We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Reeves' ISA review

Comments

-

I suspect that data might not be representative of the current scenario though. I pay £20k into an ISA each year now but I didn’t pay in anything in 21/22. That was by choice because interest rates were so low that I was never going to pay tax on the interest anyway and non isa rates were better than isa rates.SnowMan said:poseidon1 said:

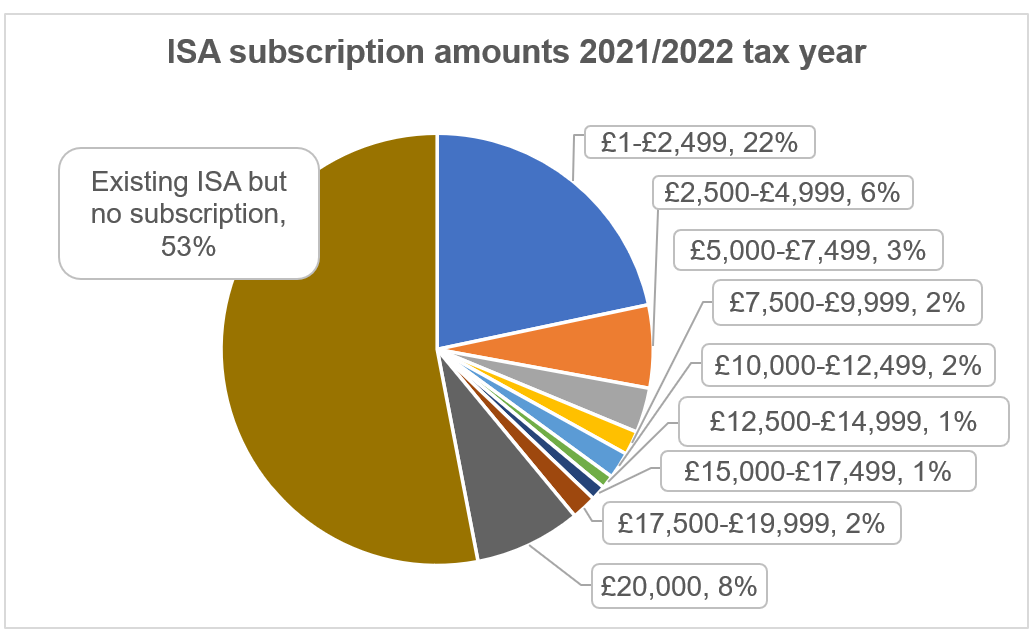

Interesting article below from A J Bell which backs up your statement. Particularly interesting how the total value in stocks and shares isas completely dwarfs that of cash isas by a magnitude of 7 times.masonic said:So about 75% of ISA subscribers will not be impacted as they don't use more allowance than that ordinarily. Seems well worth the political heat.

https://www.ajbell.co.uk/group/news/isas-unpacked-who-holds-them-and-how-much-do-they-have#:~:text=Around 1.8 million use up their full,60% contributing less than £5,000 a year

Obviously a large chunk of the population cannot afford to get anywhere near the maximum £20k annual contribution, so our little echo chamber of forumites in no way reflects the wider saving public.

I fear for that reason, other than the inevitable backlash from the Tory press, reducing cash isas to £10k annually will still be a generous limit for the vast majority.

Personally as long as the £20k overall annual limit is retained, I won't be bothered either way.The data is all at the link below although it's only available up to the 2021/2022 tax yearOf the 22 million UK residents who had an ISA (cash or stocks and shares) at all (so many don't even have one and so aren't represented in the chart below at all) the percentages contributing over 10K pa is only 14% (of which 8% contribute the full 20K)

With hindsight, that wasn’t perhaps the most sensible decision but it seemed right at the time as I never expected interest rates to go up so quickly and so soon afterwards.Northern Ireland club member No 382 :j2 -

Given where interest rates are now, the cash ISA allowance goes some way in mitigating the tax increases resulting from from the ongoing freeze of the personal allowance. It's difficult to avoid the noise in today's media that report a further extension of the freeze is on the cards, further increasing our taxes. However, everything keeps changing every two minutes, and even after budget day there are likely to be u-turns on ninety per cent of the budget announcements anyway!0

-

The last paragraph is interesting. It is always said it is best not to trade/tinker with your investments too much .Alpine_Star said:From today's FT Online. 1

1 -

At least the article contextualises the data, using inflation and QE. Explaining that their 'fortune' is predominately down to asset inflation and time in the market. Since they probably haven't realised much of the capital gain, the ISA element is largely irrelevant. Though obviously, if there is a 'tax free' option, it makes sense to use it.Alpine_Star said:From today's FT Online.0 -

The government is likely to get some money back eventually from the ISA millionaires in the form of IHT. Basic allowance of £325k unchanged since 2009 with a freeze currently planned until at least 2030.

If you're 72 and have over a million pounds sitting in your ISAs it's difficult to imagine how all that could be spent.4 -

You could follow George Best's example, wine, women & song, and then squander the restslinger2 said:The government is likely to get some money back eventually from the ISA millionaires in the form of IHT. Basic allowance of £325k unchanged since 2009 with a freeze currently planned until at least 2030.

If you're 72 and have over a million pounds sitting in your ISAs it's difficult to imagine how all that could be spent.

Member of "Rubbish at Radishes" club1 -

That's probably about six months' care home fees.2

-

So what are we thinking for pure cash ISAs?

Reduced to 15K or 12K effective the next tax year?0 -

If I put my political thinking cap on, I would not be surprised to find it does not feature in the budget at all, or at least only in some highly modified form.SickGroove said:So what are we thinking for pure cash ISAs?

Reduced to 15K or 12K effective the next tax year?

It would stir up resentment. and headlines like 'Reeves robs pensioners of more savings taxes'

It would only encourage a small minority to start investing in a S&S ISA, who had not done so before.

A lot of those investments would be outside the UK.

If the markets bombed out, the Mail/Telegraph/Express would be full of 'Pensioner loses life savings due to Reeves' headlines.

So if I was the Chancellor, I would kick the whole idea into touch .2 -

The problem they've got is that if they reduce the annual allowance for just Cash ISAs then they'll have to stop transfers from S&S ISAs to Cash ISAs. And if they announce it to start next April then they'll be encouraging transfers of S&S ISAs to Cash ISAs for the rest of this tax year if that's going to be your last chance to do such a thing. They'll probably also want to stop people investing in cash-like investments within a S&S ISA. All sounds pretty complicated to me. Simpler just to cut the annual ISA allowance to £10k or whatever.SickGroove said:So what are we thinking for pure cash ISAs?

Reduced to 15K or 12K effective the next tax year?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards