We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Help understanding NHS pension for someone who has always been (sort of) self employed

SomeMadeUpName

Posts: 373 Forumite

Hello

I've popped up again to leverage the experience on here to compensate for our ignorance in pension matters.

Some background (and I will get to the NHS bit eventually):

1 - Myself and my missus have always been self employed, or directors of our own businesses.

2 - As a result of being daft really we got to our mid 50's with nil pension funds save for an NI contracted out fund of circa £60k in my name. We do however have a decent property investment portfolio, so I'm not here crying the poor tale, just bemoaning not being a savvy as we could have.

3 - Since waking up (and joining this forum) we've spent a few years making contributions to private pensions and now we are at £25k for my wife and £30k for me (unfortunately we are limited by quite small earned income each year). We are now what you'd call late 50's I guess.

4 - The plan going forward was to continue working our ltd co and ramp salaries upto to circa £12k then make pension contributions of £12k (£9.6k net) each also to boost the funds up another £100k over the next 4yrs. Hope there is further profit in the Co to make direct pension contribs from there also.

Problem with all of the above is having enough profit to do the above and have something to live on. So a couple of weeks ago the missus decided she should go look for further work.

So now she has 2no offers, which are very different but both allow her the flexibility to ramp work up and down, allowing her to spend enough time overseas to justify the money we have tied up in a property in France.

One is working for a rental property manager. A strong advantage here is that they would like her to just invoice through our consulting business. This puts the funds in the company where we can (within limits) play tunes on how it is drawn (tax/pension advantageous salary level, dividend, direct pension contribution). The hourly rate would be set at a level that reflects no holiday pay, lack of employment rights, no employer pension contrib, etc etc).

The other is an NHS job (now we get to it). Pay is NMW, it's a zero hours, theoretically short term, contract. Technically though she joins the NHS 2015 pension, additionally, so long as they like her then why would the contract end, they are constantly looking for admin peeps to fill the roles.

So to help decide we need to understand the NHS pension, and defined benefit schemes are all new to us.

My understanding (which could be way off):

She works, as a low earner (NMW & limited hrs) she pays about 6% in, they pay about 24% in, but it all goes into a general pot. IF she gets 2 yrs of work for the NHS in then she is then entitles to benefits from the scheme of 1/54 of her annual NHS income for each year (plus reval'n, and other technicalities, but essentially that). It might take her longer than 2 yrs to get to 2 yrs, as if she works literally zero hours in a week then she might count as suspended for 'vesting'.

If she doesn't get 2 years in then she can get back her 6%'ish, but the 24%'ish is lost into the general pot. If that happens the value seems really rubbish tbh.

If she does get 2 years in, then she can draw the pension at 67, and she could buy further entitlement in units of £250 (additional pension income) for a price firmed up at the point of application.

Questions are:

Does that look about right?

Is the earned NHS pension (should she ever get one) as great a value as everyone says?

Are the purchased additional contributions good value too?

My feeling is that even though the amount she might get will never add up to a big pension income (unless we maybe buy more) then given everything else we have is defined contribution (in actuality or de facto) then it might be a good thing to have alongside full new state pension (which we both have paid up already).

But all that depends on whether my understanding is correct, so.....

Many thanks for any input.

I've popped up again to leverage the experience on here to compensate for our ignorance in pension matters.

Some background (and I will get to the NHS bit eventually):

1 - Myself and my missus have always been self employed, or directors of our own businesses.

2 - As a result of being daft really we got to our mid 50's with nil pension funds save for an NI contracted out fund of circa £60k in my name. We do however have a decent property investment portfolio, so I'm not here crying the poor tale, just bemoaning not being a savvy as we could have.

3 - Since waking up (and joining this forum) we've spent a few years making contributions to private pensions and now we are at £25k for my wife and £30k for me (unfortunately we are limited by quite small earned income each year). We are now what you'd call late 50's I guess.

4 - The plan going forward was to continue working our ltd co and ramp salaries upto to circa £12k then make pension contributions of £12k (£9.6k net) each also to boost the funds up another £100k over the next 4yrs. Hope there is further profit in the Co to make direct pension contribs from there also.

Problem with all of the above is having enough profit to do the above and have something to live on. So a couple of weeks ago the missus decided she should go look for further work.

So now she has 2no offers, which are very different but both allow her the flexibility to ramp work up and down, allowing her to spend enough time overseas to justify the money we have tied up in a property in France.

One is working for a rental property manager. A strong advantage here is that they would like her to just invoice through our consulting business. This puts the funds in the company where we can (within limits) play tunes on how it is drawn (tax/pension advantageous salary level, dividend, direct pension contribution). The hourly rate would be set at a level that reflects no holiday pay, lack of employment rights, no employer pension contrib, etc etc).

The other is an NHS job (now we get to it). Pay is NMW, it's a zero hours, theoretically short term, contract. Technically though she joins the NHS 2015 pension, additionally, so long as they like her then why would the contract end, they are constantly looking for admin peeps to fill the roles.

So to help decide we need to understand the NHS pension, and defined benefit schemes are all new to us.

My understanding (which could be way off):

She works, as a low earner (NMW & limited hrs) she pays about 6% in, they pay about 24% in, but it all goes into a general pot. IF she gets 2 yrs of work for the NHS in then she is then entitles to benefits from the scheme of 1/54 of her annual NHS income for each year (plus reval'n, and other technicalities, but essentially that). It might take her longer than 2 yrs to get to 2 yrs, as if she works literally zero hours in a week then she might count as suspended for 'vesting'.

If she doesn't get 2 years in then she can get back her 6%'ish, but the 24%'ish is lost into the general pot. If that happens the value seems really rubbish tbh.

If she does get 2 years in, then she can draw the pension at 67, and she could buy further entitlement in units of £250 (additional pension income) for a price firmed up at the point of application.

Questions are:

Does that look about right?

Is the earned NHS pension (should she ever get one) as great a value as everyone says?

Are the purchased additional contributions good value too?

My feeling is that even though the amount she might get will never add up to a big pension income (unless we maybe buy more) then given everything else we have is defined contribution (in actuality or de facto) then it might be a good thing to have alongside full new state pension (which we both have paid up already).

But all that depends on whether my understanding is correct, so.....

Many thanks for any input.

0

Comments

-

Let's address that one, not least because it's an easy answer:SomeMadeUpName said:Hello

I've popped up again to leverage the experience on here to compensate for our ignorance in pension matters.

Some background (and I will get to the NHS bit eventually):

1 - Myself and my missus have always been self employed, or directors of our own businesses.

2 - As a result of being daft really we got to our mid 50's with nil pension funds save for an NI contracted out fund of circa £60k in my name. We do however have a decent property investment portfolio, so I'm not here crying the poor tale, just bemoaning not being a savvy as we could have.

3 - Since waking up (and joining this forum) we've spent a few years making contributions to private pensions and now we are at £25k for my wife and £30k for me (unfortunately we are limited by quite small earned income each year). We are now what you'd call late 50's I guess.

4 - The plan going forward was to continue working our ltd co and ramp salaries upto to circa £12k then make pension contributions of £12k (£9.6k net) each also to boost the funds up another £100k over the next 4yrs. Hope there is further profit in the Co to make direct pension contribs from there also.

Problem with all of the above is having enough profit to do the above and have something to live on. So a couple of weeks ago the missus decided she should go look for further work.

So now she has 2no offers, which are very different but both allow her the flexibility to ramp work up and down, allowing her to spend enough time overseas to justify the money we have tied up in a property in France.

One is working for a rental property manager. A strong advantage here is that they would like her to just invoice through our consulting business. This puts the funds in the company where we can (within limits) play tunes on how it is drawn (tax/pension advantageous salary level, dividend, direct pension contribution). The hourly rate would be set at a level that reflects no holiday pay, lack of employment rights, no employer pension contrib, etc etc).

The other is an NHS job (now we get to it). Pay is NMW, it's a zero hours, theoretically short term, contract. Technically though she joins the NHS 2015 pension, additionally, so long as they like her then why would the contract end, they are constantly looking for admin peeps to fill the roles.

So to help decide we need to understand the NHS pension, and defined benefit schemes are all new to us.

My understanding (which could be way off):

She works, as a low earner (NMW & limited hrs) she pays about 6% in, they pay about 24% in, but it all goes into a general pot. IF she gets 2 yrs of work for the NHS in then she is then entitles to benefits from the scheme of 1/54 of her annual NHS income for each year (plus reval'n, and other technicalities, but essentially that). It might take her longer than 2 yrs to get to 2 yrs, as if she works literally zero hours in a week then she might count as suspended for 'vesting'.

If she doesn't get 2 years in then she can get back her 6%'ish, but the 24%'ish is lost into the general pot. If that happens the value seems really rubbish tbh.

If she does get 2 years in, then she can draw the pension at 67, and she could buy further entitlement in units of £250 (additional pension income) for a price firmed up at the point of application.

Questions are:

Does that look about right?

Is the earned NHS pension (should she ever get one) as great a value as everyone says?

Are the purchased additional contributions good value too?

My feeling is that even though the amount she might get will never add up to a big pension income (unless we maybe buy more) then given everything else we have is defined contribution (in actuality or de facto) then it might be a good thing to have alongside full new state pension (which we both have paid up already).

But all that depends on whether my understanding is correct, so.....

Many thanks for any input. Source: https://www.nhsbsa.nhs.uk/sites/default/files/2024-08/Leaving%20Early%20and%20Transferring%20Out%20Guide%20%28V17A%29%2004.2024.pdf

Source: https://www.nhsbsa.nhs.uk/sites/default/files/2024-08/Leaving%20Early%20and%20Transferring%20Out%20Guide%20%28V17A%29%2004.2024.pdf

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1 -

As directors of ltd company, you shouldn't be making personal contributions to your pension, do company contributions instead, it's more tax efficient and you aren't limited by the income you pay yourself anymore but the 60k AA limit instead.1

-

No mention of your sate pension there, how is that doing ? IRO £12K pa each is not to be sniffed at.1

-

Thx for the input. I'm across direct contribution above a certain amountNoMore said:As directors of ltd company, you shouldn't be making personal contributions to your pension, do company contributions instead, it's more tax efficient and you aren't limited by the income you pay yourself anymore but the 60k AA limit instead.

BUT

If we pay ourselves £12k each, there is no employee NI, the employer NI us claimed back by the Co as a small employer. As interest rates have scuppered our rent incomes (until I get restructured anyway) there is no income tax to pay. We then put £9.6k into the SIPP and HMRC add £2.4k, we are then £2.4k ahead. If there is more profit in the Co after the 2x£12k then we would use direct contribution. And if the missus takes the NHS contribution she would use that income and not get the £12k from the company*.

*Although now I've said that out loud: Maybe she would, as the NI piece still holds true, she then pays 20% taxed sure, but then uses the net to go into SIPP, it turns back into £12k and gets tax free growth and 25% tax free withdrawal**.

I think...........

**But then there is no advantage there over direct contribution from the Co, so simpler to go with that.0 -

Oh no, state pension forms a big part of our planning. I bought 2 years for the wife just after Covid as I was convinced the UK Gov would have to put voluntary NI contribs up to help cover the cost of the Covid support schemes. I did mention it, but rather buried it in the last multi line para of the post. Atm state pension is the only 'guaranteed' provision we have.molerat said:No mention of your sate pension there, how is that doing ? IRO £12K pa each is not to be sniffed at.1 -

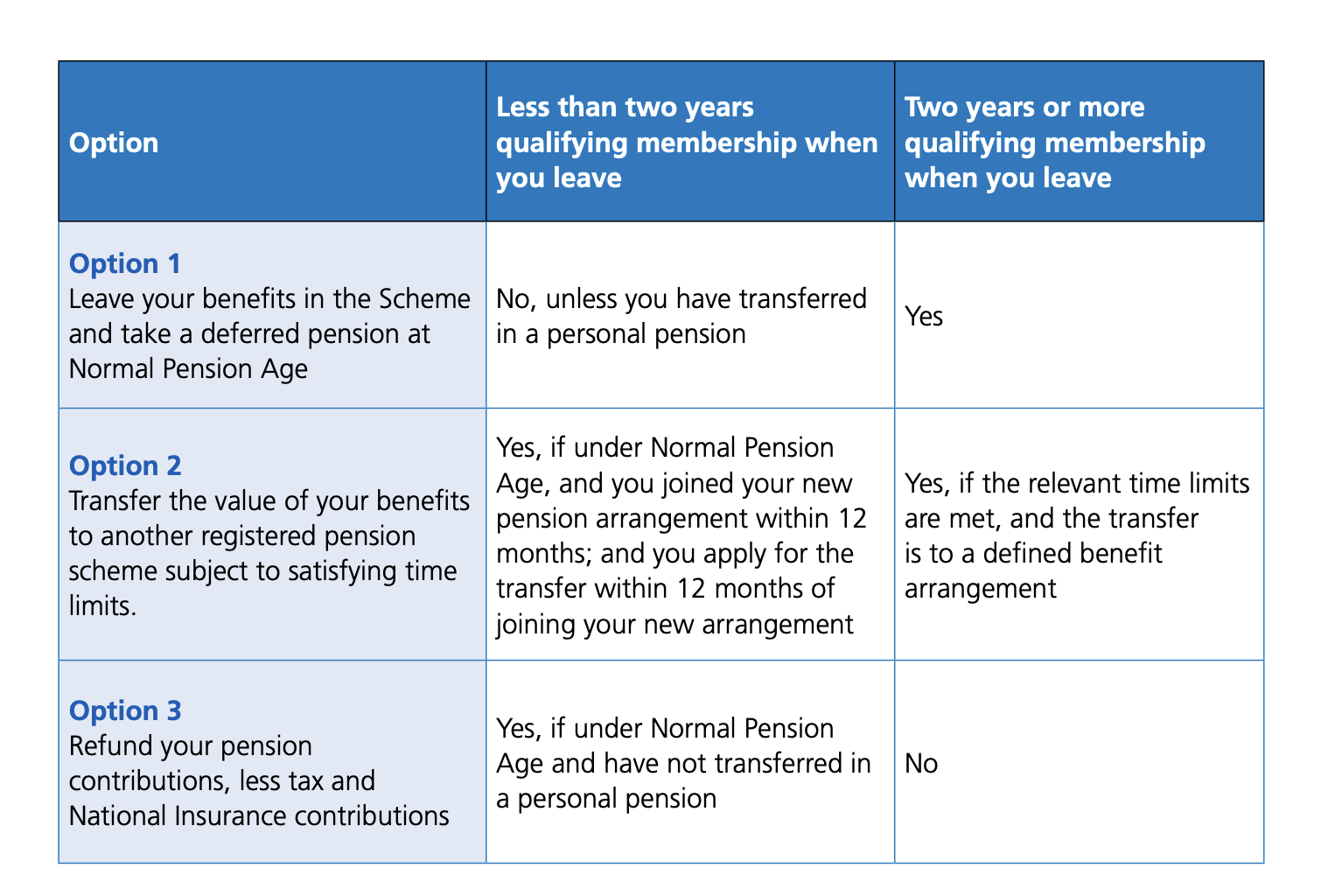

So if I'm reading the above correctly then you can transfer out the 'value' of the NHS pension (so 'sort of' both the employer and employee contributions) to a personal pension, but it has to be one that requires purchase of an annuity as opposed to a flexi draw down?Let's address that one, not least because it's an easy answer:Source: https://www.nhsbsa.nhs.uk/sites/default/files/2024-08/Leaving%20Early%20and%20Transferring%20Out%20Guide%20%28V17A%29%2004.2024.pdf

In theory sounds a lot less poor, though in reality how worthwhile it will be if the pot is really small, which it would be if you were sub 2 years on limited hours at NMW.

Am I getting that right though?0 -

It's going to be vastly better than the alternative (ie NOT joining the NHS scheme). You can only transfer out from the NHS scheme to a personal pension if you have under two years of NHS pension scheme membership - and the transfer value is likely to be higher than you might think, especially as your wife is in her mid/late 50s.SomeMadeUpName said:

So if I'm reading the above correctly then you can transfer out the 'value' of the NHS pension (so 'sort of' both the employer and employee contributions) to a personal pension, but it has to be one that requires purchase of an annuity as opposed to a flexi draw down?Let's address that one, not least because it's an easy answer:Source: https://www.nhsbsa.nhs.uk/sites/default/files/2024-08/Leaving%20Early%20and%20Transferring%20Out%20Guide%20%28V17A%29%2004.2024.pdf

In theory sounds a lot less poor, though in reality how worthwhile it will be if the pot is really small, which it would be if you were sub 2 years on limited hours at NMW.

Am I getting that right though?

Over two years and she has the benefit of a modest NHS pension. No personal pension can 'require' the purchase of annuity, so once she's beyond the two year mark, any transfer would have to be to a defined benefit pension.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1 -

OK, that's great info thx.Marcon said:

It's going to be vastly better than the alternative (ie NOT joining the NHS scheme). You can only transfer out from the NHS scheme to a personal pension if you have under two years of NHS pension scheme membership - and the transfer value is likely to be higher than you might think, especially as your wife is in her mid/late 50s.SomeMadeUpName said:

So if I'm reading the above correctly then you can transfer out the 'value' of the NHS pension (so 'sort of' both the employer and employee contributions) to a personal pension, but it has to be one that requires purchase of an annuity as opposed to a flexi draw down?Let's address that one, not least because it's an easy answer:Source: https://www.nhsbsa.nhs.uk/sites/default/files/2024-08/Leaving%20Early%20and%20Transferring%20Out%20Guide%20%28V17A%29%2004.2024.pdf

In theory sounds a lot less poor, though in reality how worthwhile it will be if the pot is really small, which it would be if you were sub 2 years on limited hours at NMW.

Am I getting that right though?

Over two years and she has the benefit of a modest NHS pension. No personal pension can 'require' the purchase of annuity, so once she's beyond the two year mark, any transfer would have to be to a defined benefit pension.

So if the job doesn't work out, she transfers out and get's what might be a poorer return (than the NHS 'annuity') but with greater flexibility as compensation.

If the job works out she goes past two years and gets access the NHS pension benefits, with the possibility of buying more income if we choose to purchase more certainty in retirement.0 -

Or if you got personal pension, transfer it in and don't have to worry about two years limit.3

-

Hi, so yes, I saw that, so....JoeCrystal said:Or if you got personal pension, transfer it in and don't have to worry about two years limit.

If she starts work and then gets a few small payments into the scheme under her belt. She can then transfer in all (or a portion of) her personal pension and that buys her more income in retirement, and by doing that she also 'vests' her entitlement early?

Is that right?

And I assume it's also pretty good value in terms of return (early demise excepted)!0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards