We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Look at my DIY plan, comments suggestions and criticism welcome

Comments

-

0

-

Actually it has been much better for a while! Not exactly 'prohibitively expensive'. Unless you think you should be getting double digits annuity then that is just very unrealistic goal.ali_bear said:I looked again at some annuity quotes - prohibitively expensive!0 -

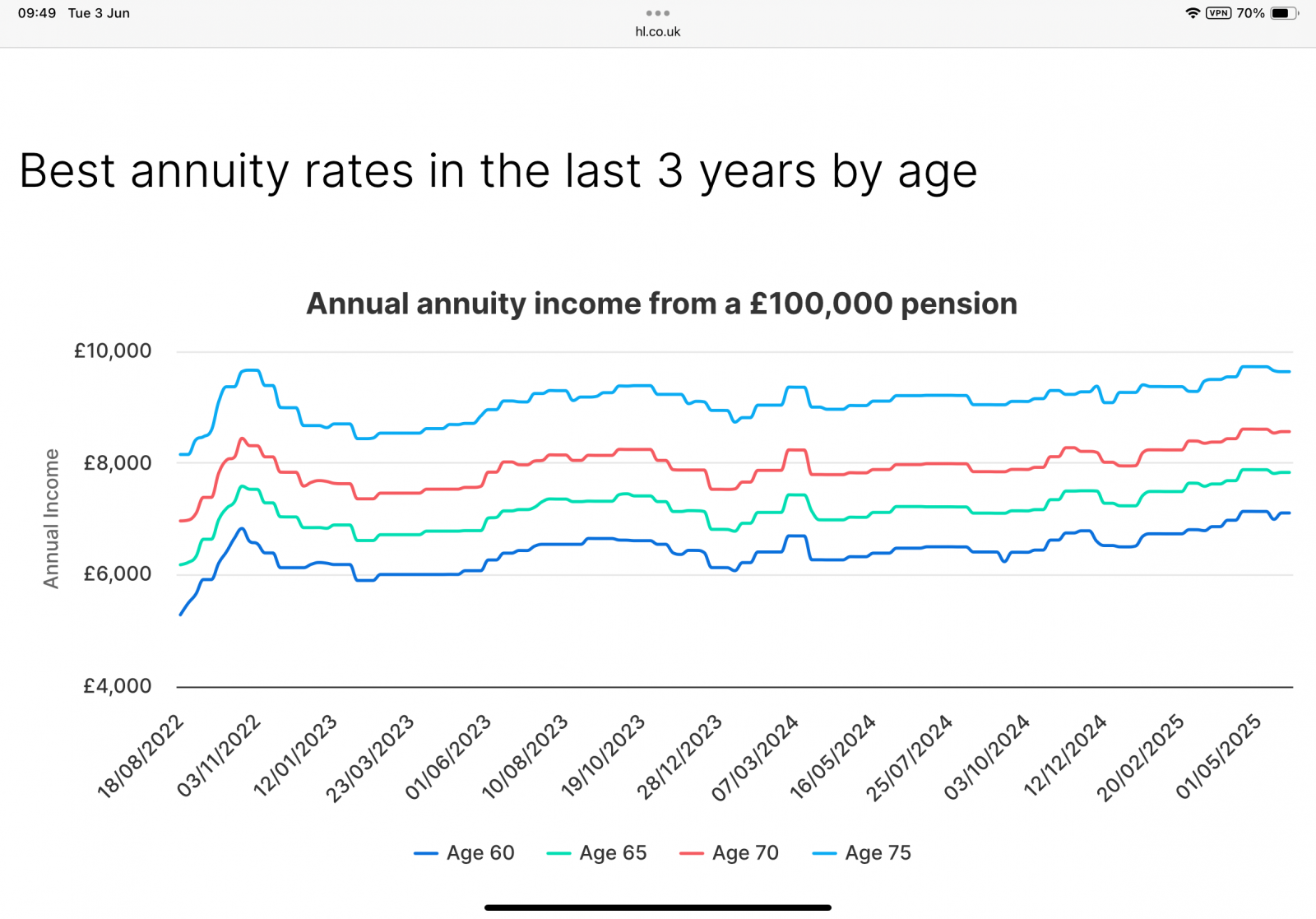

I'm doing annuities like hotcakes. They are great value at the moment and are at 18 year highs.ali_bear said:I looked again at some annuity quotes - prohibitively expensive!I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.7 -

Leaving aside any fixed term annuity, if I was to buy a single life RPI linked at age 60. What income do you think I should be aiming for from that? Or alternatively what proportion of my DC fund should I spend on it. How do you decide on that?A little FIRE lights the cigar0

-

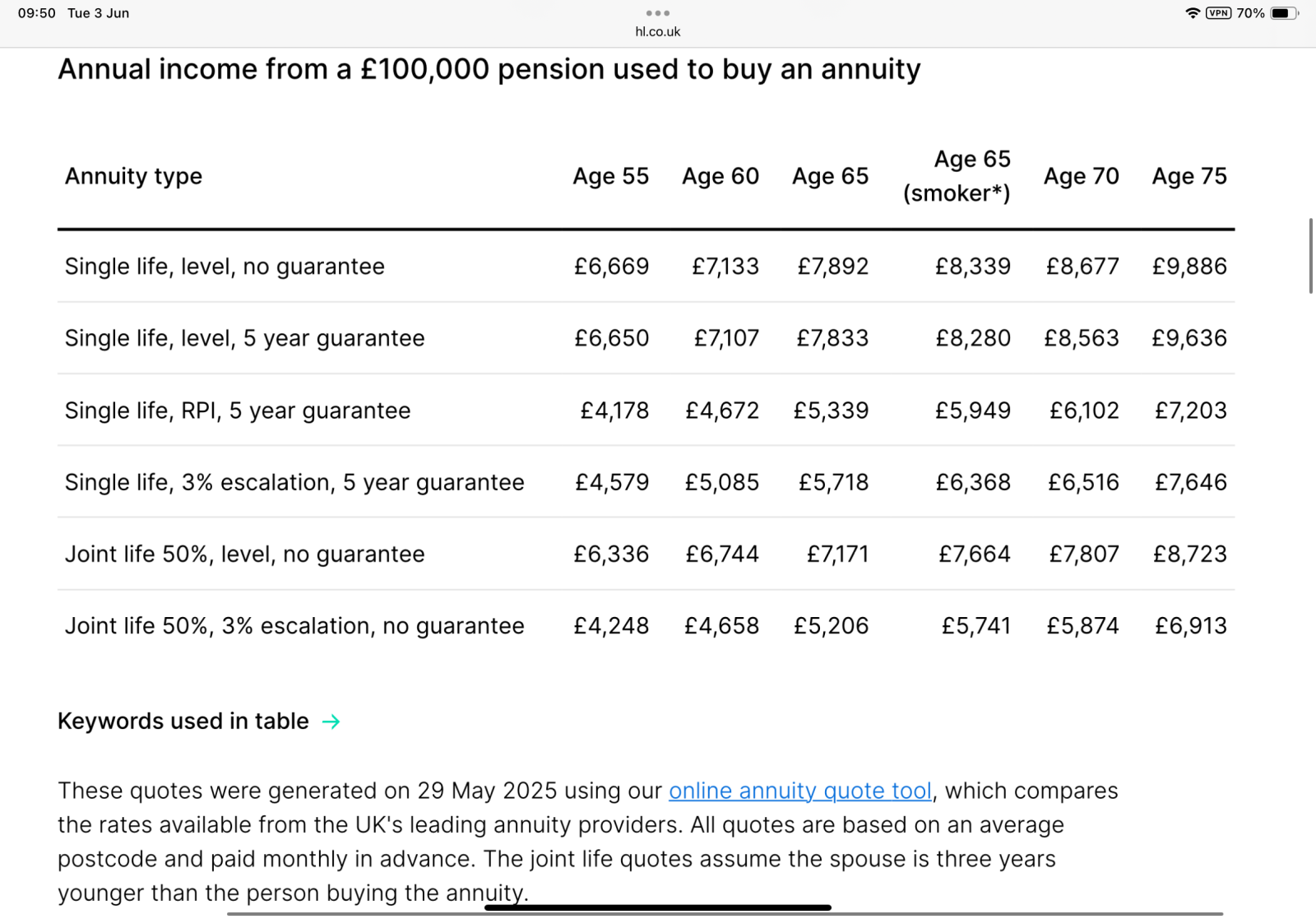

£750k buys 7.5 x £4,672 = £35,040 based on my table above.ali_bear said:Leaving aside any fixed term annuity, if I was to buy a single life RPI linked at age 60. What income do you think I should be aiming for from that? Or alternatively what proportion of my DC fund should I spend on it. How do you decide on that?

Work out how much you need or want and adjust accordingly.0 -

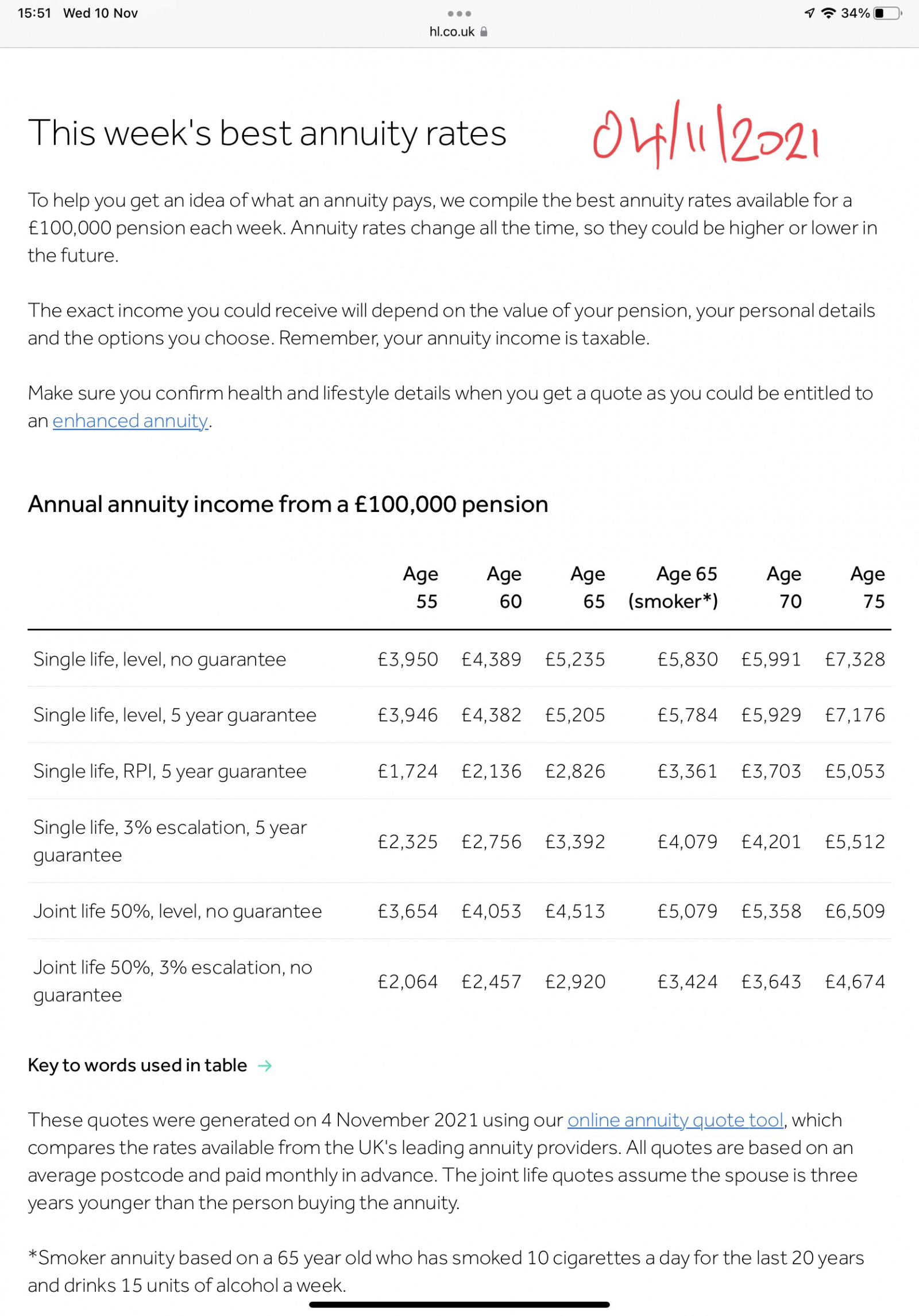

And for interest, compare the rates above to what you could have bought in November 2011.

2 -

I know that rates were depressed for a long period. Possibly now they have returned to the new normal. But even if rates are good I am surprised to be recommended to put so much into one.A little FIRE lights the cigar0

-

Just buy the guaranteed income you need. You could always annuitise the lot (after taking PCLS) and if it is too much, add it to an ISA which can hold the same investments as your DC pension.ali_bear said:I know that rates were depressed for a long period. Possibly now they have returned to the new normal. But even if rates are good I am surprised to be recommended to put so much into one.

I bought an annuity with 70% of my DC pot in 2023 and rates are now even better I am considering annuitising the rest. If you have won the game, why keep your cards on the table?

Any excess which is unspent will go into an ISA.

EDIT : inheritance tax on pension pots from 2027 are also forcing this decision and an annuity makes it easier to give away money from an actual income with no inheritance tax worry.2 -

Also consider that investment returns for a period have been abnormal. Easy to become accustomed to something and assume it will always be this way.ali_bear said:I know that rates were depressed for a long period. Possibly now they have returned to the new normal. But even if rates are good I am surprised to be recommended to put so much into one.1 -

So at those rates I could get an income of 14k for 300k, and it "breaks even" after about 21 years. That income plus my small DB and the state pension covers my monthly 2k. Nice.A little FIRE lights the cigar1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards