We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Taking 25 percent lump sum

Comments

-

Whilst the people replying are no doubt doing so to help the OP I would say none of these people are insured to protect themselves and more importantly the OP should the advice be incorrect. I would therefore reccommend seeking advice from a financial adviser who is all of the above

Rob0 -

madbadrob said:Whilst the people replying are no doubt doing so to help the OP I would say none of these people are insured to protect themselves and more importantly the OP should the advice be incorrect.Nobody on this thread has offered the OP any "advice".

Is that intended as advice, or just as a thing to consider in the round?madbadrob said:I would therefore reccommend seeking advice from a financial adviser who is all of the above

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.1 -

That would pretty much apply to every other thread on this board !madbadrob said:Whilst the people replying are no doubt doing so to help the OP I would say none of these people are insured to protect themselves and more importantly the OP should the advice be incorrect. I would therefore reccommend seeking advice from a financial adviser who is all of the above

Rob

4 -

What you are stating is true ... but ... there are some counter elements to take into account. Although he will have a reduced weekly income after 60, he will of course benefit from circa 6 years income beforehand at £5,636 per annum - totalling nearly £34,000 before that positive total will start being eaten away at circa £80 a week which will mean he will not be negatively impacted by his decision until the age of 68 when the weekly post-60 loss exceeds the cumulative 6 year gain between 54 and 60.Dazed_and_C0nfused said:

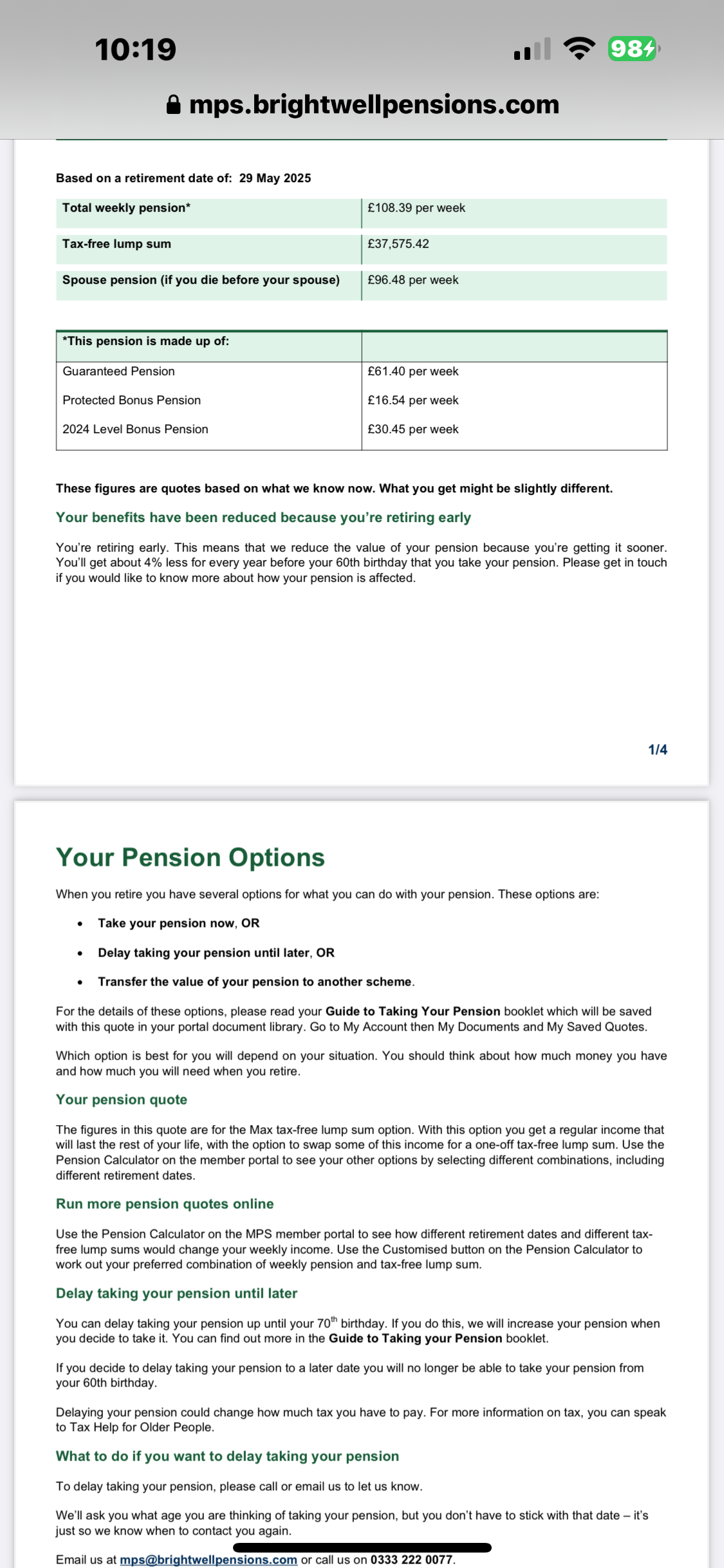

Do you understand how much guaranteed pension you are giving away to get that tax free lump sum?johnnicola said:Here is the statement that ive got

Looking at what @xylophone posted it's over £4k in annual pension (~£80/week).

Which you lose forever. You could be getting that pension for the next 40 years so definitely not something to be done lightly.

Have you considered getting a loan? That might be a much better option than giving away so much of your pension.

Also, the benefit of paying off debt-incurring interest now would also have a positive impact on his net financial position. Plus any amount remaining after the relevant debt(s) is paid off can itself be invested for (hopefully) positive growth between now and 60.

So in summary, there are aspects that add value to a potential decision to balance against the weekly loss he will incur post-60. As he appears to now have a healthy income and further private pension planning in place for enhanced income in retirement, exploiting the lump sum now can make a lot of sense.0 -

Do not forget that annual increases in the pension, mean that £80 will grow significantly over the years.Charlemagnia said:

What you are stating is true ... but ... there are some counter elements to take into account. Although he will have a reduced weekly income after 60, he will of course benefit from circa 6 years income beforehand at £5,636 per annum - totalling nearly £34,000 before that positive total will start being eaten away at circa £80 a week which will mean he will not be negatively impacted by his decision until the age of 68 when the weekly post-60 loss exceeds the cumulative 6 year gain between 54 and 60.Dazed_and_C0nfused said:

Do you understand how much guaranteed pension you are giving away to get that tax free lump sum?johnnicola said:Here is the statement that ive got

Looking at what @xylophone posted it's over £4k in annual pension (~£80/week).

Which you lose forever. You could be getting that pension for the next 40 years so definitely not something to be done lightly.

Have you considered getting a loan? That might be a much better option than giving away so much of your pension.

Also, the benefit of paying off debt-incurring interest now would also have a positive impact on his net financial position. Plus any amount remaining after the relevant debt(s) is paid off can itself be invested for (hopefully) positive growth between now and 60.

So in summary, there are aspects that add value to a potential decision to balance against the weekly loss he will incur post-60. As he appears to now have a healthy income and further private pension planning in place for enhanced income in retirement, exploiting the lump sum now can make a lot of sense.0 -

True. Of course the length of time he will be receiving the pension is unquantifiable - the maths would obviously differ between an optimistic 40 year duration and a period somewhat shorter. The circa 8 year timescale (at 68 years old) before an early redemption enters negative territory overall still holds water though as the 54-60 income would also increase too.Albermarle said:

Do not forget that annual increases in the pension, mean that £80 will grow significantly over the years.Charlemagnia said:

What you are stating is true ... but ... there are some counter elements to take into account. Although he will have a reduced weekly income after 60, he will of course benefit from circa 6 years income beforehand at £5,636 per annum - totalling nearly £34,000 before that positive total will start being eaten away at circa £80 a week which will mean he will not be negatively impacted by his decision until the age of 68 when the weekly post-60 loss exceeds the cumulative 6 year gain between 54 and 60.Dazed_and_C0nfused said:

Do you understand how much guaranteed pension you are giving away to get that tax free lump sum?johnnicola said:Here is the statement that ive got

Looking at what @xylophone posted it's over £4k in annual pension (~£80/week).

Which you lose forever. You could be getting that pension for the next 40 years so definitely not something to be done lightly.

Have you considered getting a loan? That might be a much better option than giving away so much of your pension.

Also, the benefit of paying off debt-incurring interest now would also have a positive impact on his net financial position. Plus any amount remaining after the relevant debt(s) is paid off can itself be invested for (hopefully) positive growth between now and 60.

So in summary, there are aspects that add value to a potential decision to balance against the weekly loss he will incur post-60. As he appears to now have a healthy income and further private pension planning in place for enhanced income in retirement, exploiting the lump sum now can make a lot of sense.

Not endorsing him doing so or not doing so, just highlighting that there are balancing elements to the equation, especially when taking into account what his short-term need may be for the capital to reduce current interest-incurring debt. If he had been in a position where this was his only pension provision supporting income in retirement, that would also change the calculus. Fortunately he appears to be in position to not be solely relying on this particular pension.0 -

Thanks for all your feedback really appreciate it… My other pensions that ive got apart from my mps would be £5600 per annum another current one in todays money £6600 plus my current provider is £34000 and also ive got £31000 in a private pension not paid into for years… Then state pension which is £11500 so total would be roughly around £55k per year in retirement2

-

Ok, one last thing before you give up about £100k worth of pension to get a £37k tax-free lump sum.Can you get £37k of tax-free cash from any of your other pensions? Your current workplace pension, for example, is it a Defined Contribution (DC) scheme (a big pot of investments) or a Defined Benefit (DB) (final salary or CARE) scheme? If DC, could you crystallise part of it (by making a partial transfer out, if necessary) to get the £37k you need? That could leave you with more income in retirement than your current plan does, so a win-win.N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.2 -

Once all the online forms to take your pension filled in does it start to be paid monthly and receive lump sum?

0 -

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.8K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.8K Work, Benefits & Business

- 603.4K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards