We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

NI Pay extra to increase my State Pension help

oliveoil54

Posts: 329 Forumite

I am 70, after watching Martin’s show last night I had a look to see what my NI Situation is.

I decided to retire early to look after my husband with Cancer & then Dementia. I had 3 years 2011 to 2014 when he had Lymphoma & Stem Cell Transplant, then from 2015 early on set Dementia/Alzheimer’s till death late in 2020. I didn’t know about claiming Carer’s Credits to top up my National Insurance Top Up Credits. But just been told by Carer’s Allowance Team I can’t claim retrospectively!

I found out I would be approx £60 a month better off if I topped up.

But I would need to pay nearly £10,000 to top up to my full State Pension!

I decided to retire early to look after my husband with Cancer & then Dementia. I had 3 years 2011 to 2014 when he had Lymphoma & Stem Cell Transplant, then from 2015 early on set Dementia/Alzheimer’s till death late in 2020. I didn’t know about claiming Carer’s Credits to top up my National Insurance Top Up Credits. But just been told by Carer’s Allowance Team I can’t claim retrospectively!

I found out I would be approx £60 a month better off if I topped up.

But I would need to pay nearly £10,000 to top up to my full State Pension!

So according to my calculations I would only break even in 14 years when I’m 84? I already have the State Pension, plus my own small private pensions & my late husband’s Works Pension.

I have £10,000 saved, but my question is would I be better off spending the money on topping up for an extra £60 p month in my Pension? Or spending the money on things like holidays or towards a new car, things that I want to do now whilst I am still able to?

I have £10,000 saved, but my question is would I be better off spending the money on topping up for an extra £60 p month in my Pension? Or spending the money on things like holidays or towards a new car, things that I want to do now whilst I am still able to?

0

Comments

-

Incorrect.kimwp said:I think if you are already claiming your state pension, you can no longer top it up.oliveoil54 said:I am 70, after watching Martin’s show last night I had a look to see what my NI Situation is.

I decided to retire early to look after my husband with Cancer & then Dementia.

I found out I would be approx £60 a month better off if I topped up.

But I would need to pay nearly £10,000 to top up to my full State Pension!So according to my calculations I would only break even in 14 years when I’m 84? I already have the State Pension, plus my own small private pensions & my late husband’s Works Pension.

I have £10,000 saved, but my question is would I be better off spending the money on topping up for an extra £60 p month in my Pension? Or spending the money on things like holidays or towards a new car, things that I want to do now whilst I am still able to?That does not sound right, £60 per month - the pension is paid 4 weekly not monthly - for £10K is not possible. Voluntary contributions usually break even in under 3 years - £10K would buy something like £75+ per week. If you post up some anonymous info someone will helpCurrent weekly £££.pp amount.

Number of full NI years 15-16 and earlier

Number of full NI years 16-17 and later

Tax year you reached state retirement

Were you in a contracted-out pension scheme - something like NHS, local government, civil service ?

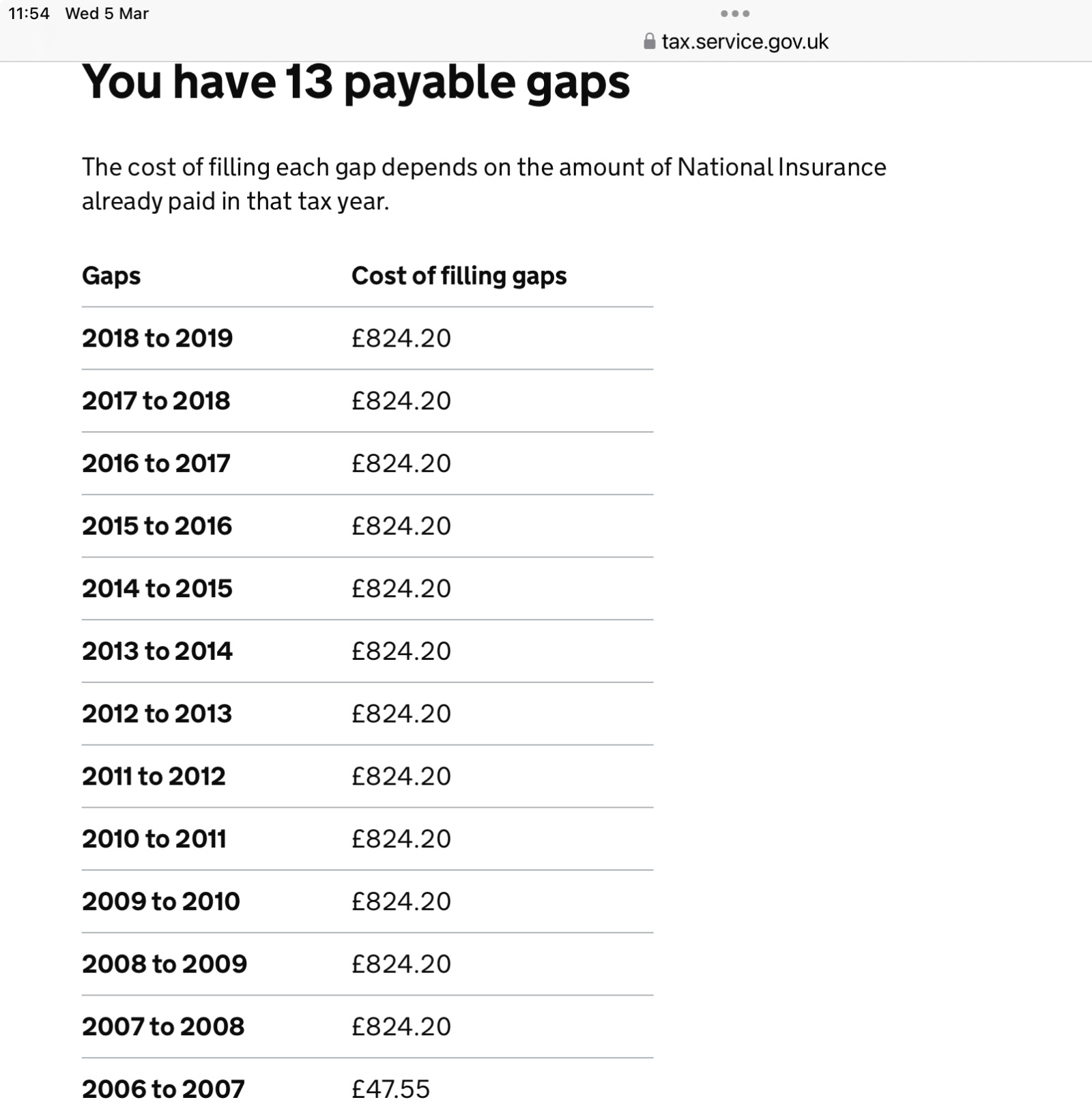

Years which show not full and prices

1 -

Thank you for your prompt reply I’ve attached the years I’ve paid in full & what it says I owe? Current weekly rate £206, mine & my late husband’s works pensions were with British Aerospace & yes I think they did contract out, but can’t remember the details. Reached State Pension age Nov 2019.molerat said:

Incorrect.kimwp said:I think if you are already claiming your state pension, you can no longer top it up.oliveoil54 said:I am 70, after watching Martin’s show last night I had a look to see what my NI Situation is.

I decided to retire early to look after my husband with Cancer & then Dementia.

I found out I would be approx £60 a month better off if I topped up.

But I would need to pay nearly £10,000 to top up to my full State Pension!So according to my calculations I would only break even in 14 years when I’m 84? I already have the State Pension, plus my own small private pensions & my late husband’s Works Pension.

I have £10,000 saved, but my question is would I be better off spending the money on topping up for an extra £60 p month in my Pension? Or spending the money on things like holidays or towards a new car, things that I want to do now whilst I am still able to?That does not sound right, £60 per month - the pension is paid 4 weekly not monthly - for £10K is not possible. Voluntary contributions usually break even in under 3 years - £10K would buy something like £75+ per week. If you post up some anonymous info someone will helpCurrent weekly £££.pp amount.

Number of full NI years 15-16 and earlier

Number of full NI years 16-17 and later

Tax year you reached state retirement

Were you in a contracted-out pension scheme - something like NHS, local government, civil service ?

Years which show not full and prices

0

0 -

Exactly £206, no pence? From that you need 3 years to get the full pension amount so it will cost you £2500. 2 will add £6.32 per week each and the third will top up to £221.20. You can only use those final 3 years, 2015-16 and earlier will not add to the pension . You now need to contact The Pension Service for them to write to you, as long as you have contacted them before 5 April the window should stay open. It could take up to a year for the new amount to come into payment but it will be backdated to the receipt of your contributions.1

-

Yes think it was about £00.07, didn’t realise you’d need the exact sum. Thankyou so much for your advice, lm not normally stupid, but do find the tax forms totally confusing! I’ll wait a few days till the effect of Martin’s recent show has worn off, as they are quoting over an hour’s wait on their telephone line! Once again thanks for taking the time to help me out!molerat said:Exactly £206, no pence? From that you need 3 years to get the full pension amount so it will cost you £2500. 2 will add £6.32 per week each and the third will top up to £221.20. You can only use those final 3 years, 2015-16 and earlier will not add to the pension . You now need to contact The Pension Service for them to write to you, as long as you have contacted them before 5 April the window should stay open. It could take up to a year for the new amount to come into payment but it will be backdated to the receipt of your contributions.0 -

The exact figure decides how much the final year is worth. The first 2 will give £6.32 each and the third only £2.49. Buying 2 will take 130 weeks to recover the outlay gross, buying the 3 will take 163 weeks. That is of course ignoring the inflationary uplifts each year.1

-

you can register for a callback.oliveoil54 said:

Yes think it was about £00.07, didn’t realise you’d need the exact sum. Thankyou so much for your advice, lm not normally stupid, but do find the tax forms totally confusing! I’ll wait a few days till the effect of Martin’s recent show has worn off, as they are quoting over an hour’s wait on their telephone line! Once again thanks for taking the time to help me out!molerat said:Exactly £206, no pence? From that you need 3 years to get the full pension amount so it will cost you £2500. 2 will add £6.32 per week each and the third will top up to £221.20. You can only use those final 3 years, 2015-16 and earlier will not add to the pension . You now need to contact The Pension Service for them to write to you, as long as you have contacted them before 5 April the window should stay open. It could take up to a year for the new amount to come into payment but it will be backdated to the receipt of your contributions.

Here’s the form you need from DWP in order to register that you want a call back about boosting your state pension. Do this and if they don’t get back before 5 April deadline you’re fine… https://secure.dwp.gov.uk/request-a-call.../contact-formI’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.0 -

I wouldn’t wait a few days, it’s only going to get busier as the deadline looms.oliveoil54 said:

Yes think it was about £00.07, didn’t realise you’d need the exact sum. Thankyou so much for your advice, lm not normally stupid, but do find the tax forms totally confusing! I’ll wait a few days till the effect of Martin’s recent show has worn off, as they are quoting over an hour’s wait on their telephone line! Once again thanks for taking the time to help me out!molerat said:Exactly £206, no pence? From that you need 3 years to get the full pension amount so it will cost you £2500. 2 will add £6.32 per week each and the third will top up to £221.20. You can only use those final 3 years, 2015-16 and earlier will not add to the pension . You now need to contact The Pension Service for them to write to you, as long as you have contacted them before 5 April the window should stay open. It could take up to a year for the new amount to come into payment but it will be backdated to the receipt of your contributions.Fashion on the Ration

2024 - 43/66 coupons used, carry forward 23

2025 - 62/890 -

the effect won't wear off, it'll get worse.oliveoil54 said:

Yes think it was about £00.07, didn’t realise you’d need the exact sum. Thankyou so much for your advice, lm not normally stupid, but do find the tax forms totally confusing! I’ll wait a few days till the effect of Martin’s recent show has worn off, as they are quoting over an hour’s wait on their telephone line! Once again thanks for taking the time to help me out!molerat said:Exactly £206, no pence? From that you need 3 years to get the full pension amount so it will cost you £2500. 2 will add £6.32 per week each and the third will top up to £221.20. You can only use those final 3 years, 2015-16 and earlier will not add to the pension . You now need to contact The Pension Service for them to write to you, as long as you have contacted them before 5 April the window should stay open. It could take up to a year for the new amount to come into payment but it will be backdated to the receipt of your contributions.

We've already been through this scenario once before a couple of years ago, before they extended the deadline - I can't imagine that they will do that again.0 -

There will be those shouting for another extension, unlikely to be given.p00hsticks said:

the effect won't wear off, it'll get worse.oliveoil54 said:

Yes think it was about £00.07, didn’t realise you’d need the exact sum. Thankyou so much for your advice, lm not normally stupid, but do find the tax forms totally confusing! I’ll wait a few days till the effect of Martin’s recent show has worn off, as they are quoting over an hour’s wait on their telephone line! Once again thanks for taking the time to help me out!molerat said:Exactly £206, no pence? From that you need 3 years to get the full pension amount so it will cost you £2500. 2 will add £6.32 per week each and the third will top up to £221.20. You can only use those final 3 years, 2015-16 and earlier will not add to the pension . You now need to contact The Pension Service for them to write to you, as long as you have contacted them before 5 April the window should stay open. It could take up to a year for the new amount to come into payment but it will be backdated to the receipt of your contributions.

We've already been through this scenario once before a couple of years ago, before they extended the deadline - I can't imagine that they will do that again.

There must be more than the couple of people I know who have deliberately left it right to the wire, in order to accrue as much savings interest as possible before divvying up.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards