We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

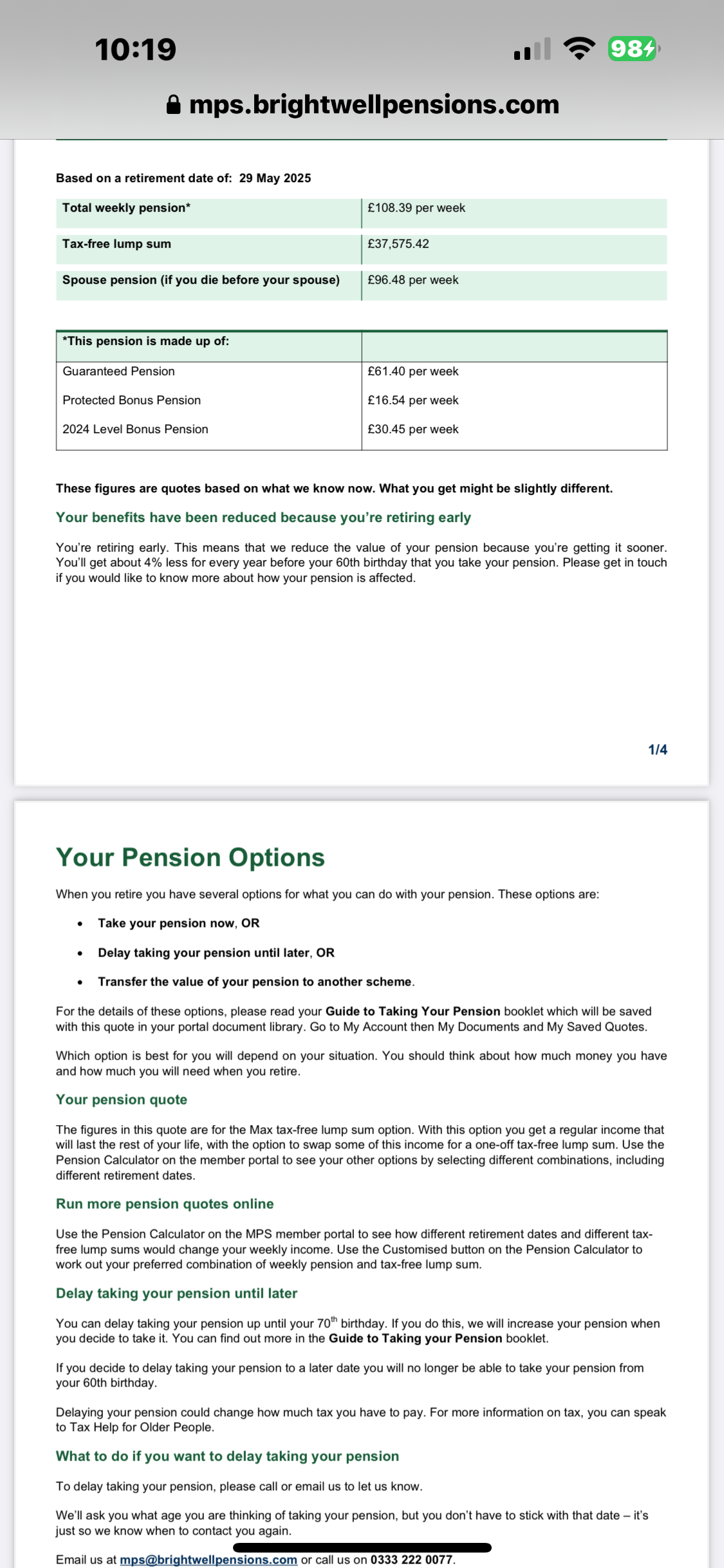

Taking 25 percent lump sum

I want to access 25 percent of my pot which is £37,575.42 and then my weekly pension £108.39.

I dont need the weekly pension but need the lump sum to pay debts off.

Many thanks

John

Comments

-

This pension sounds like it is defined benefit, there is no pot of money so you start the pension taking the commencement lump sum and the weekly pension, you have no choice over that. You can then do what you wish with the taxed regular payment amount. Have you actually had a quote for taking the pension early as there could be a fairly large reduction.edit. Looking at the pension scheme booklet it seems there will be a reduction of around 23% for taking it 5 years before 60.1

-

As a former miner, you are likely to have a 'protected pension age' so will be able to access your benefits even though you are still only 54 (although they will be reduced because you are taking them before the scheme's normal retirement age of 60).johnnicola said:Hi first time posting for a while.. Im 54 years old and ex employee of miner workers pension scheme.. Normal retirement age for this scheme is 60.Im full time employed with no intention of retiring till 65 years old unless something drastic changes.

I want to access 25 percent of my pot which is £37,575.42 and then my weekly pension £108.39.

I dont need the weekly pension but need the lump sum to pay debts off.What options do i have please?.. Would i need an annuity or could i put the 75 percent left in my current employer, or take the weekly pension and just offset my current contributions and add £108.39 in avcs to my current pension?

Many thanks

John

It sounds as if you have received a Retirement Benefits Options statement. If you want to access your tax free lump sum, which as you've noted can be up to 25% of the total value of your MPS benefits, your (regular) pension payments must start at the same time.

You can indeed increase your contributions to your current scheme by adding AVCs, which would be deducted from your current salary (and get tax relief).

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

https://iwmps.com/media/ccmf3fhb/iwmps-scheme-booklet.pdfI want to access 25 percent of my pot which is £37,575.42 and then my weekly pension £108.39.You don't have a pot - you are a deferred member of a defined benefit pension scheme. See p20 of the Guide above.

Do you mean weekly or is it monthly?

A pension for members of 1/60th

of earnings near to the date of leaving Scheme service per year of Contributing Service;

• The option for members to exchange part of their pension for a tax-free cash sum;

• A normal retirement age of 60;

• The option to take benefits from

age 50, reduced to reflect the cost

of early payment. Members who retire immediately on leaving their employment at age 59 or over, their benefits will not be reduced.Pensions are paid every four weeks two weeks in arrears and two weeks in advance.

With regard to the tax free lump sum

Can I exchange Pension for Cash at Retirement?

When you take your pension you will

have the option to exchange part of it for

a cash sum which, under current tax law,

is not subject to income tax. For every

£1 of annual pension that you give up

you will receive a cash sum of £9. This “commutation rate” is fixed in the IWMPS Rules. The maximum amount of pension you can exchange in this way in accordance with current tax law works out under the IWMPS Rules at approximately 3.82 x

your pension.The commutation rate is far from generous. See p16 of the Guide.

0 -

Here is the statement that ive got

0

0 -

So im entitled to 25 percent tax free even though im under 55 years of age?0

-

Do you understand how much guaranteed pension you are giving away to get that tax free lump sum?johnnicola said:Here is the statement that ive got

Looking at what @xylophone posted it's over £4k in annual pension (~£80/week).

Which you lose forever. You could be getting that pension for the next 40 years so definitely not something to be done lightly.

Have you considered getting a loan? That might be a much better option than giving away so much of your pension.0 -

Forget "25%", you are entitled to a tax free commencement lump sum in accordance with the scheme rules from the age of 50. That seems to be based on the (very poor) commutation rate of £9 for every £1 given up with a maximum lump sum of 3.82 times the original annual pension.0

-

Correct. You have a protected pension age.johnnicola said:So im entitled to 25 percent tax free even though im under 55 years of age?Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

I'd be careful, as the IWMPS is a different scheme to the MPS. Looks like the same commutation rate applies though (https://www.mps-pension.org.uk/im-not-taking-my-pension/your-benefits-at-retirement/).xylophone said:https://iwmps.com/media/ccmf3fhb/iwmps-scheme-booklet.pdfThe commutation rate is far from generous. See p16 of the Guide.

1 -

No. Defined benefit schemes don't have 25% tax free cash. They have a pension commencement lump sum, which is paid with a reduced annual income. Taking PCLS would likely be a poor financial decision.johnnicola said:So im entitled to 25 percent tax free even though im under 55 years of age?I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards