We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Topping up NI Contributions and Specified Adult Childcare Credits

Comments

-

Now updated:molerat said:I am afraid your numbers and narrative do not make sense. If she has £158 at April 2024 then 4 more years will take her to £183.28 and not the £168 you have quoted. With £158 for 22 years she needs another 10 to reach the max so a total of 32 years, as I said, something does not make sense there.

It is £158 amount up to April 2024

If she contributes until April 2029, this increases to £189.60 - but she will not be working to contribute the next 4 years.

Number of NI years for 15-16 or earlier: 17yrs

Number of NI years for 16-17 and later: 5yrs

Tax Year you reach state pension: 2029-2030

I thought the max is 35, not 32?0 -

So with £158 now she needs another 10 to reach the max, £221.20 - £158 = £63.20 / £6.32 = 10The big green box at the top shows £189.60 ?The text below states she can improve her forecast to £221.20 ?So if she is going to get 6 from your SACC transfers that leaves her 1 spare at the far end so she will need another 4 from 21-22 and earlier for safety.So what does she have going back to 2006-07, any part filled cheap years ?0

-

molerat said:So with £158 now she needs another 10 to reach the max, £221.20 - £158 = £63.20 / £6.32 = 10The big green box at the top shows £189.60 ?The text below states she can improve her forecast to £221.20 ?So if she is going to get 6 from your SACC transfers which will take her up to the last relevant year she will need another 4 from 21-22 and earlier.So what does she have going back to 2006-07, any part filled cheap years ?

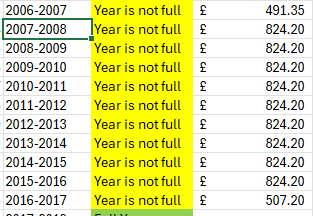

Hi, thank you for response. I'm lost on where you got 10 years from, sorry if I'm being slow? Please see screenshot below. She's got gaps 11 years gap between 2006 - 2017 and 2 years gap between 2022-2024. There's 2 cheaper years in 2006 and 2016. 0

0 -

So with £158 now she needs another 10 to reach the max, £221.20 - £158 = £63.20 / £6.32 = 10

The max is £221.20, she currently has £158, the difference is £63.20. Each year adds £6.32 so £63.20 / £6.32 = 10 years needed to reach the max. So a total of 32 years required. Due to her old rules additional state pension amount at April 2016 her starting amount with those 17 years was the equivalent of 20 years of new rules pension. Additional pre 2016 year will only pay £5.65 and would increase that 10 years needed so each year would need to be looked at on its cost / value merit.

1 -

Ar right, now I've got you!! Thank you! No wonder ppl have to ring up to speak to them about the circumstance.molerat said:So with £158 now she needs another 10 to reach the max, £221.20 - £158 = £63.20 / £6.32 = 10The max is £221.20, she currently has £158, the difference is £63.20. Each year adds £6.32 so £63.20 / £6.32 = 10 years needed to reach the max. So a total of 32 years required. Due to her old rules additional state pension amount at April 2016 her starting amount with those 17 years was the equivalent of 20 years of new rules pension. Additional pre 2016 year will only pay £5.65 and would increase that 10 years needed so each year would need to be looked at on its cost / value merit.

So she's £63.20 off / 10 years.

6 years from ASCC will come from years 2022 onwards, with a spare at the end.

So she needs to plug 4 years = £25.28, but she only has the older years worth £5.65. So I make this £25.28 /£5.65 = 4.47yrs, so she needs to purchase 5? Is this correct?0 -

Yes. 4 years would take her to £218.52 with the 5th adding the final £2.68.1

-

@molerat thank you, that makes sense. Can I ask how do you know pre 2022 is worth less at £5.65?

So looking at her gaps, she would plug

2006-2007 = £491.35

2016-2017 = £507.20

Any any other years at £824.20 x 3 years

= £3471.150 -

16-17 will give £6.32 but still requires 5 years, the 5th now adding £2.01.The value of a pre 2016 year depends on which rules the starting amount is based on. In your case the starting amount is old rules, that can be worked out from current amount and number of pre and post 2016 full years, so the value is what it would have earned under that scheme.1

-

@molerat thank you. It all makes sense, I just want to call up the line to double check everything is correct. I have had a sleepless night in case she pays incorrectly, as it's a lot of money.0

-

@molerat

Hi again, I was just thinking when the new pension raises to £230.30pw in the new tax year.

The gap between the £158 and new amount would be £72.30. So based on above, plugging 5th year, would that gain her £6.32? And takes her to £224.84, would she then need another year?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards