We'd like to remind Forumites to please avoid political debate on the Forum... Read More »

SOA Help please

Kittymumof4

Posts: 25 Forumite

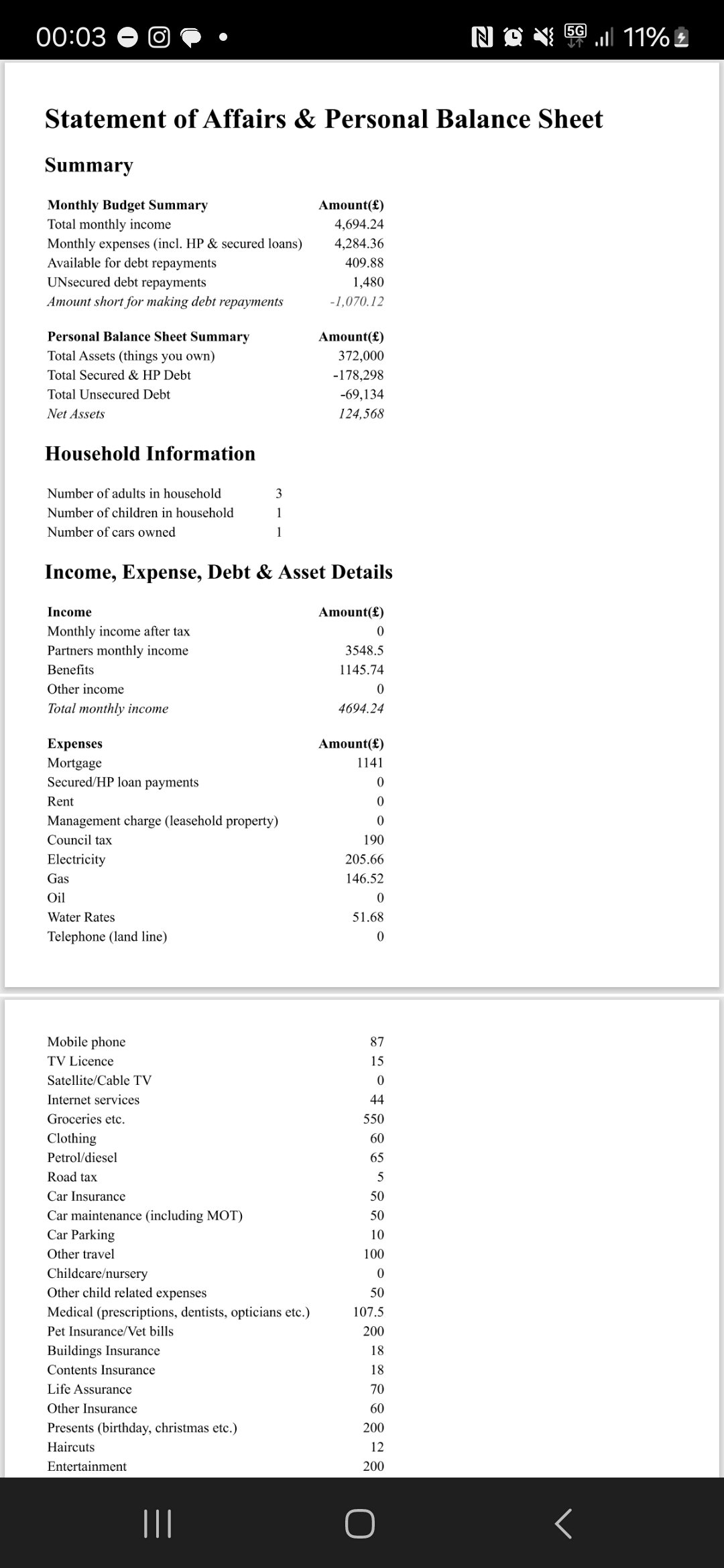

Hi, here is our SOA. It's quite sobering and now understandable as to how our debt is spiralling.

I haven't included my son's DLA (he is under 16) as this is meant to cover his additional costs which I haven't included in the outgoings.

I have included my PIP and have included some of the disability related outgoings in an added section. Others are added onto food etc as we often buy ready prepped veg as I find it difficult to peel and cut up most days. Other benefits are carers allowance and child benefit.

Phones are for 4 contracts, we may be able to buy out of one soon and replace with a SIM only deal, this would reduce the monthly amount by approximately £15.

I have just realised I missed off a work related expense of £34 which I have to pay until July.

I'm unsure what I'm doing about work as yet, I'm self employed and it's costing me money and I'm paying out but not earning anything at the moment as I've been unable to work consistently for a few years due to my own health issues and my son's care needs. I don't want to give up on the idea but I feel that trying to manage my own disability, caring for my son, studying, and trying to work have all contributed to not making time to budget and monitor spending.

Electric costs include my husbands company car EV charging and we are on an EV tariff.

Our other car is an older car which I rely on as I can't use public transport, I can't walk to and wait at bus stops and I collect my son from school daily which is 25 minutes each way.

I can see that we spend a lot of money each month and have little left to pay off debt considering the amount we owe so any advice is appreciated.

I haven't included my son's DLA (he is under 16) as this is meant to cover his additional costs which I haven't included in the outgoings.

I have included my PIP and have included some of the disability related outgoings in an added section. Others are added onto food etc as we often buy ready prepped veg as I find it difficult to peel and cut up most days. Other benefits are carers allowance and child benefit.

Phones are for 4 contracts, we may be able to buy out of one soon and replace with a SIM only deal, this would reduce the monthly amount by approximately £15.

I have just realised I missed off a work related expense of £34 which I have to pay until July.

I'm unsure what I'm doing about work as yet, I'm self employed and it's costing me money and I'm paying out but not earning anything at the moment as I've been unable to work consistently for a few years due to my own health issues and my son's care needs. I don't want to give up on the idea but I feel that trying to manage my own disability, caring for my son, studying, and trying to work have all contributed to not making time to budget and monitor spending.

Electric costs include my husbands company car EV charging and we are on an EV tariff.

Our other car is an older car which I rely on as I can't use public transport, I can't walk to and wait at bus stops and I collect my son from school daily which is 25 minutes each way.

I can see that we spend a lot of money each month and have little left to pay off debt considering the amount we owe so any advice is appreciated.

0

Comments

-

Also, I've put one car as my husbands car is a company car and is paid for from his gross wage, we just pay for electric charging. My car is an essential due to my disability and I get mobility allowance as part of PIP to pay for this.

Mortgage is just going up by over £200. We're about to go into a new deal with our current provider on a 5 yr fixed rate (new mortgage included above), was previously £911 p/m.

I was paying out more than this for work costs, previously more like £ 300 p/m and earning nothing, in the hope of getting my sole trader business up and running to help us out of the mess we're in, but it never happened due to our family circumstances and ironically got us into further debt. I've cancelled most of it now but I've kept a couple of essentials that I need to carry on with as I'm still hoping to do at least some work in the near future which will go towards paying debts. At the moment though my husband and me are at breaking point, living in a state of exhaustion with everything going on with finances and family circumstances.

We've also cancelled other subscriptions such as amazon music, Disney plus etc.

Medical includes some part funded healthcare through my husbands work from which we can claim back set amounts for opticians, dental and physiotherapy, then self paid medication.

4 cats and a dog. Pet insurance/vet bills includes pet food, cat litter, flea and wormer (not from the vets) and a little to build a fund in case we need to pay the excess for insurance or have a vet bill which is too little to claim on the insurance. I've got the food cost down from before but can't find anything cheaper that doesn't upset the cat's stomachs, 2 of them have sensitive digestion. The dog is small and food costs are lower but we do pay for grooming every 8 weeks which were now cutting down to every 12 weeks to reduce costs, the new cost is included in this section too.

We have a UK holiday booked for the summer and need to pay the balance of this somehow. Cancelling now would mean losing deposit and my son's mental health is already spiralling, and I dread to think how this would affect him. I also owe £170 to someone for a work related course as a one off payment.

Our overdraft is very near it's limit and we need to buy food eessentials and pet supplies still this month with no more income due.

I kind of feel like there's no way out of this. With nothing to get by for the rest of the month, all of the above to pay, and so little left each month to pay such a huge amount of debt......0 -

Hi Kitty, don't worry about it for this thread, but it's usually a good idea to keep to the same thread rather than start lots of different ones, then people will be able to see what's been previously discussed and pick out the relevant details more easily.Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.1

-

Not true that there's no way out.

You have £400 surplus.

Stop paying the nonpriority debts. Wait for them to default

Get a new bank account for income, essential payments and walk away from the old one

Use your surplus initially to pay for the holiday and then start to save a lump sum.

Your mortgage is now fixed for 5 years. There are two strategies that would work for you. An IVA might be the better one but you need to research the new versions that are due to be introduced in July1 -

Thank you both. Sorry @kimwp I wasn't sure whether to post it in my last thread or not, I'll keep everything here in future.

Thank you @fatbelly, it just feels like £400 is a drop in the ocean compared with what we owe, it's around 14 1/2 years to pay off if no more interest is added, presuming our income stays the same.

I've had a look into IVA and DMP, I'm finding it difficult to know the difference between the two and if each will affect us differently in the future.

The DMP, I'm reading it as we stop paying credit cards, leave our current bank and create a no overdraft account with an unrelated bank, then wait for credit card accounts to default. Then the debt is likely to be sold to debt collectors who will then come to an agreement for us to pay what we can afford. So we then set up payments with all of the creditors, splitting the £400 between them all? Do they still keep adding interest in the meantime?

So would it then stay on our credit report for 6 years after the accounts have defulted? So if our last one defaulted on say 30th December 25, it would be removed on 30th December 31? Or does it get removed 6 years after the debt has been paid?

The IVA sounds like it's a more formal agreement and the remaining debt is wiped off after the length of the IVA. So would this stay on our credit report for 6 years after it ended? So if the IVA was set for 6 years, it would be 12 years before it was removed from our credit rating?

Obviously I want us to get out of the debt cycle so don't plan on taking out more credit in the future, but I'm so worried about how all of this will affect our mortgage, especially if we move house which we plan to do in the future. It feels like our future is wrecked no matter what we do.

I'm finding it all confusing. I'm autistic myself and under so much stress at the moment, not just with this, with other stuff too, I'm finding it really difficult to make sense of the research I'm doing.0 -

Is the mortgage cost on the SOA the amount it will be going up to?

Is the £175 Study costs the one off payment owed to a friend, or for your child at uni?

Are they getting any maintenance loan at all, do they have a part time job?

The groceries look very low unless child at uni covers their own?

The entertainment and present costs need to be lower. And the emergency fund, yes you want to build one up but as an ongoing going budget that isnt realistic.

What is the other Insurance?

I think you should give up on your self employment, you cant afford any costs, it complicates debt options and you arent well enough anyway. Rething in a few years if things feel more stable and you feel more up to it.

I agree with @fatbelly's suggestion to stop paying all the debts and switch to a new bank account, then use the money you have for the next few months to pay for the holiday then to build an emergency fund

After that a new SOA.

Your first thought for future expenses needs to be No. Future holidays, another pet, etc Sorry but this is a change of mindset and it is needed

2 -

Sorry that it's not answering all your questions, but when you open the new bank account, make sure to manually move your income and essential bills manually, not using the switching service. The idea is to create a clean break from your creditors, so they have no way of taking any more payments.

At this point you would normally build up an emergency fund with the money that is not going to your creditors while waiting for your debts to default. Fatbelly is suggesting you use this money to pay for your holiday - once that is paid (or while that is being paid - how are you planning to pay for it?), you need to build up your emergency fund before you pay anything significant to your creditors. This is in case your husband loses his job, or the car breaks down and you need a new one etc as you won't be able to rely on credit to tide you over.Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.2 -

Just a quick one to say that an IVA stays on your credit file from six years from the day it starts.

You are in for six years of poor credit history whatever you do. View this as a good thing.1 -

The mortgage cost on the SOA is the new cost when it goes up.ManyWays said:Is the mortgage cost on the SOA the amount it will be going up to?

Is the £175 Study costs the one off payment owed to a friend, or for your child at uni?

Are they getting any maintenance loan at all, do they have a part time job?

The groceries look very low unless child at uni covers their own?

The entertainment and present costs need to be lower. And the emergency fund, yes you want to build one up but as an ongoing going budget that isnt realistic.

What is the other Insurance?

I think you should give up on your self employment, you cant afford any costs, it complicates debt options and you arent well enough anyway. Rething in a few years if things feel more stable and you feel more up to it.

I agree with @fatbelly's suggestion to stop paying all the debts and switch to a new bank account, then use the money you have for the next few months to pay for the holiday then to build an emergency fund

After that a new SOA.

Your first thought for future expenses needs to be No. Future holidays, another pet, etc Sorry but this is a change of mindset and it is needed

The study cost is my studies. I have a student loan for the course costs but these are in addition and are compulsory for the course. I have 2 years left after thus year. I could defer and leave in July, but then I need to qualify within 5 years or I'd have to start it all again or just not continue and I think the qualification will help me to earn, especially as my son gets older and more independent.

The grocery allowance is the absolute basics we can live on. My older uni child is also fed from this. I'm not sure if it's realistic to continue this long term or if I should account more.

The emergency fund, I've put that because we have some doors and windows that need replacing. We've been holding off but its getting to the point where we're struggling to close and lock them. We've had a quote to repair rather than replace them but it's still £1000.

Entertainment is high due to our son and his needs to go out, for the sake of him but for our sanity too. I will look at taking more of these costs from his DLA though. We do lots of free things but it would make things extremely difficult if we didn't pay for certain trips out now and then.

We need to look into the insurances, we've seen various coming out of the account but not sure what they all cover so we've planned to look at the paperwork at the weekend to see if any of these can go. I know we have mortgage and unemployment protection, not sure of the others.

I'm thinking the same about the self employment. I think my husband is hanging onto the hope that I'll magically start earning enough to keep up with debt payments.

We definitely won't have any more pets! At least not unless we get ourselves into a better position financially and only when ours are no longer with us.

Holidays, I'm not sure how I'll manage that one. My son talks about our annual holiday almost every day and won't understand at this stage why we suddenly can't go. It's a self catering budget holiday but still a cost.

My son is currently in a mental health crisis with risk of su*cide so I cannot tell him about any of this, he does understand that we don't have much money at the moment but I can't tell him more than this as I'm trying to keep him safe and stable as much as possible.

The holiday this year, we have around £750 to pay, we'll use grocery allowance for shopping while we're there and we always do as much free stuff as possible but will have to be extra careful, using the entertainment money and his DLA allowance for anything extra he spends.

With the emergency fund then, how long does it usually take from stopping payments to coming to an agreement to pay less? Just trying to work out how much we could potentially save before restarting payments. Is interest still charged while the accounts are going unpaid and while we're paying them off with the lower amounts?0 -

Don't worry about your mortgage - you will be five years on from taking action, so all the defaults will be five years ago when you are applying for your next mortgage - this means the impact will be less. Plus you'll have less debt and you'll be able to get a fix with your current provider without a credit check. You may not be able to get the best rates available, but you're already in that position anyway with your debt.Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.1

-

Okidoki, so the windows and doors fix is a separate category, not an emergency fund (which is for unknown things)Kittymumof4 said:

The mortgage cost on the SOA is the new cost when it goes up.ManyWays said:Is the mortgage cost on the SOA the amount it will be going up to?

Is the £175 Study costs the one off payment owed to a friend, or for your child at uni?

Are they getting any maintenance loan at all, do they have a part time job?

The groceries look very low unless child at uni covers their own?

The entertainment and present costs need to be lower. And the emergency fund, yes you want to build one up but as an ongoing going budget that isnt realistic.

What is the other Insurance?

I think you should give up on your self employment, you cant afford any costs, it complicates debt options and you arent well enough anyway. Rething in a few years if things feel more stable and you feel more up to it.

I agree with @fatbelly's suggestion to stop paying all the debts and switch to a new bank account, then use the money you have for the next few months to pay for the holiday then to build an emergency fund

After that a new SOA.

Your first thought for future expenses needs to be No. Future holidays, another pet, etc Sorry but this is a change of mindset and it is needed

The study cost is my studies. I have a student loan for the course costs but these are in addition and are compulsory for the course. I have 2 years left after thus year. I could defer and leave in July, but then I need to qualify within 5 years or I'd have to start it all again or just not continue and I think the qualification will help me to earn, especially as my son gets older and more independent.

The grocery allowance is the absolute basics we can live on. My older uni child is also fed from this. I'm not sure if it's realistic to continue this long term or if I should account more.

The emergency fund, I've put that because we have some doors and windows that need replacing. We've been holding off but its getting to the point where we're struggling to close and lock them. We've had a quote to repair rather than replace them but it's still £1000.

Entertainment is high due to our son and his needs to go out, for the sake of him but for our sanity too. I will look at taking more of these costs from his DLA though. We do lots of free things but it would make things extremely difficult if we didn't pay for certain trips out now and then.

We need to look into the insurances, we've seen various coming out of the account but not sure what they all cover so we've planned to look at the paperwork at the weekend to see if any of these can go. I know we have mortgage and unemployment protection, not sure of the others.

I'm thinking the same about the self employment. I think my husband is hanging onto the hope that I'll magically start earning enough to keep up with debt payments.

We definitely won't have any more pets! At least not unless we get ourselves into a better position financially and only when ours are no longer with us.

Holidays, I'm not sure how I'll manage that one. My son talks about our annual holiday almost every day and won't understand at this stage why we suddenly can't go. It's a self catering budget holiday but still a cost.

My son is currently in a mental health crisis with risk of su*cide so I cannot tell him about any of this, he does understand that we don't have much money at the moment but I can't tell him more than this as I'm trying to keep him safe and stable as much as possible.

The holiday this year, we have around £750 to pay, we'll use grocery allowance for shopping while we're there and we always do as much free stuff as possible but will have to be extra careful, using the entertainment money and his DLA allowance for anything extra he spends.

With the emergency fund then, how long does it usually take from stopping payments to coming to an agreement to pay less? Just trying to work out how much we could potentially save before restarting payments. Is interest still charged while the accounts are going unpaid and while we're paying them off with the lower amounts?

There isn't a usual time to come to an agreement. You stop paying the debts so they default and start 6 year count down til they come off your credit record (and also interest is usually stopped at this point too). Once defaulted, you contact the provider to ask where to send payments to and you only send what you can afford. So if you are still building up your window/door fix fund and emergency fund at that point, you tell them you are only able to afford small payments at the moment and you will increase the payments when you can. Later, once you have been paying a while, you can think about making full and final offers to write the debt off at a proportion of what is still owed. Note, this is applicable to the dmp route, I'm not sure what of this applies to the IVA route.

Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 350.1K Banking & Borrowing

- 252.8K Reduce Debt & Boost Income

- 453.1K Spending & Discounts

- 243.1K Work, Benefits & Business

- 597.4K Mortgages, Homes & Bills

- 176.5K Life & Family

- 256K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.6K Read-Only Boards