We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

About to renew motor insurance with 12 points no ban

RocketRonnieRadox

Posts: 83 Forumite

Hi all.

please Be kind - I know it’s my fault.

i have been with the same specialist modified car insurance for several years. Over the past year or two I accumulated 6 points for speeding, and SP30 and an SP50. This didn’t affect my premium badly at all but during the term of this years policy I managed to get 6 points and a £701 fine for speeding 53 in a 30 and I fully accept that it is my fault.

i have been with the same specialist modified car insurance for several years. Over the past year or two I accumulated 6 points for speeding, and SP30 and an SP50. This didn’t affect my premium badly at all but during the term of this years policy I managed to get 6 points and a £701 fine for speeding 53 in a 30 and I fully accept that it is my fault.

I went to court and pleaded exceptional hardship as my 84 year old mum depends on me for me driving her to hospital etc. There were numerous other reasons for EH but I’ll not list them and advise that my plea was accepted but I still got 6 points making total of 12 but with no disqualification or ban.

the time has come for me to renew and I’m very worried about whether or not I’ll get insurance or not once I declare the additional 6 points which were SP30.

maybe this insurer won’t insure anyone with more than a set number of points ?

the time has come for me to renew and I’m very worried about whether or not I’ll get insurance or not once I declare the additional 6 points which were SP30.

maybe this insurer won’t insure anyone with more than a set number of points ?

Will it be as bad as having been disqualified?

I'm terrified of not being able to get renewed or finding a reasonable quote.

eek will they cancel my insurance ! Only 10 days left on it.

having read the posts of those who got disqualified and their experiences with insurance companies after a ban I would even be tempted to not disclose ! I won’t do that as it’s fraud but it did cross my mind.

maybe I should try getting some quotes from other companies and declare the 12 points no ban first ??

I'm terrified of not being able to get renewed or finding a reasonable quote.

eek will they cancel my insurance ! Only 10 days left on it.

having read the posts of those who got disqualified and their experiences with insurance companies after a ban I would even be tempted to not disclose ! I won’t do that as it’s fraud but it did cross my mind.

maybe I should try getting some quotes from other companies and declare the 12 points no ban first ??

0

Comments

-

The best thing to do is to go to the comparison sites and get some quotes. Doing it sooner rather than later will mean that you have time to plan for what you do next.

You should be prepared to get fewer quotes than usual and for those quotes to be more expensive, but there's no reason why you shouldn't be able to get insurance at all, unless you are already restricted to a limited number of providers by age, a highly modified car or some other unusual risk.

You do mention a modified car and a specialist insurer. They should not cancel your policy mid:term because you tell then about a new conviction, but whether they'll offer you renewal terms is anybody's guess. Nobody can say whether a particular un-named insurer will insure you with 12 points.

If the combination of car and points does make it difficult to get insurance, you might consider getting a small, cheap old runabout and locking the pride and joy in the garage for a year until you can afford to insure it again. Dealing with the issue sooner rather than later does at least give you time to think about that sort if thing, in the wrist case scenario.

Don't be tempted not to declare the conviction. It is the sort of thing that it is very easy for an industry to check in the event of a claim, and paying a lot of money for a policy that will never pay out when you need it is definitely not money saving.0 -

Very unlikely that those sites will even quote for a modified vehicle; I know, I've had one in the past and it's a nightmare ( and expensive) to get insurance. OP I think the advice to put your car in mothballs and get a runabout for a while is soundAretnap said:The best thing to do is to go to the comparison sites and get some quotes. Doing it sooner rather than later will mean that you have time to plan for what you do next.

I'm also curious of course, what car is this and what have you done to it?0 -

As above, get some quotes now, the closer you leave it to renewal date the more of a risk you will be seen as. And you are a very high risk anyway if you have 12 points and drive a modified car.

If you do have a modified car, it may be that you would be better off selling it and buying something mundane that you are less likely to speed in for a few years. That is one of the only things that you have to change the risk to the insurer.0 -

Have you spoken to your current insurer yet? If not isn't that the obvious first step? You could be worrying unnecessarily. It seems there is a limited pool of insurers for modified vehicles and you aren't in a great negotiating position.1

-

Depends what the modifications are of course - the OP didn't say at first whether he was talking about a car with an added towbar or one which was practically custom built. Though tbf the mention of a specialist insurer should have been a sign that it was closer to the latter...FlorayG said:

Very unlikely that those sites will even quote for a modified vehicle; I know, I've had one in the past and it's a nightmare ( and expensive) to get insurance. OP I think the advice to put your car in mothballs and get a runabout for a while is soundAretnap said:The best thing to do is to go to the comparison sites and get some quotes. Doing it sooner rather than later will mean that you have time to plan for what you do next.

I'm also curious of course, what car is this and what have you done to it?0 -

Thanks for taking the time.Aretnap said:

Depends what the modifications are of course - the OP didn't say at first whether he was talking about a car with an added towbar or one which was practically custom built. Though tbf the mention of a specialist insurer should have been a sign that it was closer to the latter...FlorayG said:

Very unlikely that those sites will even quote for a modified vehicle; I know, I've had one in the past and it's a nightmare ( and expensive) to get insurance. OP I think the advice to put your car in mothballs and get a runabout for a while is soundAretnap said:The best thing to do is to go to the comparison sites and get some quotes. Doing it sooner rather than later will mean that you have time to plan for what you do next.

I'm also curious of course, what car is this and what have you done to it?

what I’m afraid of most is then cancelling my policy with less than 10 days left to run.In some ways I’m tempted to not disclose and let it lapse IF cancellation is likely. Then disclose when taking a new policy ?? Not trying to be dishonest here. I want to do the right thing but I also want to avoid having insurance cancelled whilst remaining within the law.Renewal letter says that I need to disclose changes in material circumstances before renewing, if I don’t renew and go with another insurer (if I can find one) and don’t disclose to current insurers am I remaining within the law ?0 -

No you are not0

-

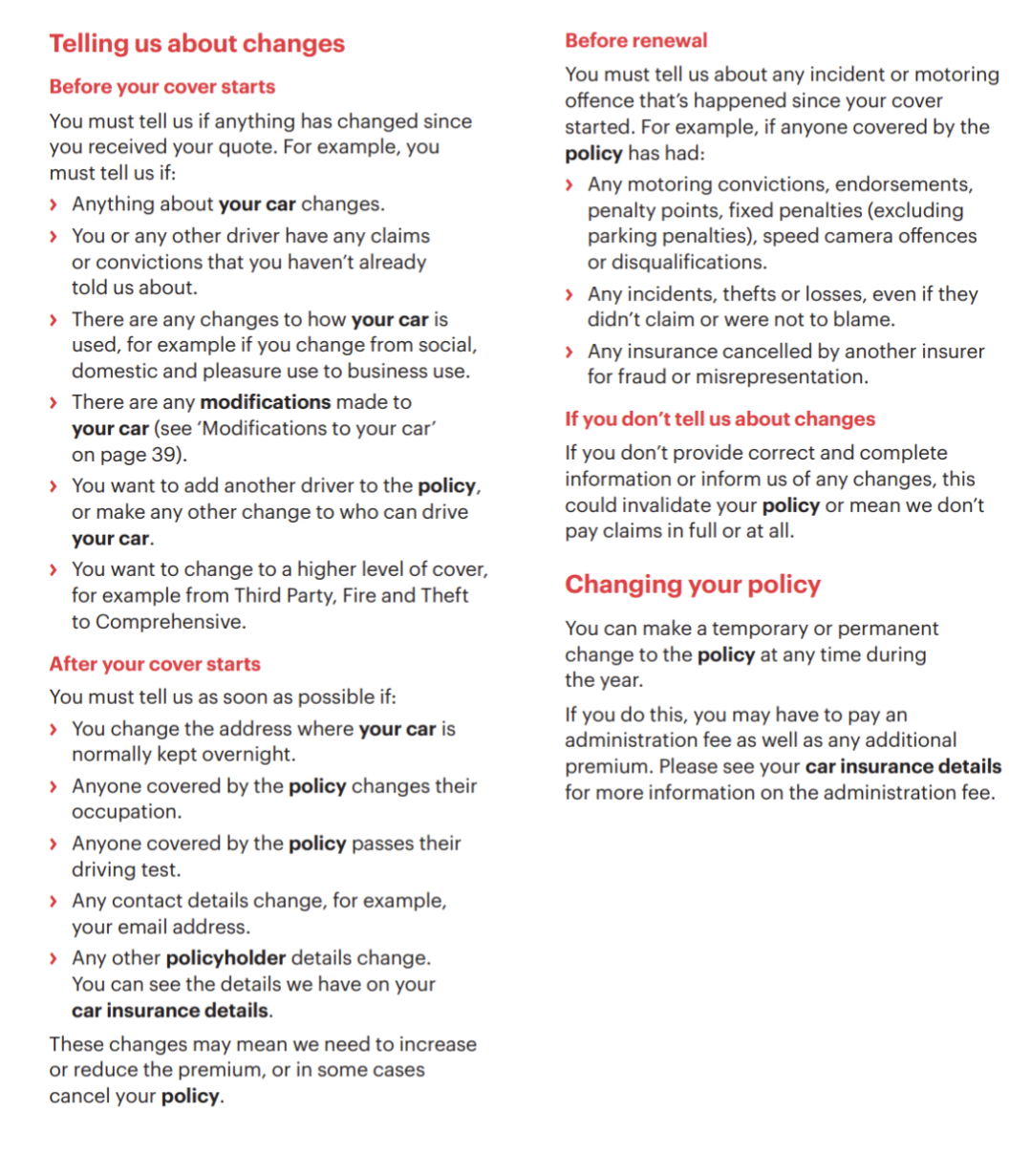

Most policies will have a section like this one which sets out what and when you need to tell the insurer.

Assuming it doesn't say that you need to tell them about convictions/points immediately (and I'm fairly sure I've never seen a policy which requires points, as opposed to bans, to be declared immediately) then you only need to tell them before you renew. And obviously if you choose not to renew, you don't have to tell them at all.0 -

Thanks. I checked the wording on mine and it says that I should tell them about “changes to my circumstances either during or before the policy begins”

by that will I be ok and not get my policy cancelled if I tell them before renewal ?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards