We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Help with tax code/untaxed savings interest

Comments

-

How can I know for sure if I was a higher rate tax payer for 2024-25? This is what I'm struggling to work out 😕molerat said:PAYE will deduct higher rate tax on any amount above your coded allowance + £37700 but that does not necessarily make you a higher rate taxpayer. You may be having higher rate tax deducted to pay the correct amount of standard rate, that still will not make you a higher rate tax payerIf you are actually a 40% tax payer and making RAS pension payments then you need to inform HMRC via the on line form, no need for SA. https://www.gov.uk/guidance/claim-tax-relief-on-your-private-pension-payments0 -

This is what I'm thinking could have happend; I've JUST spilled over into 40% tax band when you include the £750 taxable interest, and if I have spilled over then my tax free interest allowance will have dropped from £1000 to £500 so I'll be taxed on that extra bit 😕LL_USS said:I am interested to see how saving interest is taken into the tax code adjustment. Please update the result after you check with HMRC, @SneaksyWhippet . Hope it is just them making a mistake.When I called and asked them about a change in my tax code, it was indeed a mistake from their side and they fixed it right away the month after (putting back some money and thus my tax that month was reduced).As I understand (from the HMRC woman on the phone) ALL of our incomes are put together in their record: taxable pay (i.e. after pension contribution) from your work, any additional income, for e.g. gross external examination fee for me (before tax, and this is taxed from source before it reaches my account) etc. So I suppose the interest outside of ISA (in your case, ful £750) is included in this number. If the total number is still under the 40% tax threshold then you are not taxed further on the saving interest. If it's just spilling over to the 40% band then for the year after, they put the untaxed saving interest over to next year, perhaps?1 -

@SneaksyWhippet I have to be very careful keeping the total quite a bit under the threashold. When I called HMRC I was told "you are very very close, be careful". We may miss some items that need to be included in, for e.g. I've just found out that Nationwide £50 after Virgin buy-out, and if they give the fair share again - both of these are treated as saving interests. That has made me move some saving to an ISA account, though the latter is much lower rate.

0 -

Oh that's frustrating! Do you know what else counts? Is there a list somewhere? Things like cashback, switching rewards etc could catch me out 🤔LL_USS said:@SneaksyWhippet I have to be very careful keeping the total quite a bit under the threashold. When I called HMRC I was told "you are very very close, be careful". We may miss some items that need to be included in, for e.g. I've just found out that Nationwide £50 after Virgin buy-out, and if they give the fair share again - both of these are treated as saving interests. That has made me move some saving to an ISA account, though the latter is much lower rate.0 -

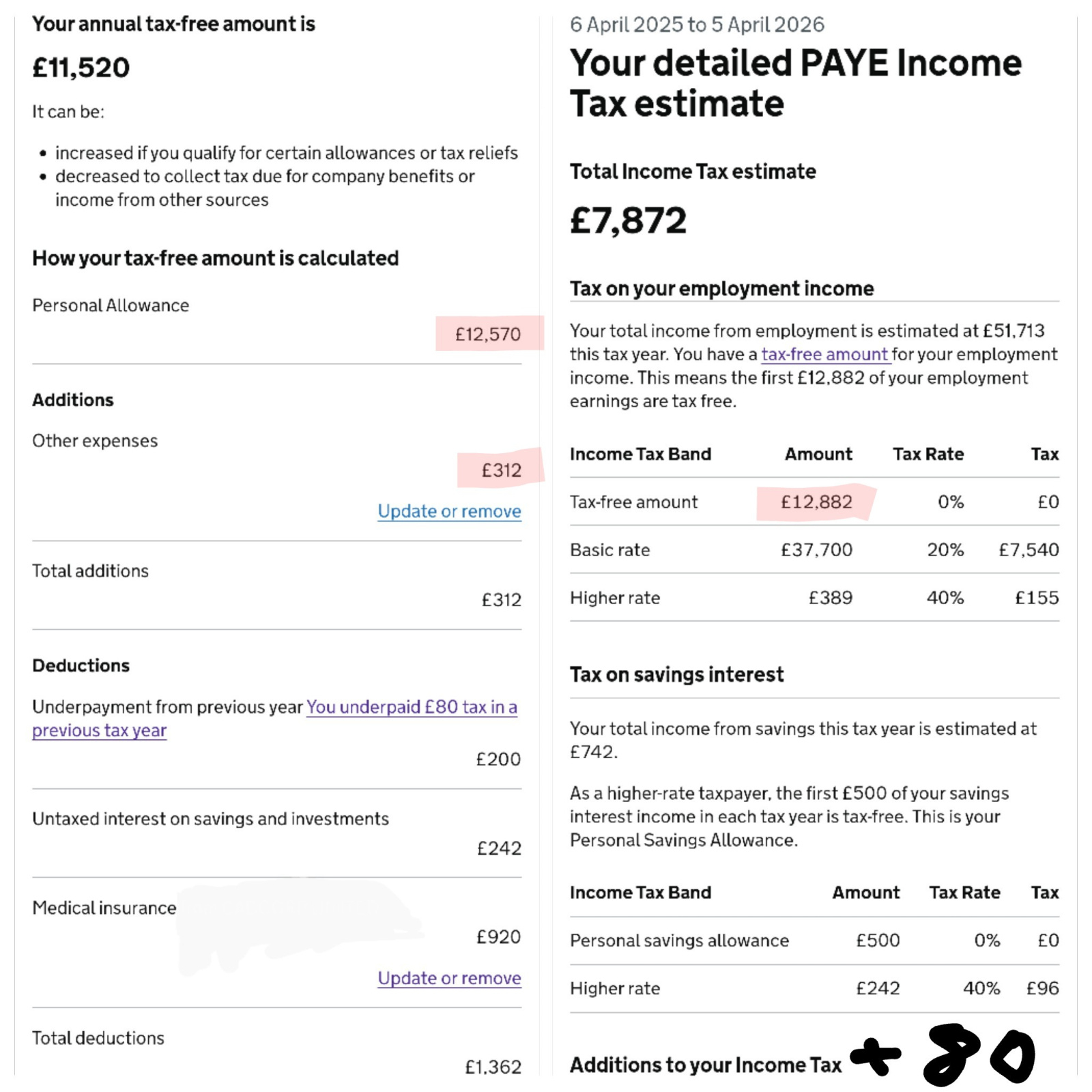

I've just found the page on the right hand side buried in the HMRC app (had to add the +80 for underpayment of tax last year as it wouldn't fit in the screenshot).

I'm really trying to understand how it all works and getting so confused. Why is the tax free amount on the RHS just the red bits on the LHS, without considering the deductions? Both sides have the exact same wording of "tax-free amount" yet they're not the same. Are the deductions (plus £500 personal savings allowance) already added on to the total estimated income amount? I can't quite work out how they've got to the figure of £51,713 (unless they consider previous bonuses/pay rises to estimate rather than looking at only current salary?).0 -

That page (on the right) is a bit confusing.SneaksyWhippet said:

I've just found the page on the right hand side buried in the HMRC app (had to add the +80 for underpayment of tax last year as it wouldn't fit in the screenshot).

I'm really trying to understand how it all works and getting so confused. Why is the tax free amount on the RHS just the red bits on the LHS, without considering the deductions? Both sides have the exact same wording of "tax-free amount" yet they're not the same. Are the deductions (plus £500 personal savings allowance) already added on to the total estimated income amount? I can't quite work out how they've got to the figure of £51,713 (unless they consider previous bonuses/pay rises to estimate rather than looking at only current salary?).

AIUI the £51,713 will include HMRC's estimate of your employment/pension income (including company benefits) but they also add in the untaxed interest. But that then isn't in the first bit, it is separated out into the Tax on savings interest section.

So if you look at your home page is their estimate of your employment/pension £50,051? This will probably have been based on the latest Real Time Information (payroll) information received by January 2025, when most codes for 2025-26 are calculated.

For example earn £18,000 by month 9 (in 2024-25) and HMRC will estimate £24,000 as your earnings for 2025-26. Where you have been in that job from 6 April 2024 or earlier.0 -

@SneaksyWhippet I had to think about all bits of income that is taxable to add into my spreadsheet. I tried to look for a list somewhere but couldn't, HMRC website is just so basic (only listed as savings on interest and not exhaustive list). I searched the tax status for any incomes I am not sure (and no cash back and bank switch bonuses are not taxable).SneaksyWhippet said:Oh that's frustrating! Do you know what else counts? Is there a list somewhere? Things like cashback, switching rewards etc could catch me out 🤔Regarding how to read these - I am also curious wanting to understand these yet sometimes it's beyond me and I kind of give up and make sure I am well under the threshold paying a bigger amount into volunteer contribution pension and giving money to my son's ISA.I just see the same thing that on the right handside 12,882=12,570+312 (the other expenses) but still not sure about other bits.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.8K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.4K Mortgages, Homes & Bills

- 178.2K Life & Family

- 261K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards