We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Offset mortgage and the Ombudsman

Comments

-

I don't think that is right, it is important that there is no interest earned on the offset balance as it would be subject to taxation if it was...silvercar said:DullGreyGuy said:

But if you dont accept that junior person's decision it goes to an Ombudsman who is certainly not a junior person. Most the ones I know have 15-20 years in industry before working for the ombudsman, all hold qualification with a Chartered Institute for their relevant field or are legally trained. Like any organisation, some start at the bottom and work their way upHalevie1 said:

I suspect that will end up being the case. My wife is a financial accountant and I've been in corporate finance for my career, as well as running a property business and had many offset mortgages.... but apparently a junior person in the FOS just accepts what a junior person in IF/Lloyds Bank says. Ironic as the ex-CEO of Lloyds Bank agrees with me!grumpy_codger said:

Cannot the the claimant support the claim with some expert statement? In this case the judge will probably need some other expert opinion to dismiss such statement.silvercar said:Of course the risk is the judge doesn’t understand the intricacies of an offset mortgage in the same way as the ombudsman didn’t.

That is not to say none have ever made mistakes but it would be highly improbable that three different ones have made the same mistake.What the issue is, is that Z% isn’t the same for the mortgage and the savings accounts when it should be.It has to be the balances that are offset not earned interest vs paid interest.0 -

It's mathematically equal but it's not the same thing and wouldn't have the same tax treatment. Coincidently a while back our savings and mortgage (not with the same bank) had the same interest but the interest on my savings are taxed and I dont get a waiver just because I have a debt with the same interest rate.silvercar said:

Even Halevie1 is focussing on (X-Y)xZ%, whereas my XxZ%-YxZ% gives the same result. What the issue is, is that Z% isn’t the same for the mortgage and the savings accounts when it should be.

It's important that the interest on the savings doesn't exist and instead the interest on the loan is waived as waived debt interest isnt taxable.0 -

MWT said:

I don't think that is right, it is important that there is no interest earned on the offset balance as it would be subject to taxation if it was...silvercar said:DullGreyGuy said:

But if you dont accept that junior person's decision it goes to an Ombudsman who is certainly not a junior person. Most the ones I know have 15-20 years in industry before working for the ombudsman, all hold qualification with a Chartered Institute for their relevant field or are legally trained. Like any organisation, some start at the bottom and work their way upHalevie1 said:

I suspect that will end up being the case. My wife is a financial accountant and I've been in corporate finance for my career, as well as running a property business and had many offset mortgages.... but apparently a junior person in the FOS just accepts what a junior person in IF/Lloyds Bank says. Ironic as the ex-CEO of Lloyds Bank agrees with me!grumpy_codger said:

Cannot the the claimant support the claim with some expert statement? In this case the judge will probably need some other expert opinion to dismiss such statement.silvercar said:Of course the risk is the judge doesn’t understand the intricacies of an offset mortgage in the same way as the ombudsman didn’t.

That is not to say none have ever made mistakes but it would be highly improbable that three different ones have made the same mistake.What the issue is, is that Z% isn’t the same for the mortgage and the savings accounts when it should be.It has to be the balances that are offset not earned interest vs paid interest.

Hmm. Maybe I should put a complaint in, as I am charged a small amount of interest when the rate increases based on the previous month's offset balance interest calculation being lower than the interest due on the increased mortgage rate in the new month.DullGreyGuy said:

It's mathematically equal but it's not the same thing and wouldn't have the same tax treatment. Coincidently a while back our savings and mortgage (not with the same bank) had the same interest but the interest on my savings are taxed and I dont get a waiver just because I have a debt with the same interest rate.silvercar said:

Even Halevie1 is focussing on (X-Y)xZ%, whereas my XxZ%-YxZ% gives the same result. What the issue is, is that Z% isn’t the same for the mortgage and the savings accounts when it should be.

It's important that the interest on the savings doesn't exist and instead the interest on the loan is waived as waived debt interest isnt taxable.

The basic point stands, @Halevie1 is being credited a much lower interest rate on his offset savings. Rather than the savings being netted off the outstanding mortgage balance.I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.0 -

We don't need the mortgage. The house is paid off. That is why the mortgage is fully offset. The long term issue for many years is that IF has not been able to explain its many charges (transfers between accounts, payments to reduce capital, etc that a customer cannot wort out). The interest calculation on the offset mortgage is just one of them. That is why I have left it fully offset for two years - to show that there is a problem because IF continues to charge interest.silvercar said:In your shoes I would look to move to another offset mortgage elsewhere. That way you can calculate the loss that has occurred and you could go to the small claims court to get it back. Until you end the mortgage with IF you don’t know how much this has costed you. By keeping your mortgage with IF it’s costing you each month. In fact, if you don’t have another use for the money, you could just clear your mortgage.

What I wouldn’t do is stay with IF and accept the 1.7% savings rate.0 -

Which would then involve the mortgage lender in a whole raft of additional administration. When the account was originally launched (a different era) the interest would have been taxable at source.MWT said:

I don't think that is right, it is important that there is no interest earned on the offset balance as it would be subject to taxation if it was...silvercar said:DullGreyGuy said:

But if you dont accept that junior person's decision it goes to an Ombudsman who is certainly not a junior person. Most the ones I know have 15-20 years in industry before working for the ombudsman, all hold qualification with a Chartered Institute for their relevant field or are legally trained. Like any organisation, some start at the bottom and work their way upHalevie1 said:

I suspect that will end up being the case. My wife is a financial accountant and I've been in corporate finance for my career, as well as running a property business and had many offset mortgages.... but apparently a junior person in the FOS just accepts what a junior person in IF/Lloyds Bank says. Ironic as the ex-CEO of Lloyds Bank agrees with me!grumpy_codger said:

Cannot the the claimant support the claim with some expert statement? In this case the judge will probably need some other expert opinion to dismiss such statement.silvercar said:Of course the risk is the judge doesn’t understand the intricacies of an offset mortgage in the same way as the ombudsman didn’t.

That is not to say none have ever made mistakes but it would be highly improbable that three different ones have made the same mistake.What the issue is, is that Z% isn’t the same for the mortgage and the savings accounts when it should be.

Why would a lender give somebody a savings interest rate at the same rate they are charging borrowers. That immediately loses them money. No commercal logic.0 -

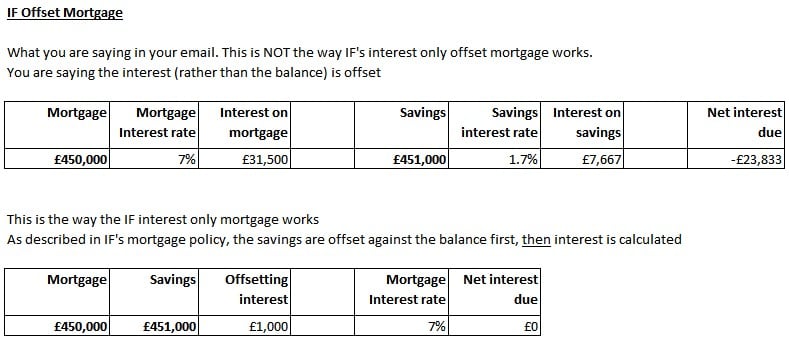

There are a lot of comments from people saying "the interest from the savings account is offset against the interest from the mortgage account". That isn't how offset mortgages work. If it did, either the interest on a mortgage account (say 6-7% currently) would require the interest on a savings account to be the same. Hight street banks/lenders make their money by the difference between savings and borrowing rates.

Offset mortgages work by offsetting the savings capital against the loan capital. So you use your savings to reduce your interest payments on the mortgage capital, thus reducing your mortgage interest and avoiding paying tax on your savings income. At the calculations show below. A fully offset mortgage with the capital offset results in no payments. That is obvious and makes sense. If the offsetting was the interest, you would be paying interest on a fully offset mortgage because of the differential rates between mortgage and savings accounts. The advantage of an offset account is that you can access money, up to the mortgage value, and pay for access to that capital at the mortgage rate. For me, this is what the value was as I wanted access to lump sums to invest in units and property, make a return, then put the profits back into the savings account. To do that without an offset mortgage would have been difficult and more expensive.

0 -

People are people. Not all manage their personal finances well.silvercar said:

User error.Hoenir said:

The first was the Virgin One Account that operated in the manner of a current account with a huge overdraft facility. Seem to recall this concept hit the rocks. With many people struggling to operate the account in the manner it was intended. Some years ago compensation was paid to affected borrowers.silvercar said:

In the days when offsets were more popular (I took mine in the late 1990s, so around then maybe) there were 2 distinct types. Those where there was an mortgage account and a savings account, the interest being charged on the difference between the two and those that were operated more like a current account, so all your debits and credits went through something like a current account and you paid interest on the outstanding amount. I know First Direct did the latter sort, and by the sound of it so did Intelligent Finance. It seems like IF may have had both a current account and a savings account attached to the mortgage account, but the principle was the same.Hoenir said:

In my personal experience it isn't. I took out an offset mortgage with the Hinckley & Rugby Building Society in July 2007. The way the offset worked (as I would expect it to from a financial system POV) . Was that the interest on the balance in the offset account earnt interest on a daily basis. Once a month this interest was credited to the mortgage loan accunt. The interest rate being that equivalent to the rate charged on the mortgage.Halevie1 said:

It clearly isn't right to be offsetting the interest rather than the capital value as that is the whole point of an offset mortgage.

In our case. No interest was earnt on any offset balance that exceeded the mount owed on the mortgage.

There's no possibility that the IF mortgage system was capable of doing what you expected it to do. That's not how the financial world works. The two accounts, mortgage and offset would have been totally unrelated. Imagine the complexity if a system had to look at the mortgage account on a daily basis and cross reference this to a savings account. In order to calculate the amount of interest to charge at the end of any given period. Mind boggling complex. Would have incurred a huge expense in computer programming as well.0 -

This sounds to me like an issue where as IF have gradually closed down their operation over the past 15 years years, the remaining account options are not producing the Offset benefits as previously.

The problem for the OP, as stated previously, is that a rejected complaint to both the Lender and the FOS (which I assume has been appealed by the OP) is achieving nothing - a Court case would be expensive, time consuming and not guaranteed to be successful..

If the funds are in place to offset in full, why not simply repay and, if offset facility is still required, switch to another Lender (assuming a new mortgage can be secured based on income).I am a Mortgage Broker

You should note that this site doesn't check my status as a Mortgage Broker, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.1 -

This is what I would do.amnblog said:This sounds to me like an issue where as IF have gradually closed down their operation over the past 15 years years, the remaining account options are not producing the Offset benefits as previously.

The problem for the OP, as stated previously, is that a rejected complaint to both the Lender and the FOS (which I assume has been appealed by the OP) is achieving nothing - a Court case would be expensive, time consuming and not guaranteed to be successful..

If the funds are in place to offset in full, why not simply repay and, if offset facility is still required, switch to another Lender (assuming a new mortgage can be secured based on income).

Keeping the ongoing IF mortgage just results in you being charged interest that shouldn't be charged. You can take this further through the courts or writing to one of the newspapers that have money advice columns etc. You will either win or you will lose. If you win, IF should refund all the erroneous charges, if you lose then you don't get the money back. Just because there is never 100% guarantee you will win, I would move to a new lender. I can't see any harm at crystalizing what you have lost at this point. There are other lenders who operate offset mortgages, shift to one of them.I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.0 -

https://www.thisismoney.co.uk/money/mortgageshome/article-14418493/We-owe-300-000-offset-mortgage-save-money-DAVID-HOLLINGWORTH-replies.html

- nothing special, just some new article on offset mortgages0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards