We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

My initial plan to retire at 59 hoping for some advice

Comments

-

Please check your state pension forecast again, what does it actually say? You will have been 'contracted out' during your employment and may need more years than you think for a full state pension.Twigwidge said:Many thanks to everyone that has replied so quickly, as I mentioned I am on a very steep learning curve here so all these comments/advice are very gratefully received 😊. This is rather long as I wanted to reply to the initial comments

@QrizB, unfortunately the only other savings I have are just under 10K in a cash ISA, as I have been using all spare cash over last few years to finish paying off mortgage (which is now paid)

@Dazed_and_C0nfused, yes this amount does have an actuarial reduction because of age and also a penalty for going before the age of 60 (explained below)

Here is my USS model prediction (hope I am allowed to post this)

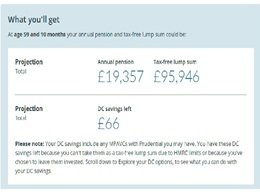

£18.239 gross pension = £17,105 net = Just over £1,400 a month

The maximum tax free lump sum of 121,595 will be topped up to £151,000 by a tax-free voluntary severance payment of £30,000 to £151,000

@Dazed_and_C0nfused, I am not sure what tax code would be used, I have heard that some people initially are put on an emergency tax code but claim any overpayments back, how would I find out what tax code I would be on? Yes this £1,400 would be net (assuming my calculations above are correct)

@LL_USS, As far as I understand the USS pension rules (and they are not easy to understand to me 😊) I seem to be better off taking the maximum tax free lump sum as USS (appear) to give a one off opportunity (I think this is what GrumpyDill is referring to?) of taking most of my defined contribution savings tax free (note on USS model screenshot that my DC pot is at Zero if I take the maximum TF lump sum)

@Phossy, yes initially I will put all my tax free money into a 4% savings account and the transfer over a few years into both mine and my partner’s ISA allowances 😊 Yes I agree about savings protection and will definitely split initial savings over 2 accounts to benefit from the £85,000 FSCS protection

@Linton and Marcon, aside from near 10k in an ISA I have no other savings or pension pots of any kind and I have checked my state pension forecast and will have 34 full years at time of retirement 31st July) so I will need to top up 1 year eventually to get full state pension. I think there is a 10% cap on USS pension increases but it is not entirely clear on their website.

@Marcon I had no real opportunity to save since all extra cash has been used to finish paying off my mortgage, so just under 10K in an ISA and that’s all my savings, I will certainly max out both mine and partners ISAs when my lump sum is paid 😊 Sorry about the £ sign, I was typing my initial post on my phone and it is a nightmare to access the symbols, I will edit the original post later this evening if I can work out how to do this 😊

@Abermarle, Yes I could take slightly more pension and less lump sum, the maximum DB pension I can take is £19,357 gross (see screenshot below)

This would be a fraction under £18,000 net (£17,999) = bang on £1,500 per month net

But obviously this reduces my lump sum by £25,649 (121,595-95,946)

If I went down this route the total going into my savings would now be £95,946+£30,000 (severance) = £125,946

So if I put this in my savings account to top my pension up to my desired £2,500 per month I need £1,000 per month for 7 years (to state pension)

1,000 x 12 x 7 = £84,000 = This would leave £41,946 of my lump left at state pension age

After playing with the modeller to me it seems the most sensible choice for me was to take the maximum lump sum as taking the maximum pension would only give me an additional £75 per month (net) but result in a loss of 25.5K lump sum (I guess it is just personal choice in the end). I think this is what @Secret2ndAccount is indicating later in the thread as the reverse commutation factor is so poor

@Barralad77, I would love to take my pension at 60 to avoid the penalty but if I want the severance package like many Universities I have to take it by 31st July (a few months before I turn 60) I have looked into this with the Uni but they won't budge on this. I was hoping that if I still went on 31st July but deferred taking my pension until after I was 60 that this may be a way around the early penalty but after speaking with the USS advisor on the phone, deferring the pension immediately triggers the early penalty. I don't think there is any way around this (unless anyone knows better). For me I am willing to take the hit to get the severance package 😊

@Secret2ndAccount, Yes I certainly will be looking at other places to put the lump sum, I just have a feeling that investments in the current world economic climate may be a bit more risky than usual so probably safer in ISAs and the highest interest savings accounts I can get.

Thanks so much everyone for taking the time to reply

0 -

The issue here is whether or not someone leaves while still an active member and takes their pension immediately (as opposed to taking their pension from deferred status) - not the actual hours they are working or the length of the extra service they clock up if working part time.Barralad77 said:Re. The point about losing out even if you defer taking it until you’ve turned 60. I learnt the same thing long after I’d spent years believing otherwise. It’s really annoying and I’ve never known what the reasoning behind it is. In terms of you discussing the possibility of staying on a few months longer, have you asked whether they’d accept you reducing your hours such that you would still be working a further 6.0FTE months? For example, if you needed to stay working until the end of December, would they allow you to drop down to, say, 0.5 for 10 months? So rather than earn 6 x 1.0 (Feb-July) you would work 1 x 1.0 (Feb) plus 10 x 0.5 (Mar-Dec). They both work out at 6.0 FTE months. Obviously, there are other factors to consider but it’s something I’d consider pursuing (if you’re losing out quite a bit on the pension for the sake of a handful of months).

Normally retiring from active membership (or, in some schemes, shortly leaving active membership) gives a 'better' early retirement reduction factor for the member than retiring from deferred status.

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!2 -

Yes, that’s my point. If you leave one day after turning 60 the ER factor will be bettter. If you leave 24 hours early (59 years and 364 days) it will be worse. Finish at 59 years and the normal pension age for that portion of the contributions will be deemed to be 63.5. Take it at 60 and it will be taken as 60 (I.e.. zero reduction applied). The difference in pension benefits accrued (1.0 vs 0.5) for a few months will barely be noticeable in the big scheme of things.Marcon said:

The issue here is whether or not someone leaves while still an active member and takes their pension immediately (as opposed to taking their pension from deferred status) - not the actual hours they are working or the length of the extra service they clock up if working part time.Barralad77 said:Re. The point about losing out even if you defer taking it until you’ve turned 60. I learnt the same thing long after I’d spent years believing otherwise. It’s really annoying and I’ve never known what the reasoning behind it is. In terms of you discussing the possibility of staying on a few months longer, have you asked whether they’d accept you reducing your hours such that you would still be working a further 6.0FTE months? For example, if you needed to stay working until the end of December, would they allow you to drop down to, say, 0.5 for 10 months? So rather than earn 6 x 1.0 (Feb-July) you would work 1 x 1.0 (Feb) plus 10 x 0.5 (Mar-Dec). They both work out at 6.0 FTE months. Obviously, there are other factors to consider but it’s something I’d consider pursuing (if you’re losing out quite a bit on the pension for the sake of a handful of months).0 -

That is a good point and I certainly will be exploring all options over the next couple of months, stupidly I left getting my head around retirement options to the last minute and playing catch upAlbermarle said:On the last point, the current global economic and political climate always looks risky, whenever you look at it. However most often markets just shrug it off. They are more interested in how many I phones Apple sell than the war in Gaza, Ukraine etc.

Over the long term it is actually more risky holding on to too much cash.0 -

But you don't need to work get any particular number of FTE months as your post suggested - that was the bit I was clarifying:Barralad77 said:

Yes, that’s my point. If you leave one day after turning 60 the ER factor will be bettter. If you leave 24 hours early (59 years and 364 days) it will be worse. Finish at 59 years and the normal pension age for that portion of the contributions will be deemed to be 63.5. Take it at 60 and it will be taken as 60 (I.e.. zero reduction applied). The difference in pension benefits accrued (1.0 vs 0.5) for a few months will barely be noticeable in the big scheme of things.Marcon said:

The issue here is whether or not someone leaves while still an active member and takes their pension immediately (as opposed to taking their pension from deferred status) - not the actual hours they are working or the length of the extra service they clock up if working part time.Barralad77 said:Re. The point about losing out even if you defer taking it until you’ve turned 60. I learnt the same thing long after I’d spent years believing otherwise. It’s really annoying and I’ve never known what the reasoning behind it is. In terms of you discussing the possibility of staying on a few months longer, have you asked whether they’d accept you reducing your hours such that you would still be working a further 6.0FTE months? For example, if you needed to stay working until the end of December, would they allow you to drop down to, say, 0.5 for 10 months? So rather than earn 6 x 1.0 (Feb-July) you would work 1 x 1.0 (Feb) plus 10 x 0.5 (Mar-Dec). They both work out at 6.0 FTE months. Obviously, there are other factors to consider but it’s something I’d consider pursuing (if you’re losing out quite a bit on the pension for the sake of a handful of months).Barralad77 said:For example, if you needed to stay working until the end of December, would they allow you to drop down to, say, 0.5 for 10 months? So rather than earn 6 x 1.0 (Feb-July) you would work 1 x 1.0 (Feb) plus 10 x 0.5 (Mar-Dec). They both work out at 6.0 FTE months.

The point is that normally you simply need to be in active membership of a scheme at the point of taking your benefits, so OP would only need to work to 31 December if that's the 'magic birthday' date (unless there's something very odd about USS!).

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

Thanks for this suggestion Barralad77 I will certainly ask the Uni, not holding out too much hope thoughBarralad77 said:Re. The point about losing out even if you defer taking it until you’ve turned 60. I learnt the same thing long after I’d spent years believing otherwise. It’s really annoying and I’ve never known what the reasoning behind it is. In terms of you discussing the possibility of staying on a few months longer, have you asked whether they’d accept you reducing your hours such that you would still be working a further 6.0FTE months? For example, if you needed to stay working until the end of December, would they allow you to drop down to, say, 0.5 for 10 months? So rather than earn 6 x 1.0 (Feb-July) you would work 1 x 1.0 (Feb) plus 10 x 0.5 (Mar-Dec). They both work out at 6.0 FTE months. Obviously, there are other factors to consider but it’s something I’d consider pursuing (if you’re losing out quite a bit on the pension for the sake of a handful of months).1 -

Twigwidge said:

@LL_USS, As far as I understand the USS pension rules (and they are not easy to understand to me 😊) I seem to be better off taking the maximum tax free lump sum as USS (appear) to give a one off opportunity (I think this is what GrumpyDill is referring to?) of taking most of my defined contribution savings tax free (note on USS model screenshot that my DC pot is at Zero if I take the maximum TF lump sum)

I started googling everywhere about TFLS earlier today until other people here said it depends on each pension scheme. And yes when I checked with USS (https://www.uss.co.uk/for-members/pension-tax/income-tax-in-retirement) it does say a couple of time "one-off cash lump sum). It's great in your case you can take out all the DC pot tax free. Seems you've been convinced to take max TFLS. It's been already discussed elsewhere in MFS that in general the commutation rate is not great when you buy more DB (like in your 2nd illustration). I was about to ask about the figure of 151K then realised you add 121K (illustration 1) with the 30K severance.I hope you can sort out the sticky point of a couple of months short to 60 to push the R button.Well, I learn new things today thanks to your thread :-), thanks.1 -

BrilliantButScary said:

Please check your state pension forecast again, what does it actually say? You will have been 'contracted out' during your employment and may need more years than you think for a full state pension.Twigwidge said:Many thanks to everyone that has replied so quickly, as I mentioned I am on a very steep learning curve here so all these comments/advice are very gratefully received 😊. This is rather long as I wanted to reply to the initial comments

@QrizB, unfortunately the only other savings I have are just under 10K in a cash ISA, as I have been using all spare cash over last few years to finish paying off mortgage (which is now paid)

@Dazed_and_C0nfused, yes this amount does have an actuarial reduction because of age and also a penalty for going before the age of 60 (explained below)

Here is my USS model prediction (hope I am allowed to post this)

£18.239 gross pension = £17,105 net = Just over £1,400 a month

The maximum tax free lump sum of 121,595 will be topped up to £151,000 by a tax-free voluntary severance payment of £30,000 to £151,000

@Dazed_and_C0nfused, I am not sure what tax code would be used, I have heard that some people initially are put on an emergency tax code but claim any overpayments back, how would I find out what tax code I would be on? Yes this £1,400 would be net (assuming my calculations above are correct)

@LL_USS, As far as I understand the USS pension rules (and they are not easy to understand to me 😊) I seem to be better off taking the maximum tax free lump sum as USS (appear) to give a one off opportunity (I think this is what GrumpyDill is referring to?) of taking most of my defined contribution savings tax free (note on USS model screenshot that my DC pot is at Zero if I take the maximum TF lump sum)

@Phossy, yes initially I will put all my tax free money into a 4% savings account and the transfer over a few years into both mine and my partner’s ISA allowances 😊 Yes I agree about savings protection and will definitely split initial savings over 2 accounts to benefit from the £85,000 FSCS protection

@Linton and Marcon, aside from near 10k in an ISA I have no other savings or pension pots of any kind and I have checked my state pension forecast and will have 34 full years at time of retirement 31st July) so I will need to top up 1 year eventually to get full state pension. I think there is a 10% cap on USS pension increases but it is not entirely clear on their website.

@Marcon I had no real opportunity to save since all extra cash has been used to finish paying off my mortgage, so just under 10K in an ISA and that’s all my savings, I will certainly max out both mine and partners ISAs when my lump sum is paid 😊 Sorry about the £ sign, I was typing my initial post on my phone and it is a nightmare to access the symbols, I will edit the original post later this evening if I can work out how to do this 😊

@Abermarle, Yes I could take slightly more pension and less lump sum, the maximum DB pension I can take is £19,357 gross (see screenshot below)

This would be a fraction under £18,000 net (£17,999) = bang on £1,500 per month net

But obviously this reduces my lump sum by £25,649 (121,595-95,946)

If I went down this route the total going into my savings would now be £95,946+£30,000 (severance) = £125,946

So if I put this in my savings account to top my pension up to my desired £2,500 per month I need £1,000 per month for 7 years (to state pension)

1,000 x 12 x 7 = £84,000 = This would leave £41,946 of my lump left at state pension age

After playing with the modeller to me it seems the most sensible choice for me was to take the maximum lump sum as taking the maximum pension would only give me an additional £75 per month (net) but result in a loss of 25.5K lump sum (I guess it is just personal choice in the end). I think this is what @Secret2ndAccount is indicating later in the thread as the reverse commutation factor is so poor

@Barralad77, I would love to take my pension at 60 to avoid the penalty but if I want the severance package like many Universities I have to take it by 31st July (a few months before I turn 60) I have looked into this with the Uni but they won't budge on this. I was hoping that if I still went on 31st July but deferred taking my pension until after I was 60 that this may be a way around the early penalty but after speaking with the USS advisor on the phone, deferring the pension immediately triggers the early penalty. I don't think there is any way around this (unless anyone knows better). For me I am willing to take the hit to get the severance package 😊

@Secret2ndAccount, Yes I certainly will be looking at other places to put the lump sum, I just have a feeling that investments in the current world economic climate may be a bit more risky than usual so probably safer in ISAs and the highest interest savings accounts I can get.

Thanks so much everyone for taking the time to reply

@BrilliantButScaryBrilliantButScary said:

Please check your state pension forecast again, what does it actually say? You will have been 'contracted out' during your employment and may need more years than you think for a full state pension.Twigwidge said:Many thanks to everyone that has replied so quickly, as I mentioned I am on a very steep learning curve here so all these comments/advice are very gratefully received 😊. This is rather long as I wanted to reply to the initial comments

@QrizB, unfortunately the only other savings I have are just under 10K in a cash ISA, as I have been using all spare cash over last few years to finish paying off mortgage (which is now paid)

@Dazed_and_C0nfused, yes this amount does have an actuarial reduction because of age and also a penalty for going before the age of 60 (explained below)

Here is my USS model prediction (hope I am allowed to post this)

£18.239 gross pension = £17,105 net = Just over £1,400 a month

The maximum tax free lump sum of 121,595 will be topped up to £151,000 by a tax-free voluntary severance payment of £30,000 to £151,000

@Dazed_and_C0nfused, I am not sure what tax code would be used, I have heard that some people initially are put on an emergency tax code but claim any overpayments back, how would I find out what tax code I would be on? Yes this £1,400 would be net (assuming my calculations above are correct)

@LL_USS, As far as I understand the USS pension rules (and they are not easy to understand to me 😊) I seem to be better off taking the maximum tax free lump sum as USS (appear) to give a one off opportunity (I think this is what GrumpyDill is referring to?) of taking most of my defined contribution savings tax free (note on USS model screenshot that my DC pot is at Zero if I take the maximum TF lump sum)

@Phossy, yes initially I will put all my tax free money into a 4% savings account and the transfer over a few years into both mine and my partner’s ISA allowances 😊 Yes I agree about savings protection and will definitely split initial savings over 2 accounts to benefit from the £85,000 FSCS protection

@Linton and Marcon, aside from near 10k in an ISA I have no other savings or pension pots of any kind and I have checked my state pension forecast and will have 34 full years at time of retirement 31st July) so I will need to top up 1 year eventually to get full state pension. I think there is a 10% cap on USS pension increases but it is not entirely clear on their website.

@Marcon I had no real opportunity to save since all extra cash has been used to finish paying off my mortgage, so just under 10K in an ISA and that’s all my savings, I will certainly max out both mine and partners ISAs when my lump sum is paid 😊 Sorry about the £ sign, I was typing my initial post on my phone and it is a nightmare to access the symbols, I will edit the original post later this evening if I can work out how to do this 😊

@Abermarle, Yes I could take slightly more pension and less lump sum, the maximum DB pension I can take is £19,357 gross (see screenshot below)

This would be a fraction under £18,000 net (£17,999) = bang on £1,500 per month net

But obviously this reduces my lump sum by £25,649 (121,595-95,946)

If I went down this route the total going into my savings would now be £95,946+£30,000 (severance) = £125,946

So if I put this in my savings account to top my pension up to my desired £2,500 per month I need £1,000 per month for 7 years (to state pension)

1,000 x 12 x 7 = £84,000 = This would leave £41,946 of my lump left at state pension age

After playing with the modeller to me it seems the most sensible choice for me was to take the maximum lump sum as taking the maximum pension would only give me an additional £75 per month (net) but result in a loss of 25.5K lump sum (I guess it is just personal choice in the end). I think this is what @Secret2ndAccount is indicating later in the thread as the reverse commutation factor is so poor

@Barralad77, I would love to take my pension at 60 to avoid the penalty but if I want the severance package like many Universities I have to take it by 31st July (a few months before I turn 60) I have looked into this with the Uni but they won't budge on this. I was hoping that if I still went on 31st July but deferred taking my pension until after I was 60 that this may be a way around the early penalty but after speaking with the USS advisor on the phone, deferring the pension immediately triggers the early penalty. I don't think there is any way around this (unless anyone knows better). For me I am willing to take the hit to get the severance package 😊

@Secret2ndAccount, Yes I certainly will be looking at other places to put the lump sum, I just have a feeling that investments in the current world economic climate may be a bit more risky than usual so probably safer in ISAs and the highest interest savings accounts I can get.

Thanks so much everyone for taking the time to reply

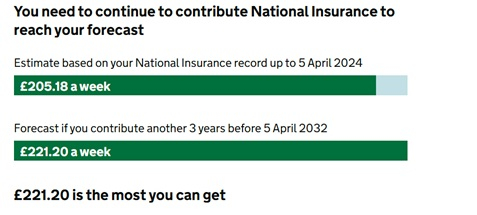

Here is a screenshot of my SP forcast below

I was slightly out as I thought I was only 1 year short but come April it will be 2 years short which I am hoping to pay.

Are you saying that because I was contracted out I will need additional years? I thought I was contracted out of SERPS and understand that I would not get the additonal SP.

There is no Contracted Out Pension Equivalent (COPE) number on my forecast so not entirely sure where I would find this? Its not on my USS forcast either.

Its even more confusing since on the SP forecast website it states that COPE does not affect the forecast which still stands.

Ahhhhh I thought the SP would be the easy bit, clearly I have a lot more research to do!! 0

0 -

You need 3 additional years to reach £221.20.Twigwidge said:BrilliantButScary said:

Please check your state pension forecast again, what does it actually say? You will have been 'contracted out' during your employment and may need more years than you think for a full state pension.Twigwidge said:Many thanks to everyone that has replied so quickly, as I mentioned I am on a very steep learning curve here so all these comments/advice are very gratefully received 😊. This is rather long as I wanted to reply to the initial comments

@QrizB, unfortunately the only other savings I have are just under 10K in a cash ISA, as I have been using all spare cash over last few years to finish paying off mortgage (which is now paid)

@Dazed_and_C0nfused, yes this amount does have an actuarial reduction because of age and also a penalty for going before the age of 60 (explained below)

Here is my USS model prediction (hope I am allowed to post this)

£18.239 gross pension = £17,105 net = Just over £1,400 a month

The maximum tax free lump sum of 121,595 will be topped up to £151,000 by a tax-free voluntary severance payment of £30,000 to £151,000

@Dazed_and_C0nfused, I am not sure what tax code would be used, I have heard that some people initially are put on an emergency tax code but claim any overpayments back, how would I find out what tax code I would be on? Yes this £1,400 would be net (assuming my calculations above are correct)

@LL_USS, As far as I understand the USS pension rules (and they are not easy to understand to me 😊) I seem to be better off taking the maximum tax free lump sum as USS (appear) to give a one off opportunity (I think this is what GrumpyDill is referring to?) of taking most of my defined contribution savings tax free (note on USS model screenshot that my DC pot is at Zero if I take the maximum TF lump sum)

@Phossy, yes initially I will put all my tax free money into a 4% savings account and the transfer over a few years into both mine and my partner’s ISA allowances 😊 Yes I agree about savings protection and will definitely split initial savings over 2 accounts to benefit from the £85,000 FSCS protection

@Linton and Marcon, aside from near 10k in an ISA I have no other savings or pension pots of any kind and I have checked my state pension forecast and will have 34 full years at time of retirement 31st July) so I will need to top up 1 year eventually to get full state pension. I think there is a 10% cap on USS pension increases but it is not entirely clear on their website.

@Marcon I had no real opportunity to save since all extra cash has been used to finish paying off my mortgage, so just under 10K in an ISA and that’s all my savings, I will certainly max out both mine and partners ISAs when my lump sum is paid 😊 Sorry about the £ sign, I was typing my initial post on my phone and it is a nightmare to access the symbols, I will edit the original post later this evening if I can work out how to do this 😊

@Abermarle, Yes I could take slightly more pension and less lump sum, the maximum DB pension I can take is £19,357 gross (see screenshot below)

This would be a fraction under £18,000 net (£17,999) = bang on £1,500 per month net

But obviously this reduces my lump sum by £25,649 (121,595-95,946)

If I went down this route the total going into my savings would now be £95,946+£30,000 (severance) = £125,946

So if I put this in my savings account to top my pension up to my desired £2,500 per month I need £1,000 per month for 7 years (to state pension)

1,000 x 12 x 7 = £84,000 = This would leave £41,946 of my lump left at state pension age

After playing with the modeller to me it seems the most sensible choice for me was to take the maximum lump sum as taking the maximum pension would only give me an additional £75 per month (net) but result in a loss of 25.5K lump sum (I guess it is just personal choice in the end). I think this is what @Secret2ndAccount is indicating later in the thread as the reverse commutation factor is so poor

@Barralad77, I would love to take my pension at 60 to avoid the penalty but if I want the severance package like many Universities I have to take it by 31st July (a few months before I turn 60) I have looked into this with the Uni but they won't budge on this. I was hoping that if I still went on 31st July but deferred taking my pension until after I was 60 that this may be a way around the early penalty but after speaking with the USS advisor on the phone, deferring the pension immediately triggers the early penalty. I don't think there is any way around this (unless anyone knows better). For me I am willing to take the hit to get the severance package 😊

@Secret2ndAccount, Yes I certainly will be looking at other places to put the lump sum, I just have a feeling that investments in the current world economic climate may be a bit more risky than usual so probably safer in ISAs and the highest interest savings accounts I can get.

Thanks so much everyone for taking the time to reply

@BrilliantButScaryBrilliantButScary said:

Please check your state pension forecast again, what does it actually say? You will have been 'contracted out' during your employment and may need more years than you think for a full state pension.Twigwidge said:Many thanks to everyone that has replied so quickly, as I mentioned I am on a very steep learning curve here so all these comments/advice are very gratefully received 😊. This is rather long as I wanted to reply to the initial comments

@QrizB, unfortunately the only other savings I have are just under 10K in a cash ISA, as I have been using all spare cash over last few years to finish paying off mortgage (which is now paid)

@Dazed_and_C0nfused, yes this amount does have an actuarial reduction because of age and also a penalty for going before the age of 60 (explained below)

Here is my USS model prediction (hope I am allowed to post this)

£18.239 gross pension = £17,105 net = Just over £1,400 a month

The maximum tax free lump sum of 121,595 will be topped up to £151,000 by a tax-free voluntary severance payment of £30,000 to £151,000

@Dazed_and_C0nfused, I am not sure what tax code would be used, I have heard that some people initially are put on an emergency tax code but claim any overpayments back, how would I find out what tax code I would be on? Yes this £1,400 would be net (assuming my calculations above are correct)

@LL_USS, As far as I understand the USS pension rules (and they are not easy to understand to me 😊) I seem to be better off taking the maximum tax free lump sum as USS (appear) to give a one off opportunity (I think this is what GrumpyDill is referring to?) of taking most of my defined contribution savings tax free (note on USS model screenshot that my DC pot is at Zero if I take the maximum TF lump sum)

@Phossy, yes initially I will put all my tax free money into a 4% savings account and the transfer over a few years into both mine and my partner’s ISA allowances 😊 Yes I agree about savings protection and will definitely split initial savings over 2 accounts to benefit from the £85,000 FSCS protection

@Linton and Marcon, aside from near 10k in an ISA I have no other savings or pension pots of any kind and I have checked my state pension forecast and will have 34 full years at time of retirement 31st July) so I will need to top up 1 year eventually to get full state pension. I think there is a 10% cap on USS pension increases but it is not entirely clear on their website.

@Marcon I had no real opportunity to save since all extra cash has been used to finish paying off my mortgage, so just under 10K in an ISA and that’s all my savings, I will certainly max out both mine and partners ISAs when my lump sum is paid 😊 Sorry about the £ sign, I was typing my initial post on my phone and it is a nightmare to access the symbols, I will edit the original post later this evening if I can work out how to do this 😊

@Abermarle, Yes I could take slightly more pension and less lump sum, the maximum DB pension I can take is £19,357 gross (see screenshot below)

This would be a fraction under £18,000 net (£17,999) = bang on £1,500 per month net

But obviously this reduces my lump sum by £25,649 (121,595-95,946)

If I went down this route the total going into my savings would now be £95,946+£30,000 (severance) = £125,946

So if I put this in my savings account to top my pension up to my desired £2,500 per month I need £1,000 per month for 7 years (to state pension)

1,000 x 12 x 7 = £84,000 = This would leave £41,946 of my lump left at state pension age

After playing with the modeller to me it seems the most sensible choice for me was to take the maximum lump sum as taking the maximum pension would only give me an additional £75 per month (net) but result in a loss of 25.5K lump sum (I guess it is just personal choice in the end). I think this is what @Secret2ndAccount is indicating later in the thread as the reverse commutation factor is so poor

@Barralad77, I would love to take my pension at 60 to avoid the penalty but if I want the severance package like many Universities I have to take it by 31st July (a few months before I turn 60) I have looked into this with the Uni but they won't budge on this. I was hoping that if I still went on 31st July but deferred taking my pension until after I was 60 that this may be a way around the early penalty but after speaking with the USS advisor on the phone, deferring the pension immediately triggers the early penalty. I don't think there is any way around this (unless anyone knows better). For me I am willing to take the hit to get the severance package 😊

@Secret2ndAccount, Yes I certainly will be looking at other places to put the lump sum, I just have a feeling that investments in the current world economic climate may be a bit more risky than usual so probably safer in ISAs and the highest interest savings accounts I can get.

Thanks so much everyone for taking the time to reply

Here is a screenshot of my SP forcast below

I was slightly out as I thought I was only 1 year short but come April it will be 2 years short which I am hoping to pay.

Are you saying that because I was contracted out I will need additional years? I thought I was contracted out of SERPS and understand that I would not get the additonal SP.

There is no Contracted Out Pension Equivalent (COPE) number on my forecast so not entirely sure where I would find this? Its not on my USS forcast either.

Its even more confusing since on the SP forecast website it states that COPE does not affect the forecast which still stands.

Ahhhhh I thought the SP would be the easy bit, clearly I have a lot more research to do!!

You may well have already earned enough in the current year to add a further £6.32.

A second year will add another £6.32, taking you to £217.82.

The third year adds the final £3.38.0 -

I suspect that we are probably in agreement. The way I see the current scenario is that the OP has been asked to leave work six months from now, and it seems he’s intent on taking his pension at that point. In that case, the Uni is obviously happy to keep paying him for those 6 months but he will lose out on the pension due to the worse factor being applied (because he’ll only be 59). In my hypothetical scenario he ‘spreads’ those 6.0 FTE months across a period of 11 months such that (a) the Uni still only pays him for 6.0 FTE months but (b) he exits after turning 60. I raised it as a possible bartering tool to use with the Uni (I.e. point out to them that if the OP reduces his hours from March but remains employed after July it shouldn’t cost the Uni very much extra at all, compared with them paying him for working full time until end of July. It would, arguably, be a win-win (the Uni secures a VS and the OP secures the better ER factor, and hence the better pension). The only important point is the one you’ve highlighted: In scenario A he turns 60 after taking his pension (so loses out on the USS factors) but in scenario B he takes his pension after turning 60 but he will only be employed for 6.0 FTE months in both scenarios.Marcon said:

But you don't need to work get any particular number of FTE months as your post suggested - that was the bit I was clarifying:Barralad77 said:

Yes, that’s my point. If you leave one day after turning 60 the ER factor will be bettter. If you leave 24 hours early (59 years and 364 days) it will be worse. Finish at 59 years and the normal pension age for that portion of the contributions will be deemed to be 63.5. Take it at 60 and it will be taken as 60 (I.e.. zero reduction applied). The difference in pension benefits accrued (1.0 vs 0.5) for a few months will barely be noticeable in the big scheme of things.Marcon said:

The issue here is whether or not someone leaves while still an active member and takes their pension immediately (as opposed to taking their pension from deferred status) - not the actual hours they are working or the length of the extra service they clock up if working part time.Barralad77 said:Re. The point about losing out even if you defer taking it until you’ve turned 60. I learnt the same thing long after I’d spent years believing otherwise. It’s really annoying and I’ve never known what the reasoning behind it is. In terms of you discussing the possibility of staying on a few months longer, have you asked whether they’d accept you reducing your hours such that you would still be working a further 6.0FTE months? For example, if you needed to stay working until the end of December, would they allow you to drop down to, say, 0.5 for 10 months? So rather than earn 6 x 1.0 (Feb-July) you would work 1 x 1.0 (Feb) plus 10 x 0.5 (Mar-Dec). They both work out at 6.0 FTE months. Obviously, there are other factors to consider but it’s something I’d consider pursuing (if you’re losing out quite a bit on the pension for the sake of a handful of months).Barralad77 said:For example, if you needed to stay working until the end of December, would they allow you to drop down to, say, 0.5 for 10 months? So rather than earn 6 x 1.0 (Feb-July) you would work 1 x 1.0 (Feb) plus 10 x 0.5 (Mar-Dec). They both work out at 6.0 FTE months.

The point is that normally you simply need to be in active membership of a scheme at the point of taking your benefits, so OP would only need to work to 31 December if that's the 'magic birthday' date (unless there's something very odd about USS!).1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards