap.Arent you not supposed to pay any money you get from a pension back into another pension fund to get another tax-free top-up ?I’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards