We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

I’m £50k in debt Scotland

chrisjvc1

Posts: 21 Forumite

Hi folks, I know this is all my own doing but after a difficult divorce I bought a small house that needed some work. To cut a long story short I now have 8 credit cards, with £17k of debt, most of which is on 0% for a year. I have 3 loans, one with 8k left, one with 7k left and one with 19k left. I earn £50k a year, I can just cover all my payments but have about £100 spare for food……I don’t want to loose my house but either I sell up or take out a 7 year loan for £29k which will mean I can pay off all my credit cards and 2 loans, this will take my payments for all that from £870 a month to £538 giving me some money to live on. Any advice please

0

Comments

-

Can you complete and post an SOA so we can get a more complete picture?

https://www.lemonfool.co.uk/financecalculators/soa.php1 -

I think it's optimistic to be thinking that you will get a 29k 7 year loan when you already have 51k of debt.

It's quite likely to be higher apr than your current loans and certainly higher than the 0% that your credit cards are at.

Put that idea on the back burner for now and we'll see if we can find a better one

Ps. You won't lose your house as long as you pay the mortgage.2 -

Consolidating bad debts is like pouring more petrol on a fire, in the vain hope it will go out, its not recommended.

I will be bold, and jump the gun slightly before seeing your SOA, because, unless your spending is way out of control on other things, that can be stopped, as a homeowner it will boil down to one of two choices, either you opt for the informal solution of debt management, where essential debts take priority, and what`s left from your disposable income go`s towards the non priority cards and loans etc.

Or you opt for the insolvency route via an IVA, a more formal solution that gives you legal protection from creditors taking further action against you.

With around 30k of debt, and a house to protect, either would be an option here.

Possibly the informal route would be best, creditors taking folks homes is mostly way in the past these days, as long as regular payments are made, things just trundle along as per normal.

You should put aside all thoughts of borrowing your way out of this, that`s not going to happen.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter1 -

You won't lose the house as long as you keep paying the mortgage and keep up the building insurance.

There are various options, let's see the SOA and we can make suggestions.

It might also be possible to increase you income say via the rent a room scheme?If you've have not made a mistake, you've made nothing1 -

[font=courier new][b]Statement of Affairs and Personal Balance Sheet[/b][b]Household Information[/b]Number of adults in household........... 1Number of children in household......... 0Number of cars owned.................... 1[b]Monthly Income Details[/b]Monthly income after tax................ 3049Partners monthly income after tax....... 0Benefits................................ 0Other income............................ 0[b]Total monthly income.................... 3049[/b][b]Monthly Expense Details[/b]Mortgage................................ 1005Secured/HP loan repayments.............. 0Rent.................................... 0Management charge (leasehold property).. 0Council tax............................. 145Electricity............................. 75Gas..................................... 75Oil..................................... 0Water rates............................. 0Telephone (land line)................... 0Mobile phone............................ 12TV Licence.............................. 15Satellite/Cable TV...................... 40Internet Services....................... 25Groceries etc. ......................... 280Clothing................................ 0Petrol/diesel........................... 200Road tax................................ 0Car Insurance........................... 45Car maintenance (including MOT)......... 0Car parking............................. 0Other travel............................ 0Childcare/nursery....................... 0Other child related expenses............ 150Medical (prescriptions, dentist etc).... 0Pet insurance/vet bills................. 0Buildings insurance..................... 23Contents insurance...................... 0Life assurance ......................... 0Other insurance......................... 0Presents (birthday, christmas etc)...... 10Haircuts................................ 20Entertainment........................... 0Holiday................................. 0Emergency fund.......................... 0[b]Total monthly expenses.................. 2120[/b][b]Assets[/b]Cash.................................... 0House value (Gross)..................... 163000Shares and bonds........................ 0Car(s).................................. 7000Other assets............................ 0[b]Total Assets............................ 170000[/b][b]Secured & HP Debts[/b]Description....................Debt......Monthly...APRMortgage...................... 144000...(1005).....5.1[b]Total secured & HP debts...... 144000....-.........- [/b][b]Unsecured Debts[/b]Description....................Debt......Monthly...APRSainsburys.....................4626......104.......0Natwest........................2934......75........0Bank of Scotland ..............3120......78........0Zopa...........................19000.....415.......11.2Nationwide.....................8523......189.......8Halifax .......................6327......189.......7.8Halifax........................287.......5.........0Nmba...........................2028......50........0Lloyds.........................1639......42........0Natiinwide.....................3141......60........0[b]Total unsecured debts..........51625.....1207......- [/b][b]Monthly Budget Summary[/b]Total monthly income.................... 3,049Expenses (including HP & secured debts). 2,120Available for debt repayments........... 929Monthly UNsecured debt repayments....... 1,207[b]Amount short for making debt repayments. -278[/b][b]Personal Balance Sheet Summary[/b]Total assets (things you own)........... 170,000Total HP & Secured debt................. -144,000Total Unsecured debt.................... -51,625[b]Net Assets.............................. -25,625[/b][i]Created using the SOA calculator at www.LemonFool.co.uk.Reproduced on Moneysavingexpert with permission, using other browser.[/i][/font]0

-

Nothing there is high interest so a consolidation loan is not a good idea.

Looks like a debt management plan will work for you.

No water charge - are you in Scotland?

I think you need to budget something for car maintenance, clothing and road tax (?)2 -

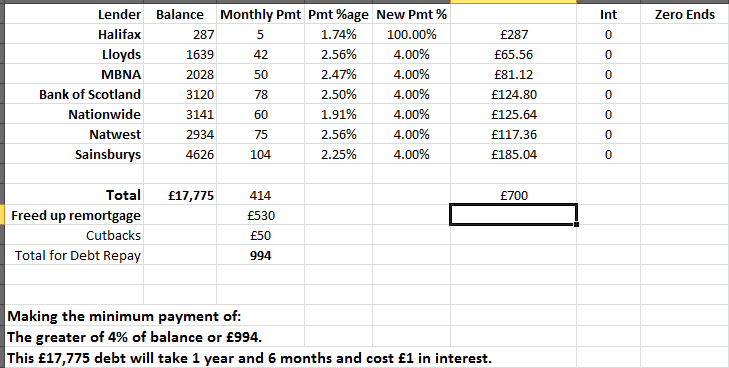

chrisjvc1 said:Hi folks, I know this is all my own doing but after a difficult divorce I bought a small house that needed some work. To cut a long story short I now have 8 credit cards, with £17k of debt, most of which is on 0% for a year. I have 3 loans, one with 8k left, one with 7k left and one with 19k left. I earn £50k a year, I can just cover all my payments but have about £100 spare for food……I don’t want to loose my house but either I sell up or take out a 7 year loan for £29k which will mean I can pay off all my credit cards and 2 loans, this will take my payments for all that from £870 a month to £538 giving me some money to live on. Any advice pleaseFirst of all, well done for recognising you have a problem and coming to get help, this is not always easy.Before deciding on a debt solution I think there needs to be some analysis of where the money went.I have had family and friends in London buy a flat to add a bedroom, it was the only way they could afford to get to a 2 bed flat to start a family. They both used up to 6 credit cards each to fund the development of the property and that was after they had saved up around £40k and cashed in ISA's etc. When one went to remortgage to pay off all this debt (as property value was not £250k higher) the bank refused the mortgage because apparently they do not like to use a mortgage for this purpose. 6 months later they went to a broker who got them a deal to remortgage and they paid off every penny of debt, even the zero percent.House value (Gross)..................... 163000Mortgage....................................... 144000Therefore if your debt was 90% spent on the property and the property now has a higher value then I would suggest a remortgage, even if you have to pay above the going rate. However, unless you were quoting the old house valuation then it seems as if this was a money pit and you made poor decisions on developers.If we consider that theAmount short for making debt repayments. -278and you do only have around £20,000 of equity then the simple solution is to remortgage the house, pay off the Zopa thus reducing your outgoings by £415Zopa...........................19000.....415.......11.2This would give you an extra £137 a month to attack the Nationwide and HalifaxNationwide.................8523......189.......8Halifax .......................6327......189.......7.8If now that you have done up the house worth more you could add and extra £15k and pay off the Nationwide and Halifax too.This would release a further £398 a month so an extra £530 a month to pare down your zero percent debt.If you use can remortgage and then use this £530 you could have the whole debt paid off in 18 months

If you had the dates when the zero rate expires it would be possible to reorder the cards so that you pay off the ones that have debt expiring first.If remortgage is NOT and option then let's work through other options, but first consider the ROOT CAUSE of the debt.If the Zopa debt for example was to already consolidate previous overspending then I think you need to address that problem. There is no judgement here, many people have gambling habits, paying of an Ex's debt and so on. What you need to know is whether the root cause could happen again?Normally the way I would approach an SOA like yours is on how much disposable income you have without debt and yours seems pretty healthy.So the next question is whether you mind trashing your credit record for 6 years to get a reduced rate on this debt?If the answer to that is that you want to preserve your credit record then there are two things to check,1. Is there any discount for early repayment of any loan?2. How much credit do you have on the zero percent cards and3, When do the zero rate expire.If there is some capacity on the zero percent cards and there is a discount for early repayment then it makes sense to use that capacity to reduce the debts that are costing you the most. You do this by putting your monthly spending of bills & food on the zero percent card and then each day move what you spent on the zero card to a savings account and then pay those accumulated amounts from the savings to the debt with the highest interest rate (if you benefit from early repayment).The three that stand out areZopa...........................19000......415.......11.2Nationwide...................8523......189.........8Halifax .........................6327......189........7.8

If you had the dates when the zero rate expires it would be possible to reorder the cards so that you pay off the ones that have debt expiring first.If remortgage is NOT and option then let's work through other options, but first consider the ROOT CAUSE of the debt.If the Zopa debt for example was to already consolidate previous overspending then I think you need to address that problem. There is no judgement here, many people have gambling habits, paying of an Ex's debt and so on. What you need to know is whether the root cause could happen again?Normally the way I would approach an SOA like yours is on how much disposable income you have without debt and yours seems pretty healthy.So the next question is whether you mind trashing your credit record for 6 years to get a reduced rate on this debt?If the answer to that is that you want to preserve your credit record then there are two things to check,1. Is there any discount for early repayment of any loan?2. How much credit do you have on the zero percent cards and3, When do the zero rate expire.If there is some capacity on the zero percent cards and there is a discount for early repayment then it makes sense to use that capacity to reduce the debts that are costing you the most. You do this by putting your monthly spending of bills & food on the zero percent card and then each day move what you spent on the zero card to a savings account and then pay those accumulated amounts from the savings to the debt with the highest interest rate (if you benefit from early repayment).The three that stand out areZopa...........................19000......415.......11.2Nationwide...................8523......189.........8Halifax .........................6327......189........7.8

If Zopa is a fixed rate loan and does not cost less if you pay off early then Nationwide and/or Halifax would be where you spend it, assuming they too reduce.If neither reduce then still use up your credit limit but use the money to pay off the zero percent that ends earliest. This will reduce the risk of you having to pay 24% when an offer expires and you are deemed over extended and can't transfer to another zero percent card.On personal spending these are the areas to question:Water rates............................... 0 ----> This should be payableMobile phone.......................... 12----> Switch to Lebara £3 month dealTV Licence.............................. 15 ----> £0 Dump BBC & Live TVSatellite/Cable TV.................... 40 ---> Dump all pay TVGroceries etc. ....................... 280 ----> Try to cut this by 20% minimum

Petrol/diesel........................... 200 ---->Road tax.................................... 0 ----> Is this another omission, how can you spend £200 on petrol but £0 on this?Haircuts................................... 20 ----> Get a trimmer for £18 at Tesco

If you were going to DMP your debt then you might take a different approach and pare down your mortgage with any spare cash but that would be a bit of a dodgy thing to do. You are not in that desperate a state yet.

DMP will trash your credit record but you should be able to remortgage at variable rate with existing lender when the promotion rate expires (or that may have happened). If your mortgage discount has reverted it would be a good reason to remortgage as rates are coming down.

0 -

Could you get a lodger? When i got divorced i let out a room. You can get up to £7500 tax free and it costs you very little. Obviously you need the space to do it but it helped me pay off my debts.1

-

Even if full-time isn't an option there are folk looking for Monday to Thursday. And others moving jobs looking for short-term until they can find a rental or to fulfil a short-term contract.Green_hopeful said:Could you get a lodger? When i got divorced i let out a room. You can get up to £7500 tax free and it costs you very little. Obviously you need the space to do it but it helped me pay off my debts.If you've have not made a mistake, you've made nothing0 -

It’s difficult to know what to do next.DankVielen said:chrisjvc1 said:Hi folks, I know this is all my own doing but after a difficult divorce I bought a small house that needed some work. To cut a long story short I now have 8 credit cards, with £17k of debt, most of which is on 0% for a year. I have 3 loans, one with 8k left, one with 7k left and one with 19k left. I earn £50k a year, I can just cover all my payments but have about £100 spare for food……I don’t want to loose my house but either I sell up or take out a 7 year loan for £29k which will mean I can pay off all my credit cards and 2 loans, this will take my payments for all that from £870 a month to £538 giving me some money to live on. Any advice pleaseFirst of all, well done for recognising you have a problem and coming to get help, this is not always easy.Before deciding on a debt solution I think there needs to be some analysis of where the money went.I have had family and friends in London buy a flat to add a bedroom, it was the only way they could afford to get to a 2 bed flat to start a family. They both used up to 6 credit cards each to fund the development of the property and that was after they had saved up around £40k and cashed in ISA's etc. When one went to remortgage to pay off all this debt (as property value was not £250k higher) the bank refused the mortgage because apparently they do not like to use a mortgage for this purpose. 6 months later they went to a broker who got them a deal to remortgage and they paid off every penny of debt, even the zero percent.House value (Gross)..................... 163000Mortgage....................................... 144000Therefore if your debt was 90% spent on the property and the property now has a higher value then I would suggest a remortgage, even if you have to pay above the going rate. However, unless you were quoting the old house valuation then it seems as if this was a money pit and you made poor decisions on developers.If we consider that theAmount short for making debt repayments. -278and you do only have around £20,000 of equity then the simple solution is to remortgage the house, pay off the Zopa thus reducing your outgoings by £415Zopa...........................19000.....415.......11.2This would give you an extra £137 a month to attack the Nationwide and HalifaxNationwide.................8523......189.......8Halifax .......................6327......189.......7.8If now that you have done up the house worth more you could add and extra £15k and pay off the Nationwide and Halifax too.This would release a further £398 a month so an extra £530 a month to pare down your zero percent debt.If you use can remortgage and then use this £530 you could have the whole debt paid off in 18 monthsIf you had the dates when the zero rate expires it would be possible to reorder the cards so that you pay off the ones that have debt expiring first.If remortgage is NOT and option then let's work through other options, but first consider the ROOT CAUSE of the debt.If the Zopa debt for example was to already consolidate previous overspending then I think you need to address that problem. There is no judgement here, many people have gambling habits, paying of an Ex's debt and so on. What you need to know is whether the root cause could happen again?Normally the way I would approach an SOA like yours is on how much disposable income you have without debt and yours seems pretty healthy.So the next question is whether you mind trashing your credit record for 6 years to get a reduced rate on this debt?If the answer to that is that you want to preserve your credit record then there are two things to check,1. Is there any discount for early repayment of any loan?2. How much credit do you have on the zero percent cards and3, When do the zero rate expire.If there is some capacity on the zero percent cards and there is a discount for early repayment then it makes sense to use that capacity to reduce the debts that are costing you the most. You do this by putting your monthly spending of bills & food on the zero percent card and then each day move what you spent on the zero card to a savings account and then pay those accumulated amounts from the savings to the debt with the highest interest rate (if you benefit from early repayment).The three that stand out areZopa...........................19000......415.......11.2Nationwide...................8523......189.........8Halifax .........................6327......189........7.8

If Zopa is a fixed rate loan and does not cost less if you pay off early then Nationwide and/or Halifax would be where you spend it, assuming they too reduce.If neither reduce then still use up your credit limit but use the money to pay off the zero percent that ends earliest. This will reduce the risk of you having to pay 24% when an offer expires and you are deemed over extended and can't transfer to another zero percent card.On personal spending these are the areas to question:Water rates............................... 0 ----> This should be payableMobile phone.......................... 12----> Switch to Lebara £3 month dealTV Licence.............................. 15 ----> £0 Dump BBC & Live TVSatellite/Cable TV.................... 40 ---> Dump all pay TVGroceries etc. ....................... 280 ----> Try to cut this by 20% minimum

Petrol/diesel........................... 200 ---->Road tax.................................... 0 ----> Is this another omission, how can you spend £200 on petrol but £0 on this?Haircuts................................... 20 ----> Get a trimmer for £18 at Tesco

If you were going to DMP your debt then you might take a different approach and pare down your mortgage with any spare cash but that would be a bit of a dodgy thing to do. You are not in that desperate a state yet.

DMP will trash your credit record but you should be able to remortgage at variable rate with existing lender when the promotion rate expires (or that may have happened). If your mortgage discount has reverted it would be a good reason to remortgage as rates are coming down.

thank you for all the fantastic advise. I’m tied to year 3 of a 5 year fixed mortgage deal, I doubt that remortgaging is an option. You were correct to assume that most of the money went on the house. And as I am currently living beyond my means I am consuming more on my credit cards. I have managed to move all the card balances around this month to start new zero percent deals most at 12 months. I was focused on how to reduce my outgoings and payments before I sink. Consolidating debts and having one loan was the only way I saw to do this. I only have about twenty years until retirement so I’m limited what I can achieve. I was also worried about raising all the debt on my zero percent cards to pay off loans as this will increase my payments and also it’s only for 12 months. I keep getting messages from clear score saying my credit rating might get damaged if I go above 40 percent utilisation. I potentially have around £27000 I could utilise further at 0. Percent.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603.1K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards